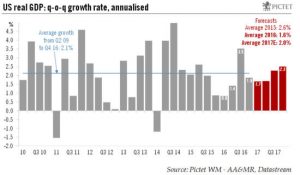

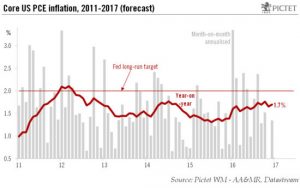

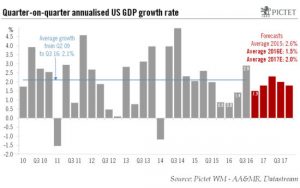

The latest non-farm payroll report is unlikely to make the Fed deviate from plans for policy normalisation.All in all, today’s employment report was healthy. In the end, job creation was actually quite robust overall in Q2, ‘aggregate weekly payrolls’ rose strongly q-o-q, and if unemployment rebounded a little in June, it was only because of higher participation, not a lack of employment growth. However, once again, wage data brought some disappointment, with average hourly earnings increasing by less than expected in June, although we continue to expect wage increases in the US to gradually pick up over the coming quarters.We are not modifying our scenario for US economic growth and monetary policy in light of the latest statistics. Our forecast for US GDP growth of 2.7% q-o-q annualised

Read More »US job market remains strong, but wage growth still disappoints

July 7, 2017