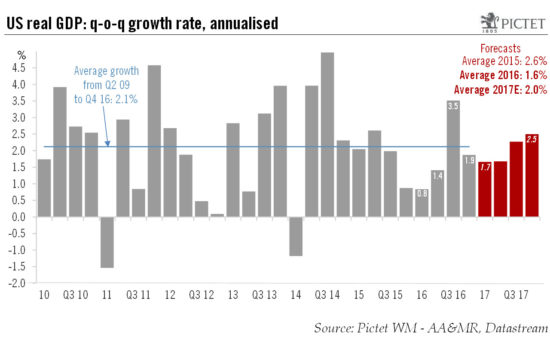

In spite of softness in headline Q4 GDP figure, growth momentum in the US picked up in the second half of 2016 and should be underpinned by fiscal stimulus later this year.US GDP growth decelerated from 3.5% in Q3 to 1.9% quarter-on-quarter annualised in Q4, below consensus expectations of 2.2%. However, this soft reading was mainly due to a reversal of the surge in soybean exports in the previous quarter, while growth in final domestic demand picked up from 2.1% in Q3 to 2.5% in Q4. Overall, it is probably more meaningful to look at growth by semester rather than by quarter. In the second half of last year, GDP growth averaged a strong 2.7%, following a weak 1.1% in the first half.Looking forward, the recent substantial tightening in monetary conditions should weigh on US growth in the first six months of 2017, while fiscal stimulus should boost it in the second half. Although there has been a significant correction over the past two weeks, on a trade-weighted basis the US dollar is still some 3.5% higher than it was just before Donald Trump won the presidency. Together with the spike in long-term interest rates and the 25bp Fed’s hike in December, this has resulted in a marked tightening of monetary conditions. We estimate the tightening over the past four months to be equivalent to an increase of around 120 basis points in short-term rates.

Topics:

Bernard Lambert considers the following as important: Macroview, US fiscal stimulus, US GDP acceleration, US GDP growth, US growth forecast

This could be interesting, too:

Cesar Perez Ruiz writes Weekly View – Big Splits

Cesar Perez Ruiz writes Weekly View – Central Bank Halloween

Cesar Perez Ruiz writes Weekly View – Widening bottlenecks

Cesar Perez Ruiz writes Weekly View – Debt ceiling deadline postponed

In spite of softness in headline Q4 GDP figure, growth momentum in the US picked up in the second half of 2016 and should be underpinned by fiscal stimulus later this year.

US GDP growth decelerated from 3.5% in Q3 to 1.9% quarter-on-quarter annualised in Q4, below consensus expectations of 2.2%. However, this soft reading was mainly due to a reversal of the surge in soybean exports in the previous quarter, while growth in final domestic demand picked up from 2.1% in Q3 to 2.5% in Q4. Overall, it is probably more meaningful to look at growth by semester rather than by quarter. In the second half of last year, GDP growth averaged a strong 2.7%, following a weak 1.1% in the first half.

Looking forward, the recent substantial tightening in monetary conditions should weigh on US growth in the first six months of 2017, while fiscal stimulus should boost it in the second half. Although there has been a significant correction over the past two weeks, on a trade-weighted basis the US dollar is still some 3.5% higher than it was just before Donald Trump won the presidency. Together with the spike in long-term interest rates and the 25bp Fed’s hike in December, this has resulted in a marked tightening of monetary conditions. We estimate the tightening over the past four months to be equivalent to an increase of around 120 basis points in short-term rates. Continued uncertainties surrounding the Trump administration’s policies and potential announcements on the trade front could also weigh on growth in the first half.

For the time being, our best guess remains that the measures that president Trump effectively takes on the trade front will prove limited (higher tariffs only for a short period or only on specific products, renegotiation of trade treaties rather than repeal), with only a modest impact on growth and inflation, at least this year.

More positively, the fiscal stimulus that is widely expected should start to boost growth in the second half of this year. As a consequence, our growth forecasts remain unchanged. We continue to believe that US GDP growth will slow to some 1.7% on average in the first half of 2017, before picking up to 2.4% in the second half. On a yearly average basis, growth should accelerate to 2.0% in 2017 from 1.6% in 2016.