Consumer Confidence, as surveyed by the Conference Board and University of Michigan, shows consumers are starting to lose economic confidence. Given that consumer spending drives the economy and influences inflation, confidence and the means to spend can significantly impact markets. Based on recent job data, the means (i.e., wages) to consume appear to be in good shape. However, consumer savings are historically low, while credit card balances are high. Recently, in a sign that the average consumer may be retrenching, consumer debt declined by the largest amount in ten years, excluding an instance in early 2020. Equally crucial to consumer spending is confidence. Even if consumers have the financial ability to consume, they must also have the desire or

Topics:

RIA Team considers the following as important: 9) Personal Investment, 9a.) Real Investment Advice, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Consumer Confidence, as surveyed by the Conference Board and University of Michigan, shows consumers are starting to lose economic confidence. Given that consumer spending drives the economy and influences inflation, confidence and the means to spend can significantly impact markets. Based on recent job data, the means (i.e., wages) to consume appear to be in good shape. However, consumer savings are historically low, while credit card balances are high. Recently, in a sign that the average consumer may be retrenching, consumer debt declined by the largest amount in ten years, excluding an instance in early 2020. Equally crucial to consumer spending is confidence. Even if consumers have the financial ability to consume, they must also have the desire or confidence in their economic outlook to spend. Accordingly, it's not just the broad measure of confidence that is declining that concerns us, but confidence in the labor market.

The graph below shows that consumers' expectations of fewer jobs in six months jumped to a level last seen ten years ago. Many consumers will cut back on their consumption if they have concerns that they could lose their jobs or even not get an appropriate raise. Moreover, if the unemployment rate rises, consumer confidence will weaken further, negatively impacting spending and hurting the labor market. Consequently, in a circular fashion, weaker confidence in the labor market can become a self-fulfilling prophecy.

Given the political climate and post-holiday consumption patterns, it's too early to read too much into consumer surveys. Therefore, it's too soon to forecast an uptick in the unemployment rate based on one or two confidence measures. However, it is worth closely monitoring consumer sentiment and personal consumption.

What To Watch Today

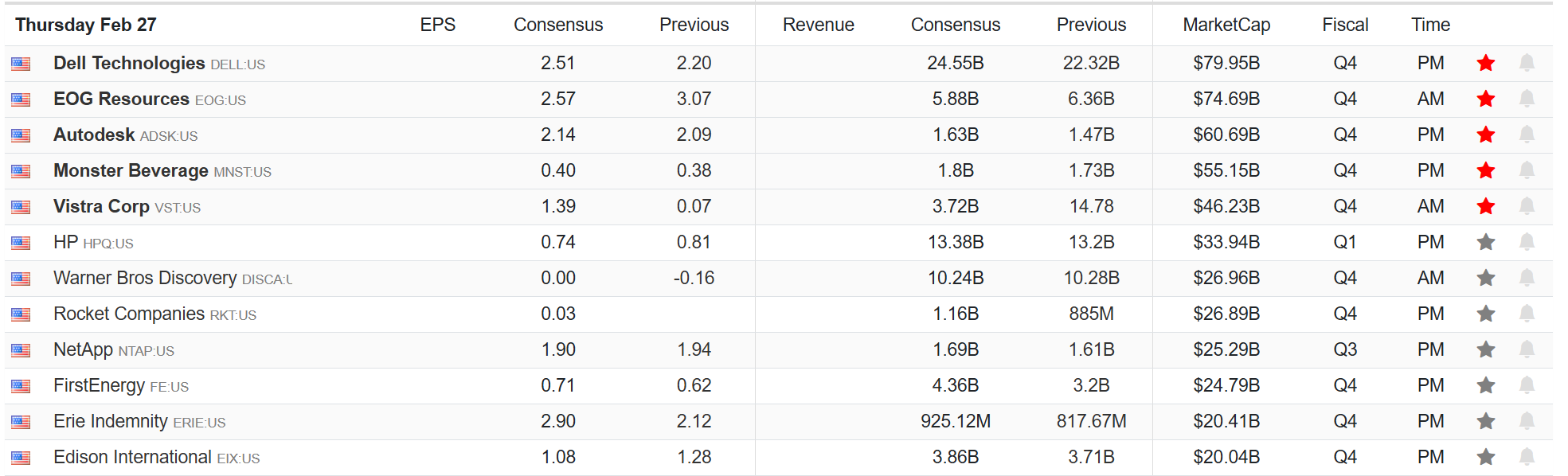

Earnings

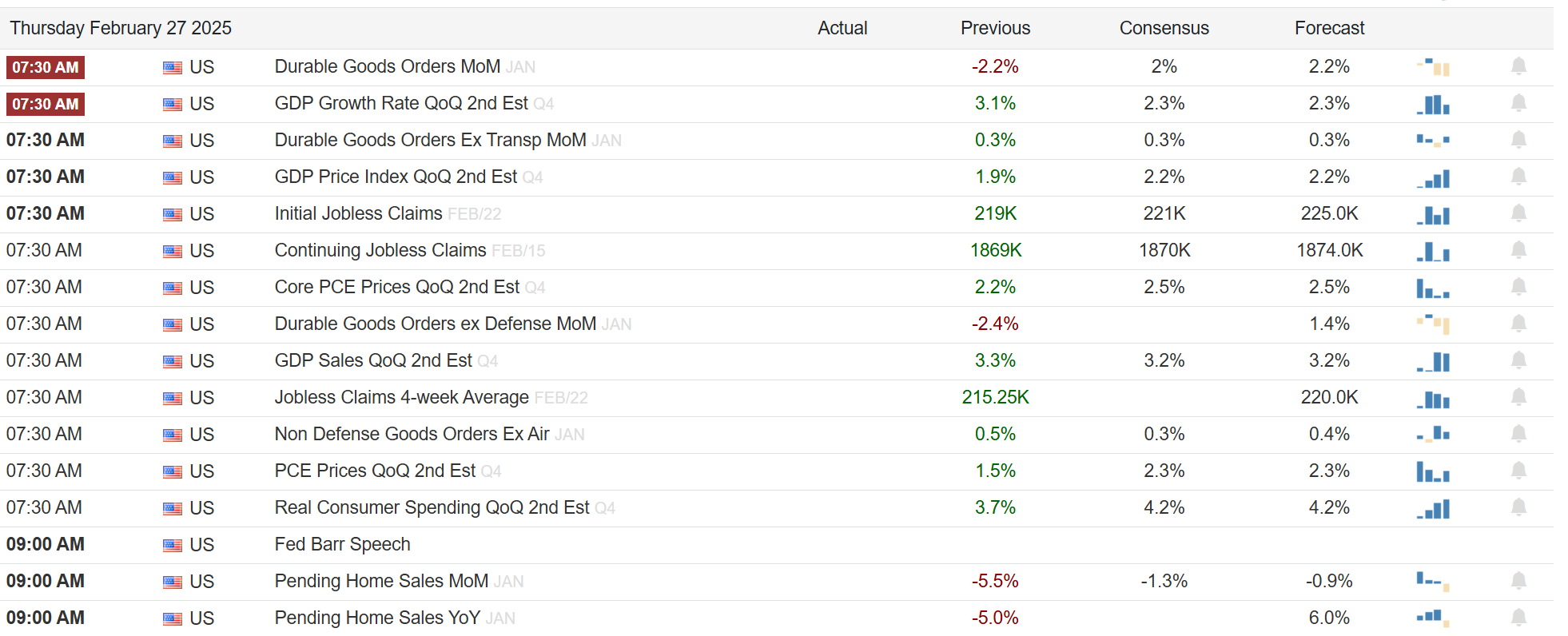

Economy

Market Trading Update

Yesterday, we discussed the bid bonds have gotten lately as their hedging capability for volatile markets returned. Today, I wanted to provide a note about "stop losses" and how to use them in today's market environment.

Before 2008, and really before the introduction of instantaneous market information and algorithms, investors could safely place a "stop loss" order in the market to hedge portfolios. If the price declined to that level, the position was automatically sold, and the investor was protected. Today that is no longer the case. When investors put "stop loss" orders into the market, many algorithmic programs and computerized trading systems will "hunt" those orders by driving stock prices lower to trigger those sales and then immediately reverse to buy orders once triggered. Such has frustrated many investors into making the mistake of not using stop orders at all.

Tuesday and Wednesday provided a good lesson on managing stop-loss levels in portfolios. First, investors can no longer put "live" orders that the algorithms can see in the market. Instead, investors must be diligent about stop/-loss levels and maintain them mentally. Here is a good example of how to manage that.

Let's assume that we use the 100-DMA as the trailing stop-loss level. I like moving averages better than a fixed number or a percentage loss. On Tuesday, the market violated the 100-DMA early in the afternoon. However, instead of immediately reacting to that break, investors should be patient and wait to see if that break holds. By giving the market some time, the selling pressure reversed, and buying entered the market, pushing the market back above the 100-DMA. Wednesday saw a repeat of the situation where the market defended the 100-DMA without decisively breaking it.

While markets are very close to triggering a stop loss, it hasn't done so yet. Furthermore, when a stop-loss level is triggered, markets are often oversold enough for a reflexive bounce, which also frustrates investors who sold on the initial break of the stop-loss. As investors, we look for three signals to confirm the break of a stop-loss.

- A break of the stop-loss level.

- A reflexive rally that fails to move above the previous break level.

- A reversal lower confirming the stop-loss level is broken.

This is just our method of managing stop-loss levels to hedge risk in our portfolios. However, while we often do sell at slightly lower prices, that small penalty has saved us numerous times from getting whipsawed by a market recovery.

How you manage your risk exposures is up to you. This is just ours. I hope you find it useful.

Not QE, QE

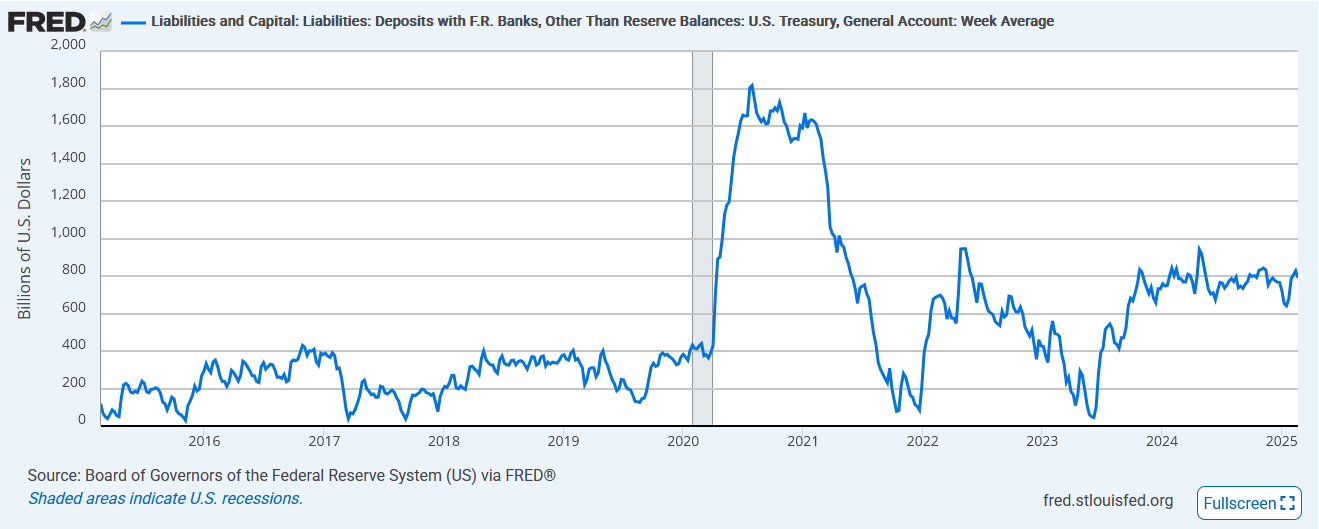

As the debt ceiling approaches, a few media pundits use the term QE to describe how the Treasury will fund itself. The government hit its $36 trillion debt ceiling in late January. Since then, they have been using emergency measures to continue funding the government. However, in mid-March, those accounting gimmicks will be unavailable. In mid-March, the Treasury will then draw down its "savings account" held at the Fed. The Treasury General Account (TGA) currently has about $800 billion. The $800 billion in liquidity was removed from the market when the debt was issued. Therefore, the liquidity will be released back to the market and economy when they spend it down.

Thus, some think the additional liquidity is equivalent to QE. We argue that may be true, but it's not nearly as powerful for stocks. For starters, the money goes straight into the economy, not financial markets. Second, the drawdown is limited in amount and time. Once an agreement is forged, the drawdown is likely to end. Moreover, the Treasury may ramp up its debt issuance to replenish the TGA, thus removing liquidity. Bear in mind that the Treasury will issue debt but can only do so to replace maturing debt.

We will have more on this topic next week in an article about liquidity.

Managing Your Inner Voice

The combination of extremely rich equity valuations, high interest rates, and a new President taking bold actions will likely continue to whip stocks around for the foreseeable future. Alongside those volatility-provoking factors is that the S&P 500 just posted two annual twenty-plus percent gains in a row. Accordingly, seeing average or below-average returns this year and volatility spikes should not be surprising. If we are correct about volatility, it’s entirely possible that our worst behavioral traits as investors will be provoked. Given this possibility, it’s worth taking a break from our typical market or economic topics and focusing on behavioral economics.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.

The post Consumers Are Losing Confidence appeared first on RIA.

Tags: Featured,newsletter