Yesterday morning we noted why, in light of the ongoing global bond rout, all eyes would be on the BOJ, and specifically whether Kuroda would engage his "Yield control" operation to stabilize the steepness of the JGB yield curve and implicitly support global bond yields in what DB said would be "full blown helicopter money" where the "BoJ is flying the copter over the US and may be about to become the new US government’s best friend." And sure enough that is precisely what Kuroda did last night after the Bank of Japan "fired a warning at the bond market" as Bloomberg described it, offering to buy an unlimited amount of debt at fixed yields for the first time, an operation meant to maintain the central bank's yield-curve target and which stopped the bleeding not only across Japanese but also global bonds, in the process pushing the dollar lower. The central bank announced two operations, one to buy two-year notes at minus 0.09 percent, and another for five-year debt at minus 0.04 percent. That came after two-year yields rose as high as minus 0.095 percent on Wednesday, up 18 basis points in five days. The BOJ introduced the tools after deciding in September it would control the yield curve. As Bloomberg notes, the so-called fixed-rate operation yielded no bids, a sign that the move was more of a demonstration exercise than an intended transaction in notes.

Topics:

Tyler Durden considers the following as important: Abenomics, ASX 200, Australia, B+, Bank Negara Malaysia, Bank of Japan, Banking, Barclays, BlackRock, Bloomberg Dollar Spot, Bloomberg News, Bond, Business, China, Consumer Prices, Continuing Claims, Copper, CPI, Crude, Dow 30, Dow Jones Industrial Average, Economic Calendar, economy, European Central Bank, European Union, Eurozone, FED, Federal Communications Commission, Federal Funds Rate, Federal Reserve, Finance, fixed, Fixed income market, France, Freddie Mac, FTSE 100, Futures market, Germany, Hang Seng 40, headlines, Housing Market, Housing Starts, Initial Jobless Claims, Interest Rate, Internal Revenue Service, Iran, Iraq, Ireland, Italy, Jamie Dimon, Janet Yellen, Japan, Japanese government, Jim Reid, Joint Economic Committee, Market Share, Monetary Policy, Money, NAHB, Nikkei, Nikkei 225, OLED, OPEC, Organization of Petroleum-Exporting Countries, percentThe U.S. government, Philadelphia Fed, Philadelphia Fed manufacturing, ratings, Reserve Bank of Australia, Russell 2000, S&P 500, S&P GSCI, S&P/ASX 200, Saudi Arabia, Stoxx 600, Testimony, Topix, Trump Administration, Trump Cabinet, U.S. Treasury, Unemployment, United Nations, US Federal Reserve, US government, West Africa, White House, Yen, Yield Curve, Zurich

This could be interesting, too:

investrends.ch writes BlackRock Bitcoin-ETF mit Rekordabfluss

investrends.ch writes Trump deutet Powell-Nachfolge bis Jahresende an

investrends.ch writes Jerome Powell schürt Hoffnungen auf tiefere Zinsen

investrends.ch writes Jerome Powell: «Es gibt keinen risikolosen Weg»

Yesterday morning we noted why, in light of the ongoing global bond rout, all eyes would be on the BOJ, and specifically whether Kuroda would engage his "Yield control" operation to stabilize the steepness of the JGB yield curve and implicitly support global bond yields in what DB said would be "full blown helicopter money" where the "BoJ is flying the copter over the US and may be about to become the new US government’s best friend." And sure enough that is precisely what Kuroda did last night after the Bank of Japan "fired a warning at the bond market" as Bloomberg described it, offering to buy an unlimited amount of debt at fixed yields for the first time, an operation meant to maintain the central bank's yield-curve target and which stopped the bleeding not only across Japanese but also global bonds, in the process pushing the dollar lower.

The central bank announced two operations, one to buy two-year notes at minus 0.09 percent, and another for five-year debt at minus 0.04 percent. That came after two-year yields rose as high as minus 0.095 percent on Wednesday, up 18 basis points in five days. The BOJ introduced the tools after deciding in September it would control the yield curve. As Bloomberg notes, the so-called fixed-rate operation yielded no bids, a sign that the move was more of a demonstration exercise than an intended transaction in notes. Officials acted amid relative calm in the market, but in the wake of a global bond sell-off in the past week that had driven up yields across the globe -- and in the process put pressure on Japanese government bonds as well. “It’s a surprise that the BOJ took action today,” said Souichi Takeyama, a rates strategist at SMBC Nikko Securities Inc. in Tokyo, a unit of Japan’s second-biggest lender. “Markets won’t test levels above these fixed rates as these will be seen as reflecting the BOJ’s upper limit.”

“The aim is to send a warning to markets about a significant surge in rates,” said Keiko Onogi, a fixed-income strategist at Daiwa Securities Co. in Tokyo. At the same time, “there are questions as to why the BOJ conducted this operation now, when the market had already stabilized after the surge in yields to yesterday,” she said.

“The BOJ will have welcomed the rise in Japanese stocks and decline in the yen following the Trump Shock, but they’ve shown they aren’t going to stand for a jump in JGB yields,” said Naoya Oshikubo, a rates strategist at Barclays Plc in Tokyo. “It’s the strength of that stance rather than the actual levels at which the BOJ offered to buy the debt that’s pulling down yields.”

The BOJ operation helped halt a five-day selloff in Japanese bonds, and government securities advanced from Australia to Germany, together with U.S. Treasuries. The euro strengthened for the first time in nine days as Bloomberg’s dollar index slipped from a nine-month high. Crude reversed declines as OPEC and Russia prepared to meet in Doha for more talks. European shares were little changed, and Asian equities rose with Japan’s Topix measure closing on the brink of a bull market.

In the US traders are walking to their desks, awaiting testimony from Federal Reserve Chair Janet Yellen before the Joint Economic Committee that will help shape the outlook for interest rates: focus will be on her comments about the December rate hike and the speed of future moves as financial conditions have materially tightened in recent days.

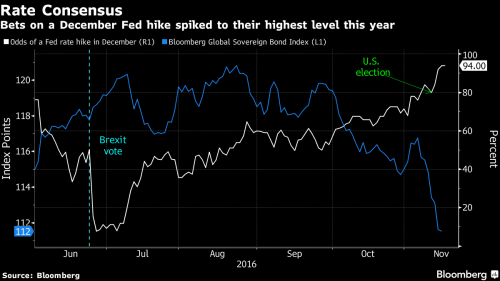

A December increase is now all but assured by the futures market which gives it a 94% probability, while prospects for further tightening triggered a global bonds rout and boosted the dollar since the start of last week.

“From the BOJ operation, it looks like it’s a firmer cap on yields than was previously being expected, so that’s supportive for fixed-income globally, ” said Peter Chatwell, head of rates strategy at Mizuho International Plc in London. “It means that the other markets can trade with a bit less of downside risk, or downside fear.”

Japan's intervention eased the Bloomberg Dollar Spot Index, which was down 0.2 percent. The yen rose 0.1 percent to 108.95 per dollar, but is still down more than 3 percent since Trump’s victory. The euro strengthened 0.3 percent against the dollar, halting an eight-day losing streak. The pound gained for the first time in four days as figures from the Office for National Statistics showed U.K. spending remained robust despite the Brexit vote.

Crude gained 0.4 percent to $45.76 a barrel in New York as Saudi Arabia and some other OPEC nations meet with Russia for informal talks without oil ministers from Iran and Iraq, the two countries that pose the biggest hurdle to an output deal. Russia will hold discussions with representatives from the Organization of Petroleum Exporting Countries in Doha from Thursday, Energy Minister Alexander Novak said.

The Stoxx Europe 600 Index added 0.1 percent. While the gauge has remained calm in recent days, it has alternated between intraday gains and losses for eight straight sessions, the longest streak in two years. Its valuation of about 14 times estimated earnings is at its lowest since Brexit relative to a measure tracking global shares. S&P 500 futures were little changed after the gauge slipped 0.2 percent on Wednesday. It closed within 0.6 percent of the record reached in August, while the Dow Jones Industrial Average slipped 0.3 percent from the all-time high it reached on Tuesday. The Russell 2000 Index of small-cap shares closed at a peak.

Among stocks moving on corporate news:

- Zurich Insurance Group AG gained 2.7 percent after saying it will increase its dividend and cut costs.

- Royal Ahold Delhaize NV declined 3.1 percent as its quarterly profits missed analyst projections.

- ABN Amro Group NV fell 3.1 percent after the Dutch state sold 65 million of its shares.

- Cisco Systems Inc. lost 4.4 percent in early New York trading after projecting sales and profit pointing to a slowdown in corporate spending on technology hardware.

Treasury 10-year yields fell three basis points to 2.19 percent at 9:19 a.m. London time, retreating further from this year’s high of 2.3 percent, reached Monday, after the BOJ’s first offer to buy an unlimited amount of securities. Japanese bonds also rose after the operation, which was viewed by many as a response to the surge in global yields. 10Y German bund yields also dropped three basis points, to 0.24 percentThe U.S. government will sell TIPS on Thursday, and demand may be robust, with BlackRock Inc., Fidelity Investments and Pacific Investment Management Co. all having recommended the securities since the presidential vote on speculation that Trump’s policies will boost consumer prices.

* * *

Bulletin Headline Summary From RanSquawk

- European equities enter the North American crossover mostly lower as financial names pause for breath after recent election-inspired upside

- Some tentative signs of USD moderation in the making, with USD moderation against the EUR and JPY seeing 1.0650 and 110.00 levels respectively held

- Looking ahead, highlights include UK retail sales, EU & US CPI, ECB minutes, US weekly jobless data, housing starts & Philadelphia Fed Manufacturing Index & a host of Fed speakers

Global Market Wrap

- S&P 500 futures up 0.1% to 2175

- Stoxx 600 up 0.1% to 339

- FTSE 100 up 0.3% to 6770

- DAX down 0.3% to 10629

- German 10Yr yield down 2bps to 0.28%

- Italian 10Yr yield down 2bps to 2.02%

- Spanish 10Yr yield down 2bps to 1.52%

- S&P GSCI Index up 0.2% to 358.3

- MSCI Asia Pacific up 0.3% to 135

- Nikkei 225 up less than 0.1% to 17863

- Hang Seng down less than 0.1% to 22263

- Shanghai Composite up 0.1% to 3208

- S&P/ASX 200 up 0.2% to 5339

- US 10-yr yield down 3bps to 2.2%

- Dollar Index down 0.29% to 100.12

- WTI Crude futures up 0.2% to $45.66

- Brent Futures up 0.2% to $46.72

- Gold spot up 0.2% to $1,227

- Silver spot up 0.3% to $17.04

Top Headline News

- Apple Wants OLED in iPhones, But Most Suppliers Aren’t Ready Yet: Display makers seen struggling to meet iPhone output in 2017

- Apple Is Said To Cut Fees Video Services Will Pay for App Store

- Dimon Told Trump Team He Has No Interest in Treasury: Fortune

- Gingrich Doesn’t Want Formal Role in Trump White House: Fox

- Haley, McMaster Considered for Trump Cabinet: Post and Courier

- Verizon’s Buy of Fiber Network From Icahn’s XO Wins Approval: FCC clears $1.8 billion deal, says it doesn’t harm competition

- Ahold Delhaize Profit Misses Estimates on U.S. Deflation: Price pressure erodes sales at Food Lion supermarket chain

- Gilead’s Myelofibrosis Drug Gets Mixed Results in Cancer Trials: Treatment for a rare bone marrow cancer succeeded in one trial and failed in another

- Facebook Yields to IRS Demand for Records Over Asset Transfer: IRS demands for records related to co.’s transfer of global operations to Ireland in 2010

- Sen. Cotton Plans to Offer $26b Emergency Defense Spending Bill

* * *

Looking at regional markets, we start in Asia where stocks were slightly downbeat following a lacklustre lead from Wall St, where underperformance in energy and financials weighed on sentiment and saw DJIA close negative for the first time in 8 days. Nikkei 225 (Unch) was driven by JPY fluctuations, while ASX 200 (+0.2%) closed higher amid strength in defensive stocks with weak employment data also raising doubts that RBA may not be done with its easing cycle. Shanghai Comp (+0.1%) dampened amid ongoing trade concerns, while downside in the Hang Seng (-0.3%) was stemmed by consumer names and banks. 10yr JGBs gained with outperformance seen in the short-end after the BoJ announced to purchase an unlimited amount of bonds ranging from 1yr-5yr maturities at fixed rates which suggested an intent to cap yields if needed, although the BoJ found no takers and some gains were later pared following a weaker 20yr auction in which the b/c and average price fell from the prior month.

Japanese cabinet advisor Fujii stated he wants additional fiscal stimulus in 2017 and would like JPY 21trl added to the primary budget in the next fiscal year and in the following years thereafter.

Top Asian News

- JPMorgan Said Set to Pay $200 Million in China Hires Settlement: Non-prosecution deal reflects bank’s cooperation with inquiry

- Yuan Watchers Lower Forecasts as Trump Victory Raises Risks: Currency may weaken to 7 per dollar early next year

- Philippines Posts Strongest Economic Growth in Asia at 7.1%: Nation seen as among fastest-expanding in the world until 2018

- BOJ First Unlimited Bond Buys Get No Bids After Yields Retreated: BOJ announces first fixed-rate operation to buy JGBs

- Ward Ferry to Shut 15-Year-Old Asia Hedge Fund as Co-CIO Leaves: Co. will focus on long-only funds after Nash-Webber leaves

In Europe, bourses opened lower following the lead from Wall Street, as DAX (-0.2%) and EUROSTOXX (-0.2%) have both seen underperformance in financial names after a retracement from recent election-inspired gains. The Telecoms sector is the outperformer following reports of a potential merger between T-Mobile and Sprint in the US. Bond markets have also received a bid inline with general risk sentiment. In Italy the latest polls put the no vote ahead and with the referendum too close to call and as more comments filter through to the markets we must keep a close eye on eye on Italian yields particularly the short end.

Top European News

- VW Loses European Market Share as Scandal Effect Lingers: Carmaker’s October sales fell 1.8% vs. market’s 0.3% drop

- ABN Amro’s Dutch State Owner Selling 7% as Part of Exit Plan: Stock up 18% in 12 months as most European lenders have fallen

- Rio Tinto Fires Two Senior Executives Amid Payment Probe: fired two of its top executives over a payment connected to a giant iron ore project in Guinea in West Africa

- NN Group Chief Wants Delta Lloyd to Open Up to Deal Talks: NN still sees ‘strong merit’ in a combination of the firms

In FX, the Bloomberg Dollar Spot Index was down 0.2 percent. The yen rose 0.1 percent to 108.95 per dollar, but is still down more than 3 percent since Trump’s victory. The euro strengthened 0.3 percent against the dollar, halting an eight-day losing streak. The pound gained for the first time in four days as figures from the Office for National Statistics showed U.K. spending remained robust despite the Brexit vote. Malaysia’s ringgit fell for a seventh day, its longest stretch of losses in more than a year. Bank Negara Malaysia said Wednesday it will continue to restrict speculative activity in the currency market. The Vietnamese dong fell for a fourth day to a five-month low. “I’m just seeing this as overall dollar strength,” said Wu Mingze, a foreign-exchange trader in Singapore at INTL FCStone Inc., a Nasdaq-listed global payments-service provider. “Unfortunately speculators will treat Bank Negara’s statements as a sign of weakness if they do not actually do something.”

In commodities, crude gained 0.4 percent to $45.76 a barrel in New York as Saudi Arabia and some other OPEC nations meet with Russia for informal talks without oil ministers from Iran and Iraq, the two countries that pose the biggest hurdle to an output deal. Russia will hold discussions with representatives from the Organization of Petroleum Exporting Countries in Doha from Thursday, Energy Minister Alexander Novak said. There’s a high chance of an agreement and Russia is ready to support a decision, he said. Copper traded near a 17-month high in Shanghai. Jiangxi Copper Co., China’s top producer, agreed to cut processing fees for next year as mine supply is poised to be little changed and Chinese smelting capacity expands. Gold has stabilized after its U.S. election thrashing and is on course to end the week little changed, even as investors bail from bullion-backed exchange-traded funds. Prices for immediate delivery climbed 0.4 percent to $1,229.84 an ounce.

On today's economic calendar, the key data to watch will be the October inflation report with headline CPI expected to tick up (+0.4% mom expected; +0.3% previous). In terms of labour market data we will get the initial jobless claims numbers for last week (257k expected; 254k previous) and the continuing claims from the week before (2030k expected; 2041k previous). We will also see the Housing starts (1156k expected; 1047k previous) and the Building Permits numbers (1195k expected; 1225k previous) for October, and finally round out the day with the Philadelphia Fed PMI for November (7.8 expected; 9.7 previous). Away from data, we continue on a busy week for Fedspeak. As already noted above, Fed Chair Yellen will testify before the Joint Economic Committee today – the first time we’ll hear from her following the US elections. We will also hear from Brainard in New York. The other event to note for today is the scheduled meeting between US President-elect Trump and Japanese PM Abe.

US Event Calendar

- 8:30am: Housing Starts, Oct., est. 1.156m (prior 1.047m)

- 8:30am: CPI m/m, Oct., est. 0.4% (prior 0.3%)

- 8:30am: Initial Jobless Claims, Nov. 12, est. 257k (prior 254k); Continuing Claims, Nov. 5, est. 2.030m (prior 2.041m)

- 8:30am: Philadelphia Fed Business Outlook, Nov., est. 7.8 (prior 9.7)

- 9:45am: Bloomberg Economic Expectations, Nov. (prior 45)

- Bloomberg Consumer Comfort, Nov. 13 (prior 45.1)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

* * *

DB's Jim Reid concludes the overnight wrap

Today the Trump story advances further with the President elect meeting his first world leader post the election with Japan's Abe passing through town. We'll also see Fed Chair Yellen testify before the Joint Economic Committee today – note that this is the first time we’ll hear from her following the election. We think her prepared remarks will be out at 8am EST. So potential for headlines from both events. It was also interesting that late last night Fox's Maria Bartiromo suggested that the crucial US Treasury secretary role will be decided today (announced tomorrow) and is down to a choice between Jamie Dimon of JPM and Steve Mnuchin. The fact that Jamie Dimon is still in the race after his public comments downplaying his desire for the role would be a surprise to many but he would certainly be another appointment that Wall Street would appreciate. Indeed both potential candidates are Wall Street veterans. So one to watch over the next two days.

The most interesting news overnight is that the BoJ has announced its first operations to purchase an unlimited amount of bonds at a fixed rate following 10-year JGB yields turning positive earlier this week for the first time since the BoJ announced their desire to peg them near zero. They are carrying out two operations, one in 1-3 year maturities and another in the 3-5 year part of the curve. The operation received no bids but its the first sign that they are prepared to intervene. 10 year yields have edged back a fraction through zero as we type having traded as high as 0.035% yesterday.

As we discussed yesterday if the BoJ is serious about defending their targets in the face of rising global yields then we effectively have cross border helicopter money but with the helicopters dropping money printed in Japan over the US given Trump's fiscal agenda. It's an interesting backdrop to today's meeting of the respective leaders. Trump might end up being very grateful for Japanese policy as it could help hold global yields down more than they would have been without it. Elsewhere Asian markets are relatively quiet with very little movement of note although I admit I might be too tired to spot anything significant even if there was.

A similar story was seen yesterday as markets continue to settle a little after a frenetic past week. The STOXX 600 (-0.20%) and S&P 500 (also -0.2%) both dipped though. US banks were the worst performing US sector yesterday (-2.1%), finally running out of steam following a strong post-election rally. The Dow (-0.32%) was also down for the first time since the beginning of last week.

Over in currency markets, the US dollar continued its post-election rally by gaining +0.3% and quickly erasing yesterday’s dip. Commodity markets were broadly down, with WTI and Brent falling by -0.7% and -1.0% respectively and copper down -0.6%. Gold was marginally lower on the day as it continued its string of losses (down -4.4% since the beginning of last week).

European credit markets were also down as iTraxx Main and Crossover both widened by +1bps on the day. Over in the US we saw CDX IG hold steady while CDX HY widened by +5bps on the day.

Turning to the other end of the risk spectrum, German 10Y yields dropped by -1bps on the day while US 10Y yields saw some big intraday swings that saw yields rise and fall by nearly +8bps and -2bps respectively before ending the day flat. The US curve also flattened somewhat as the US 2Y ticked up +1bp while the 30Y dropped by -4bps. Markets in general continue to price in a December Fed hike with near certainty, with the implied probability around 94% (unchanged from yesterday).

On the topic of rate hikes, one of the key questions surrounding Trump’s unexpected election victory last week was regarding the impact his policies may have on the Fed in the year ahead. DB’s GEP team focuses on one specific area of this issue – what appropriate Fed policy would look like given Trump’s policy mix. They find that a much faster pace of rate hikes are certainly implied under the new administration – even under a relatively conservative assessment the team finds that Yellen's preferred Taylor rule would imply that the Fed should pursue one more rate hike next year than they currently expect. Under a more optimistic scenario (in which US growth rises to around 3% in 2017) the appropriate fed funds rate would be about 75bp higher than the Fed's current expectations. However, the team notes that while a substantially faster pace of rate hikes in 2017 is a risk, this is not their base case: they believe inflation is likely to moderate early next year and the full growth benefits of Trump’s policies may not begin to be felt until the second half of the year. Hence, the Fed is likely to initially keep to their expectations for a gradual pace of rate increases, with the greater risk for faster rate hikes in late-2017 and 2018.

Another key topic of focus following Trump’s victory has been the potential for increased fiscal spending in the US – particularly infrastructure spending. While such a policy is largely expected to prove to be growth positive, there are also fears regarding how such unfunded spending may be possible without damaging the government’s fiscal position. However, a Bloomberg news story yesterday noted that the Trump administration is exploring ways of establishing an ‘infrastructure bank’ to fund such planned infrastructure investments. Depending on its structure, such an entity could potentially provide a way to accommodate increased spending and investment while managing the impact on the government balance sheet. Trump’s policy mix so far has had its share of unknowns (note the campaign team derided a similar policy from Clinton) and so this development might be worth following.

Another piece of political news out yesterday was that Emmanuel Macron officially confirmed his plan to run for French presidency as an independent. While Macron’s candidacy for next year’s election was expected, it does introduce further uncertainty into the race as it may further fragment the electorate. DB’s France economist Marc de-Muizon discussed Macron’s potential candidacy (among other political issues) in a report published last month and noted that his position was more difficult than his high popularity ratings suggested.

Taking a look now at some of the data out today, we saw the September and October employment report from the UK which was a bit of a mixed bag. The ILO unemployment rate for September came in marginally better than expected at 4.8% (vs. 4.9% expected; 4.9% previous). However there remain signs that the labour market may be cooling as the employment change numbers for September came in below expectations at 49k (vs. 91k expected; 106k previous) and jobless claims numbers for October ticked up to 9.8k (vs. 2.0k expected) with September being revised up to 5.6k as well (0.7k before revision). Average weekly earnings growth for September was unchanged and marginally below expectations at +2.3% (vs. +2.4% expected; +2.3% previous).

In the US data slightly disappointed. Wholesale prices for October were unexpectedly unchanged on the month (PPI +0.0% mom) and below expectations of a +0.3% increase. Industrial production was flat and below expectations in October (+0.2% expected), while the September number was revised down to -0.2% (vs. +0.1% before revision). Capacity utilization in October also ticked down and came in marginally below expectations at 75.3% (vs. 75.5% expected; 75.4% previous). The NAHB housing market index for November however did hold stable and come in as expected at 63.

Looking at the data calendar for the day ahead now, we kick off in France where we get the Q3 employment numbers, with the headline unemployment rate (9.9% expected; 9.9% previous) expected to remain unchanged. Thereafter we turn to the UK where we will see the October retail sales numbers (+0.4% mom expected; 0.0% previous). Thereafter we will see the final October CPI numbers for the Eurozone where no revisions are expected (+0.5% YoY expected).

Over in the US, the key data to watch will be the October inflation report with headline CPI expected to tick up (+0.4% mom expected; +0.3% previous). In terms of labour market data we will get the initial jobless claims numbers for last week (257k expected; 254k previous) and the continuing claims from the week before (2030k expected; 2041k previous). We will also see the Housing starts (1156k expected; 1047k previous) and the Building Permits numbers (1195k expected; 1225k previous) for October, and finally round out the day with the Philadelphia Fed PMI for November (7.8 expected; 9.7 previous).

Away from data, we continue on a busy week for Fedspeak. As already noted above, Fed Chair Yellen will testify before the Joint Economic Committee today – the first time we’ll hear from her following the US elections. We will also hear from Brainard in New York. The other event to note for today is the scheduled meeting between US President-elect Trump and Japanese PM Abe.