Perspectives Pictet

Perspectives Pictet

German activity has accelerated in the first quarter of the year on the back of a strong domestic economy.German GDP rose by 0.4% quarter-on-quarter in Q1, accelerating from a flat figure in Q4.The strong Q1 GDP growth is good news and confirms our long-held view that domestic demand remains resilient despite many external headwinds.The signal given by other data (factory orders, surveys) suggests that some negative payback is likely in Q2.The prospect of higher German growth (on average) in...

Read More »Do not hesitate to contact Pictet for an investment proposal. Please contact Zurich Office, the Geneva Office or one of 26 other offices world-wide.

A premium mode of transport for urban commuters

Technological innovations offer a Swiss solution to modern traffic problems in the form of a powerful e-bike capable of long-distance, high-speed urban commuting with full connectivity modelled on global brands such as TeslaSwitzerland may not feature on lists of the world’s leading carmakers, but it is home to the manufacturer of a state-of-the-art form of commuter transport. Stromer battery-powered e-bikes, made in the small village of Oberwangen near Bern, are capable of travelling...

Read More »Core sovereign bond yields – update

We are adjusting downward our year-end targets for the 10-year US Treasury and Bund yields.Taking hold of two important changes to our central macroeconomic scenarios, we are adjusting downward our year-end target for the 10-year US Treasury yield from 3.0% to 2.8% and the Bund yield from 0.5% to 0.3%. The drivers behind this include lower inflation expectations, rising US-China trade tensions against a constant monetary policy backdrop.Four consecutive disappointing US inflation prints have...

Read More »US-China trade: New tariffs – watch the second derivative

Our view about US-China trade tensions remains largely unchanged. We expect limited direct impact on the US economy, but the indirect costs could be more significant.The direct macro cost on the US economy of the raised tariffs to 25% from 10%, and the fresh counter-tariffs from China, should be limited in our view, at around 0.1% of US GDP.The US economy tends to be much more sensitive to financial conditions than to the narrow question of the tariffs’ impact on end-purchasers in the US....

Read More »Weekly View – Game of chicken

The CIO office’s view of the week ahead.As a US-China trade negotiation impasse became evident last week, markets corrected a bit, particularly cyclical sectors. Given the strong US economy, Trump is feeling empowered to pursue his agenda, raising existing tariffs from 10-25% on USD 200bn worth of goods with immediate effect and threatening more. Now we will wait to see how China retaliates. For the time being, we feel assured that the Chinese authorities will not use currency or its US...

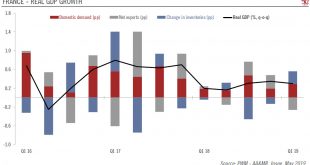

Read More »French tax cuts designed to reboot Macron’s presidency

The French government’s response to the ‘yellow vest’ protests could provide a meaningful boost to consumer spending, mostly next year.Following a series of townhall meetings with French citizens up and down France, President Emmanuel Macron responded to social unrest with two doses of fiscal easing. The December package (worth EUR10bn) was incorporated in the stability plan sent to Brussels before Easter and is included in the 3.1% public deficit planned for this year. The measures...

Read More »What we are watching for now

[embedded content] Equity markets have reached new highs, extending the longest bull market in US history. However, César Pérez Ruiz, Head of Investments and CIO at Pictet Wealth Management, is conscious of complacency in markets and keeping protection on portfolios as tail risks remain. Geopolitical developments such as the potential escalation of Iranian tensions and drawn-out trade negotiations between the US and China, could send short-term volatility through markets.

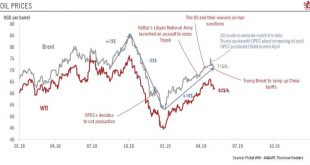

Read More »Oil prices decline despite the end of Iran waivers

We believe prices will remain volatile in the short term, before a possible oil glut becomes an issue toward year’s end.The increase in prices that followed President Trump’s 22 April decision to end waivers on Iranian oil imports did not last, with Brent prices falling from almost USD75 on 24 April to below USD70. Nonetheless, we continue to see heightened risk of oil price spikes above USD80 for Brent in the short-term.Trump’s recent threat to increase US tariffs on Chinese imports could...

Read More »A spanner in the works

While Trump’s weekend tweets have created fresh uncertainties around US trade talks with China, some perspective is needed.At the weekend, US President Trump threatened to increase the tariff rate on Chinese imports as he believes that US-China trade negotiations are going “too slowly”. Importantly, Trump’s threats do not mean bilateral talks are breaking down. Indeed, the Chinese government confirmed today that its trade delegation would still go to Washington DC this week for another round...

Read More »Weekly View – The final countdown

The CIO office’s view of the week ahead.Last week markets were relatively muted, with commodities down, developed markets flat and emerging markets up slightly. That brief period of calm has already ended, with Trump’s Sunday tweets sending Chinese markets sharply down on Monday. With the Chinese scheduled to attend the next round of trade negotiations in the US on Wednesday, the US president is putting extra pressure on China to concede to US demands and seal a deal through threats to...

Read More »