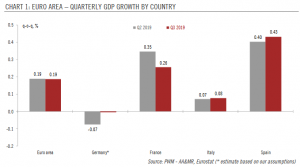

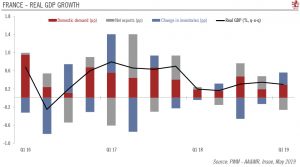

According to Eurostat’s preliminary figures, euro area GDP grew by 0.2% quarter on quarter in Q3, the same pace as in Q2 and in line with our expectations.

Country wise, France, Italy and Spain grew at the same pace in Q3 as in Q2. In particular, household and investment spending grew at a solid pace in both France and Spain. The preliminary GDP figure for Germany will not be released until 14 November. But based on the country data released so far and assuming stable growth for other euro area countries that have not yet published their Q3 estimates, we think German GDP was broadly flat in Q3. Risks are nevertheless tilted to the downside and even if Germany avoids a ‘technical recession’ (two consecutive quarters of negative growth), the country’s economy is

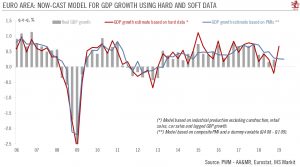

Steady euro area growth and rise in core inflation

November 4, 2019