Perspectives Pictet

Perspectives Pictet

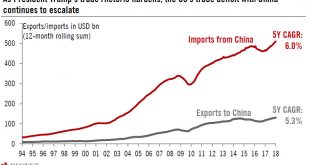

CEO sentiment reaches a record high, but protectionist tendencies could impact confidence down the road.US businesses are feeling good – in fact, they are borderline euphoric. The latest evidence comes from the quarterly Business Roundtable CEO economic outlook index, a survey of 137 CEOs, conducted in February, which rose to its highest level since the survey began 15 years ago. All three sub-indices (capex, employment, sales) rose to fresh highs.Particularly encouraging was the sharp rise...

Read More »US chart of the week – Corporate euphoria