Perspectives Pictet

Perspectives Pictet

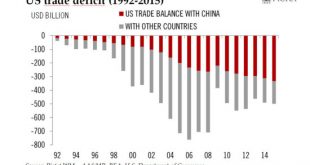

There is a high risk that tensions between the US and China over the latter’s rise are set to come to a head under Trump’s presidency and become an important source of market volatility.The relationship between the US and China is of vital importance for the world both from an economic and a geopolitical perspective. Competition between the two powers could be set to come to a head under Donald Trump’s presidency. First, the trade relationship with China is a central issue in the Trump...

Read More »U.S.-China: Trump’s new approach risks a dangerous confrontation