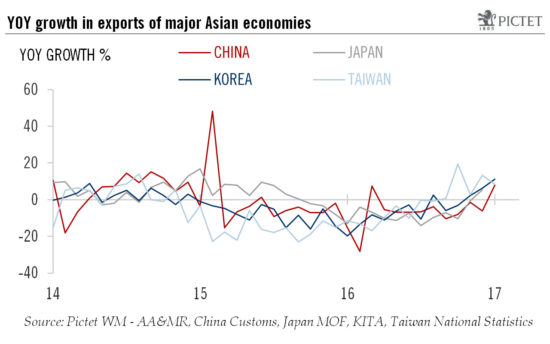

Fourth straight quarter of growth poses upside risk to our Japanese GDP forecast.The first preliminary reading of Japan’s real GDP growth for Q4 2016 came in at 1% q-o-q annualised, roughly in line with the consensus forecast of 1.1% but below the 1.3% growth in Q3. The growth in Q4 almost all came from external demand (+1.0%), while the contribution from domestic demand was virtually 0%. Japanese exports have shown clear signs of improvement in recent months, consistent with the export recovery in broad Asia since H2 2016.The stronger performance of Japan’s export/manufacturing sector in recent months poses upside risk to our Japanese GDP forecast for 2017, which currently stands at 0.8%. As the Q4 GDP figures indicate, exports and domestic production give clear signs of recovery, and the gradual reacceleration in the Japanese economy is likely to persist at least through H1 2017.

Topics:

Dong Chen considers the following as important: Asian exports, Japan, Japan growth forecast, Japanese growth, Macroview

This could be interesting, too:

Marc Chandler writes US Dollar is Offered and China’s Politburo Promises more Monetary and Fiscal Support

Marc Chandler writes US-China Exchange Export Restrictions, Yuan is Sold to New Lows for the Year, while the Greenback Extends Waller’s Inspired Losses

Marc Chandler writes Yen Jumps on Rate Hike Speculation

Marc Chandler writes Trump’s Tariff Talks Wobble Forex Market, Close Neighbors Suffer Most

Fourth straight quarter of growth poses upside risk to our Japanese GDP forecast.

The first preliminary reading of Japan’s real GDP growth for Q4 2016 came in at 1% q-o-q annualised, roughly in line with the consensus forecast of 1.1% but below the 1.3% growth in Q3. The growth in Q4 almost all came from external demand (+1.0%), while the contribution from domestic demand was virtually 0%. Japanese exports have shown clear signs of improvement in recent months, consistent with the export recovery in broad Asia since H2 2016.

The stronger performance of Japan’s export/manufacturing sector in recent months poses upside risk to our Japanese GDP forecast for 2017, which currently stands at 0.8%. As the Q4 GDP figures indicate, exports and domestic production give clear signs of recovery, and the gradual reacceleration in the Japanese economy is likely to persist at least through H1 2017.