Frederik Ducrozet

September 7, 2017

Perspectives Pictet

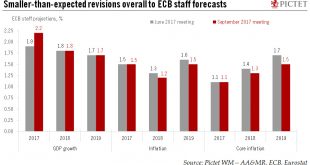

In spite of euro strength, a decision on tapering QE will likely come in October. We believe a reduction in monthly asset purchases could commence in H1 2018.The ECB left its assessment and communication broadly unchanged at its meeting on 7 September. Draghi confirmed that “the bulk of the decisions” on QE extension should be made at the 26 October meeting.The statement mentioned recent currency volatility as “a source of uncertainty” to be monitored in the future, and the staff...

Read More »

Thomas Costerg

September 6, 2017

Perspectives Pictet

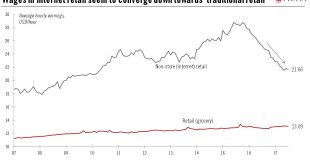

The US labour market is tight, but wage growth remains relatively muted. Trends in e-retailing may provide part of the explanation.The US economy is challenging ‘textbook’ macroeconomics. The labour market is tight, but wage growth is paltry. Growth is chugging along steadily and the output gap (the difference between actual GDP and its theoretical trajectory at full potential) is gradually closing, but inflation remains muted.Clues as to why things are not panning out the way theory suggest...

Read More »

Nadia Gharbi

September 5, 2017

Perspectives Pictet

The SNB is unlikely to pre-empt the ECB in normalising monetary policy. We are keeping our baseline scenario unchanged and expect the interest on sight deposit to stay at -0.75%.The SNB’s 14 September meeting could be one of the most interesting in a while, as it comes just after a period when the Swiss franc has witnessed significant depreciation, mainly against the euro.The key focus of the SNB’s September 14 meeting will be its assessment of exchange rate moves. We do not expect the SNB...

Read More »

Luc Luyet

September 4, 2017

Perspectives Pictet

The upcycle in the US dollar that began in 2011 has faded, but further depreciation of the greenback may be limited and there is a good chance of a near-term recovery against the euro.The US dollar index has declined significantly this year, challenging our constructive view on the US dollar. Disappointment regarding potential US tax reform, the decline in US inflation, the significant overvaluation of the greenback and strong economic recovery in the rest of the world all help explain a...

Read More »

Thomas Costerg

September 1, 2017

Perspectives Pictet

Underlying trends in the labour market are unlikely to deter the Fed from a further rate hike in December.Non-farm payrolls (NFPs) rose 156,000 in August, bringing the three-month average to a still-robust 185,000/month. The three-month average stands higher than the 12-month average of 175,000, suggesting that underlying momentum in the US labour market – and the broader economy – remains healthy. The unemployment rate increased marginally (+0.1%) to 4.4%, but this remains within the...

Read More »

Frederik Ducrozet

September 1, 2017

Perspectives Pictet

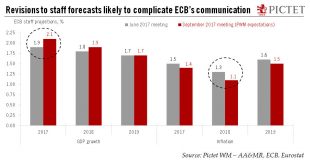

The ECB’s Governing Council meeting on 7 September may see the first tentative steps toward an unwinding of QE, with a firm announcement on policy to come in October.The ECB will likely prepare for a cautious, flexible, slow-motion exit at its Governing Council meeting on 7 September, tasking its committees to study all policy options for 2018. We continue to expect an announcement in October that quantitative easing (QE) will be extended for six months, but at a reduced pace of EUR40bn per...

Read More »

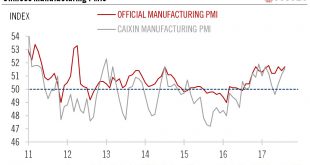

Dong Chen

September 1, 2017

Perspectives Pictet

August manufacturing PMI showed solid industrial activity, while domestic demand is holding up well. We are keeping our Chinese GDP forecast unchanged.China’s official manufacturing PMI in August came in at 51.7, rising slightly from July (51.4), and remaining firmly in expansionary territory. The Markit PMI extended its ascendance for the third consecutive month to reach 51.6 in August.Domestic demand seems to be holding up well. The production, new orders and imports sub-indices of the...

Read More »

Frederik Ducrozet

August 31, 2017

Perspectives Pictet

A close look at recent data suggest that core inflation in the currency area is edging higher, supporting the ECB ‘s plans for policy normalisation.Euro area flash HICP inflation rose to 1.5% y-o-y in August from 1.3% in July, while core inflation remained stable at 1.2% year on year. In our opinion, modest upward price momentum has started to build over the past few months, with core inflation likely to edge slightly higher from here.Euro area core inflation has broken out of the tight...

Read More »

Thomas Costerg

August 31, 2017

Perspectives Pictet

US companies are showing little propensity to use healthy profits to increase their investments. We remain prudent about the outlook for US capex in the coming months.A major feature of the US growth recovery since mid-2009 has been the significant improvement in corporate profits. But improvement has been mostly achieved at the expense of investment (capex) and wage growth, which have been kept on a tight leash. This has puzzled policymakers, including the Federal Reserve, which has been...

Read More »

Dong Chen

August 31, 2017

Perspectives Pictet

The growth in retail sales slowed slightly in July, but a strong labour market and the rise in aggregate wages should continue to boost consumer spending.Following a strong rebound in Q2, the momentum behind consumer spending in Japan seems to have moderated somewhat in July. Retail sales in Japan grew by 1.9% y-o-y, down slightly from 2.2% in June and 2.5% in Q2.Despite the softer momentum, the recovery in Japan’s consumer sector, which started roughly in the second half of 2016, may...

Read More »

Perspectives Pictet

Perspectives Pictet