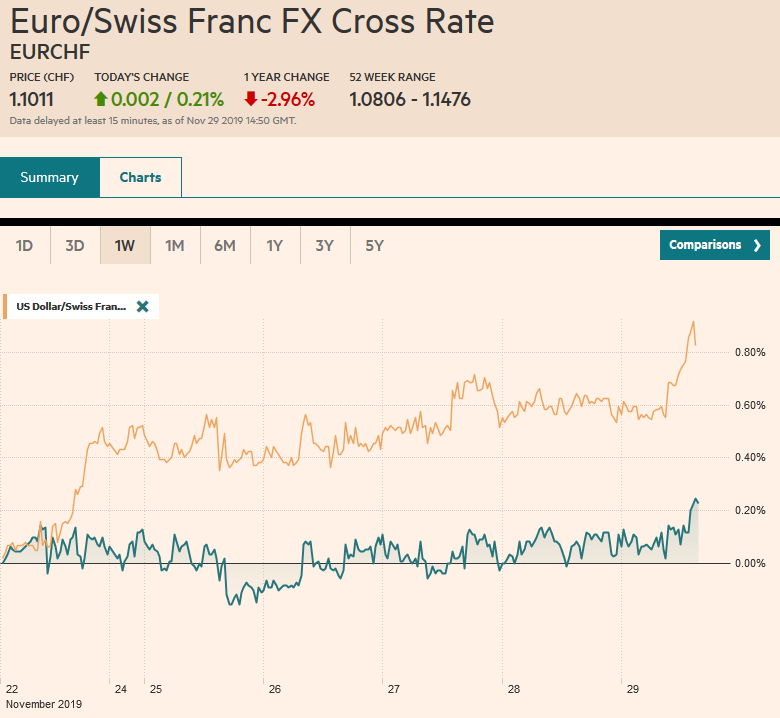

Swiss Franc The Euro has risen by 0.21% to 1.1011 EUR/CHF and USD/CHF, November 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Global equities are trading heavily. Both the MSCI Asia Pacific and the Dow Jones Stoxx 600 snapped four-day advancing streaks yesterday and have seen some follow-through selling today. In the Asia Pacific region, all the markets fell but Jakarta. Hong Kong’s Hang Seng slipped a little more than 0.2% yesterday but dropped 2% earlier today to record its biggest decline in three weeks. European shares opened lower after the Dow Jones Stoxx eased 0.15% yesterday but steadied as the European morning progressed. With US markets closed yesterday, the S&P 500’s four-day advance will be

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, Brexit, Chile, Featured, Hong Kong Canada, newsletter, Poland, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Krypto-Ausblick 2025: Stehen Bitcoin, Ethereum & Co. vor einem Boom oder Einbruch?

Connor O'Keeffe writes The Establishment’s “Principles” Are Fake

Per Bylund writes Bitcoiners’ Guide to Austrian Economics

Ron Paul writes What Are We Doing in Syria?

Swiss FrancThe Euro has risen by 0.21% to 1.1011 |

EUR/CHF and USD/CHF, November 29(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Global equities are trading heavily. Both the MSCI Asia Pacific and the Dow Jones Stoxx 600 snapped four-day advancing streaks yesterday and have seen some follow-through selling today. In the Asia Pacific region, all the markets fell but Jakarta. Hong Kong’s Hang Seng slipped a little more than 0.2% yesterday but dropped 2% earlier today to record its biggest decline in three weeks. European shares opened lower after the Dow Jones Stoxx eased 0.15% yesterday but steadied as the European morning progressed. With US markets closed yesterday, the S&P 500’s four-day advance will be challenged today. There is a small gap from Wednesday’s high opening (~3142.7-3143.4) that may attract prices. US and European benchmark 10-year yields have slipped a little though yields in Japan and Australia edged up. The foreign exchange market is subdued, and the dollar still enjoys a firm tone. Only the Antipodeans and the Swedish krona are stronger. The dollar has been confined to a 15-pip range against the yen, and the euro is in a little more than a 10-pip against the dollar. The JP Morgan Emerging Markets Currency Index is slightly higher, ending a five-day decline. Gold is little changed but has succeeded in holding above important chart support around $1450 this week. The price of January WTI is off about 0.3%, which halves this week’s gain and sees it straddle the $58 a barrel level. |

FX Performance, November 29 - Click to enlarge |

Asia PacificThere was little doubt that Japan’s economy was going to pay back for the strong performance in production and consumption seen in September ahead of the sales tax. Yesterday it reported retail sales plummeted 14.4% in October. Economists had anticipated a little more than a 10% drop after a 7.2% surge (initially 7.1%) in September. Today, Japan reported a 4.2% contraction in industrial output in October after a 1.7% gain in September. Interestingly, November’s consumer confidence rose to 38.7 from 36.2. The Bank of Japan meets December 19 but is not expected to respond with a change in policy, but the Abe government could increase the size of the supplemental budget it is proposing. |

Japan Unemployment Rate, October 2019(see more posts on Japan Unemployment Rate, ) Source: investing.com - Click to enlarge |

South Korea reported that October industrial output fell 1.7%. The market had been looking for less than a 0.5% decline after a 2.0% gain in September. The central bank trimmed its 2019 and 2020 GDP forecasts but left policy on hold (1.25%) and suggested the economy may be bottoming. Separately, North Korea has been active, testing multiple rocket launchers and some short-term ballistic missiles.

The dollar reached a six-month high of JPY109.60 in the middle of the week. The longest rally of the year (six sessions) ended yesterday with a minor (~three pip) decline and it is a 15-tick range today below the midweek high. There is an option for $540 mln at JPY109.35 that rolls off today. The next important chart area is JPY110.00. The Australian dollar fell to new lows since the middle of October yesterday, near $0.6760. It has stabilized today in quiet, uneventful activity and needs to resurface above $0.6800 be meaningful, and without pushing above $0.6785, it will extend its weekly losses for the fourth week. The yuan rose four of this week’s five sessions, and today’s almost 0.25% gain is the largest in three weeks. The dollar slipped below CNY7.02 for the first time since November 18.

EuropeAnother controversy over antisemitism hobbles the Labour Party, which does not appear to be running a strong campaign. YouGov warns that Labour may not pick up any more seats and may lose as many as 30 seats in which a Labour MP represents a district that voted to Leave in the 2016 referendum. The Liberal Democrats remain marginalized, and YouGov poll shows them winning less than 15 seats. The Brexit Party is projected not to win any seats. Sterling reached a five-day high on Thursday, near $1.2950, retreated back to $1.29. It remains mired in a $1.28-$1.30 range as it has more or less since mid-October. |

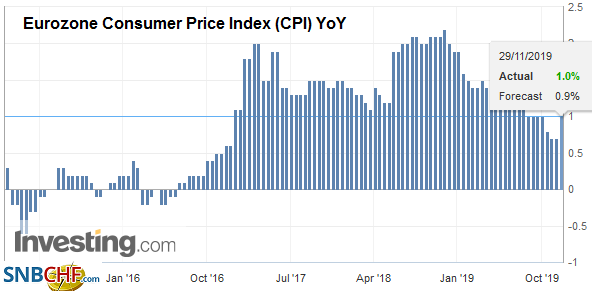

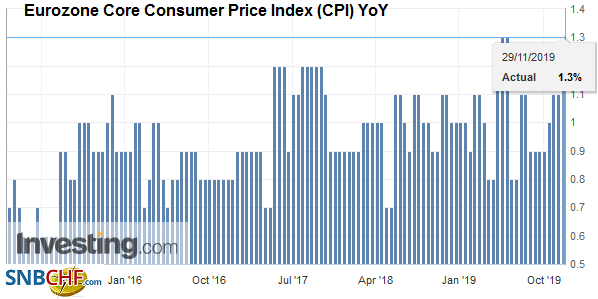

Eurozone Consumer Price Index (CPI) YoY, November 2019(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| The eurozone reported its preliminary estimate for November CPI rose more than expected. The 1.0% year-over-year headline rise compares with 0.7% in October and expectations for a 0.9% pace. The core rate rose to 1.3% from 1.1%, which is also a little more than expected. The key here is the base effect, and as we have noted before, it is favorable through January. |  |

| Separately, Germany surprised by a decline in November unemployment queues, which slimmed by 16k. Economists had expected a 6k increase. It was the biggest decline since February but left the unemployment rate steady at 5%. On the other hand, October retail sales slumped 1.9%, Economists had looked for a 0.2% increase. It is the biggest decline of the year and the first since July. The EMU reports the region’s figures next week, and there is a downside risk form the flat forecast after Germany’s report. |

. |

Sweden’s economy expanded by 0.3% in Q3, which was a little better than expected, and Q2 growth was revised to 0.2% from 0.1%. It increases the chances that the Riksbank will hike rates to zero at its December 19 meeting. The central bank had signaled its intention, but mixed data and global risks had made some investors cautious. Still, the krona has strengthened against the euro by more than 1% this week and has gained in six of the last seven weeks. The euro recorded a 10-year high in mid-October over SEK10.93 and today is near SEK10.50, a four-month low.

The Polish zloty has been under pressure lately against both the dollar and euro. Losses accelerated after Poland’s top court issued its latest ruling yesterday on the Swiss franc mortgages, which have bedeviled the Polish banks for years. They have about PLN104 bln ($~$25 bln) of Swiss franc mortgages, which were sold to homeowners who wanted to lock in low-interest rates. The cost of the sharp appreciation of the franc has been a political and legal hot potato. The court ruled that the loans could be converted into zloty without invalidating them while the interest the borrowers pay would continue to be linked to Swiss rates, which are well below Poland’s. Although it was a decision in one case, a broader application is a reasonable expectation. Bank shares sold off 3-4% yesterday as the bank provisions may have to be boosted to cover the franc-denominated loans, not just the indexed-loans, but has stabilized today.

The euro is stuck near its recent trough around $1.10, where a nearly 740 mln euro option has been struck that expires today. Yesterday’s high was near $1.1020, and the week’s low, set on Wednesday, was just above $1.0990. Sterling peaked yesterday near $1.2950 after positing an outside up day in the middle of the week. However, it has struggled to sustain the upside momentum and, instead, faded back toward $1.2880 today. There is a GBP385 mln option at $1.29 that will be cut today. Sterling is in the middle of the $1.28-$1.30 range that has dominated activity since the mid-October.

America

President Trump signed the two bills that passed with nearly unanimous support in Congress. It was a calculated risk. The executive branch controls the implementation, as Congress defers its authority to regulate commerce. China’s vague threats have been discounted. It threatened retaliation after the US sold advanced weapons to Taiwan, sanctioned Chinese companies over human rights violations, and blacklisting Huawei. Trump did not have to sign the bills. If he did nothing, the bills would have become laws anyway. He did so because the domestic advantages outweighed the risk that it would derail the trade talks. In fact, confidence that a trade deal was in the “final throes” or “millimeters” away as the White House claimed, with speculation that an agreement is possible in the coming days, discouraged a more significant wave of profit-taking in equities or the dollar.

Earlier this week, Brazil intervened in the foreign exchange market to support the real that had fallen to new record lows. The dollar fell 1% against the Brazilian real Thursday. Yesterday, as the Chilean peso fell to record lows (-10.6% this month ahead of today’s local session), the central bank announced it would sell $10 bln (about a quarter of its currency reserves) and offer $10 bln in hedges. It plans on sterilizing the impact of the intervention in its money markets by injecting liquidity via swaps and repo.

The North American calendar is light today with no US data or Fed speakers. The highlight is Canada’s Q3 GDP. Canada is one of the few high-income countries, alongside the UK, that reports monthly GDP estimates. The July (flat) and August (0.1%) already warned that the economy had lost some momentum after the heady 3.7% year-over-year pace in Q2. The median forecast in the Bloomberg survey is that the economy slowed to a 1.3% rate in Q3. The Bank of Canada meets next week, and although it has softened its neutral language, there is practically no expectation for a rate cut. Indeed, judging from the derivatives market, the Bank of Canada is expected to hold steady at least through H1 2020.

The US dollar has trended higher against the Canadian dollar since the late October low near CAD1.3050 to reach a high near CAD1.3330 on November 20. It has been consolidating since, and the trendline drawn off the recent highs is found near CAD1.3310 today. Support is seen around CAD1.3250. Expiring options at CAD1.3250 and CAD1.3350 (for about $600 mln and $685 mln respectively) mark the broad range but do not seem to be in play. The US dollar reached almost MXN19.66 yesterday, its highest level since early October before pulling back. Regional pressure and doubts about AMLO’s domestic agenda took a toll. We look for the dollar to find support near MXN19.40. The greenback is on track to extend its advance of the third consecutive week against the peso and the fourth week out of the past five after falling every week in October.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Brexit,Chile,Featured,Hong Kong Canada,newsletter,Poland