Swiss Economicblogs.org

Swiss Economicblogs.org

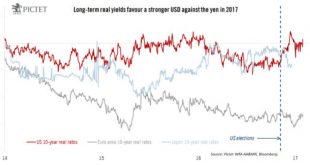

Pictet Wealth Management’s positioning in fast-evolving markets.Asset allocationImproved earnings growth should support attractive returns on developed-market equities.We still expect Treasury yields to rise this year. The 35-year fall in long-term interest rates, during which government bonds provided both strong returns and protection, has probably ended. The protection that government bonds provide for portfolios is therefore set to come at a cost again.Volatility on equity markets is...

Read More »Monthly Investment Strategy Highlights, February 2017