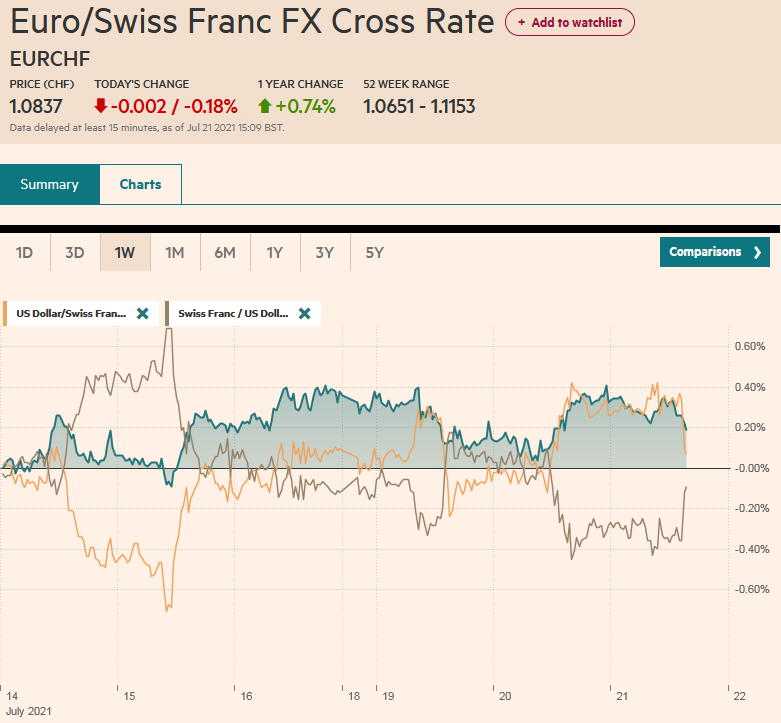

Swiss Franc The Euro has fallen by 0.18% to 1.0837 EUR/CHF and USD/CHF, July 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The biggest rally in US equities in four months has helped stabilize global shares today. In the Asia Pacific region, Japan, China, and Australian markets advanced. Led by information technology and consumer discretionary sectors, Europe’s Dow Jones Stoxx 600 is up around 1.35% near the middle of the session. US equity futures are firm, though the NASDAQ is lagging. The US 10-year yield that briefly dipped below 1.13% yesterday is firm today, around 1.25%, while European bond yields are 1-2 bp firmer. After a poor retail sales report, Australia’s benchmark yield slipped a couple of

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Canada, China, Currency Movement, Featured, infrastructure, Japan, newsletter, Poland, South Korea, Taiwan, U.K., USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.18% to 1.0837 |

EUR/CHF and USD/CHF, July 21(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The biggest rally in US equities in four months has helped stabilize global shares today. In the Asia Pacific region, Japan, China, and Australian markets advanced. Led by information technology and consumer discretionary sectors, Europe’s Dow Jones Stoxx 600 is up around 1.35% near the middle of the session. US equity futures are firm, though the NASDAQ is lagging. The US 10-year yield that briefly dipped below 1.13% yesterday is firm today, around 1.25%, while European bond yields are 1-2 bp firmer. After a poor retail sales report, Australia’s benchmark yield slipped a couple of basis points, which was sufficient to mark a new three-month low (~1.15%). Most of the major currencies are trading slightly heavier against the US dollar. The Scandis and New Zealand dollar are the most resilient today. Emerging market currencies are mostly weaker, leaving the Chinese yuan’s 0.2% gain being the best. The JP Morgan Emerging Market Currency Index has been alternating between up and down sessions since the start of last week. Yesterday’s small advance is being followed by a minor loss today. Gold is heavy, approaching $1800 after being turned back from $1825 yesterday. An unexpected drawdown in US oil inventories, according to API, would be the first since May if confirmed by the EIA later today, maybe helping oil prices recover from Monday’s sharp drop. Initial resistance for the September WTI contract is seen near $68.80 and then $70. |

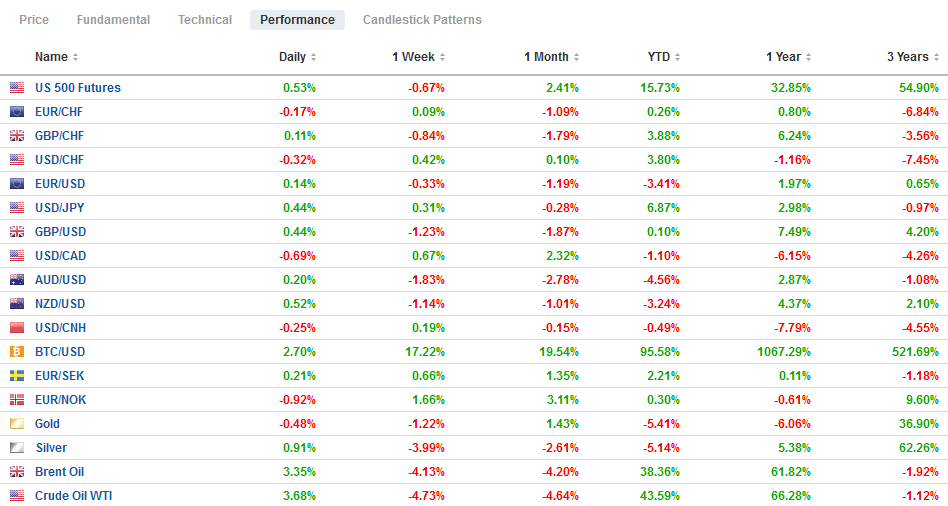

FX Performance, July 21 - Click to enlarge |

Asia Pacific

There appears to be an escalation of posturing and positioning over Taiwan. This week, Taiwan’s first European office under its name opened in Lithuania. Other diplomatic posts are under the name Taipei. Recently, a civilian equivalent of the US’s C-130 transport plane landed in Taiwan. Beijing claims the US military uses civilian aircraft for subterfuge. Military aircraft were used to deliver the vaccines the US donated to Taiwan. Japan has also escalated its position. On July 5, Deputy Prime Minister Aso explicitly went further than Washington and pledged Japan would come to the aid of Taiwan if it were invaded by China. A week later, Japan’s annual security review was published, noting for the first time that stability around Taiwan was a significant part of its security.

This puts the US, which has a defense pact with Japan but not Taiwan, in a precarious position. Does Japan’s pledge commit the US? And if the US has been dealt a fait accompli, does this change Beijing’s calculations? As we have noted, the US “strategic ambiguity” towards Taiwan is meant to deter a unilateral declaration of independence by Taipei than an attempt to keep Beijing off balance. China has been aerially harassing Taiwan, sometimes sending dozens of fighters and bombers into Taiwan’s airspace frequently. Beijing recently signaled by having extensive amphibious landing exercises and war games on nearby islands. Separately, but not unrelated, the UK announced that it will base two naval ships in Asia to help provide a bulwark against Chinese territorial claims in the South China Sea.

Japan’s trade balance always improves in June over May, and this year did not break the strong seasonal pattern. The trade surplus stood at JPY383 bln after a May deficit of JPY189 bln. Auto and auto part exports helped lift overall exports to 48.6% above year-ago levels, inflated by the low base. Still, in H1 21, the average monthly trade surplus was JPY164 bln, compared with a deficit of nearly JPY380 bln last year and a deficit of almost JPY150 bln in 2019. South Korea reported strong exports for the first 20-days in July (32.8%). Exports, adjusted for the number of working days, are up by nearly a quarter over 2019 levels. Semiconductor exports account for about a fifth of overall exports and are being flattered by rising prices as well as volumes.

The dollar bottomed on Monday in front of JPY109, and today see the week’s high so far, slightly above JPY110.15. Resistance is seen in the JPY110.35-JPY110.50 area. The upper end holds an $820 mln option that rolls off today. Note that Japanese markets are closed Thursday and Friday. Australia’s June retail sales were expected to have fallen by 0.7% as the virus spurs local lockdowns. Instead, retail sales fell by 1.8%, the largest decline of the year, and saw the Aussie dip below $0.7300 for the first time this year. It has steadied and resurfaced above $0.7300. It faces resistance in the $0.7330-$0.7345 band. The Chinese yuan has risen by 0.2% against the US dollar. It may not sound like much, but the gain makes the yuan among the strongest currencies so far today, and it is the largest gain here in July. Since around the middle of last month, the dollar has been rangebound between roughly CNY6.45 and CNY6.50. The PBOC set the dollar’s reference rate at CNY6.4835, in line with expectations (CNY6.4831, the median forecast in Bloomberg’s survey).

Europe

Surveys from the UK illustrate some of the challenges facing employers post-Covid. One survey found that UK employees want GBP5.1k raises to return to the office, roughly the cost of the average commuter train ticket. A third of those looking for work expect to work from home at least twice a week. Only 17% say they actively want to return to the office full-time. Nearly half say flexible work is among the most important considerations. Another survey found that about 57% of employees are going to the office.

The EC gave Poland until August to comply with the European Court of Justice ruling that demanded an end to the controversial mechanism that has been installed to punish judges who do not comply with the government led by the conservative Law and Justice Party. However, it is not clear what happens if the Polish government does not capitulate. Recall that a week ago, Poland’s top court ruled that the ECJ overreached in its ruling on the Polish judiciary. The ECJ has been calling for Warsaw to abandon what it sees as encroachment of the judiciary’s independence for over a year. The government says it will review the EC’s written letter. From 2004-2020, Poland has received about 195 bln euros from the EU, and as a member, paid around 62 bln. The 2021-2027 budget projects Poland receiving almost 140 bln euros in subsidies and about 32.5 bln in repayable aid. Access to these funds may be the stick that goes with the carrot.

The ECB’s two-day meeting concludes tomorrow, and the main focus is on adjusting the forward guidance in light of the new symmetrical inflation target. The euro is little changed after slipping to a new four-month low near $1.1750. However, the downside momentum is easing as news appear harder to record and marginal at best. Resistance is seen in the $1.1790-$1.1800 area. For its part, sterling held above yesterday’s low (~$1.3570) and recovered to around $1.3630 in the European morning. The (50%) retracement objective of sterling’s rally since early last November is found near $1.3550. On the topside, the $1.3700 area is key and holds the 200-day moving average.

America

The economic calendar for North America is light today. The focus is on the infrastructure bill that looks to be stuck in the Senate in the US. Sixty votes are needed to begin debate, and they do not seem to be there. The chances of a bipartisan deal are diminishing, leaving the Democrats to push it all into a reconciliation bill that it has the numbers to pass without Republican support. The American fascination with bipartisanship seems rather unique, and in any event, is proving elusive in most areas outside of confronting China.

The number of fully vaccinated people in Canada appears to be edging above the US for the first time. Finance Minister Freeland acknowledged that the re-opening of the economy is taking place a little later than the government anticipated in April. It is willing to extend income support programs to businesses and households beyond the end of September if necessary. In the scenario we have sketched, as the vaccination program accelerated and the economy strengthened, we anticipated Prime Minister Trudeau, who heads a minority government, to call for snap elections. Talk of such is picking up, and a fall timetable seems reasonable. Stay tuned. There had been talk that former Bank of Canada and Bank of England Governor Carney could challenge Trudeau in the Liberal Party. Carney denied such intentions yesterday.

The US dollar is continuing to retrace its outsized gain scored against the Canadian dollar on Monday (~1.1%). It recouped almost half yesterday and is edging lower today. Monday’s low was set near CAD1.2600, and the 200-day moving average is a little higher, closer to CAD1.2625. A move below CAD1.2570 would boost the chances that a high is in place. There is an option for about $510 mln at CAD1.2700 that expires today. The session high so far was set in Asia near CAD1.2730. Initially, the greenback’s gains against the Mexican peso were extended to MXN20.2170, a new one-month high and the 200-day moving average. However, it is better offered in Europe and is below MXN20.12 as the North American session prepares to open. Initial support is seen in the MXN20.00-MXN20.05 area.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

SNB Sight Deposits: Inflation is there, CHF must Rise

SNB Sight Deposits: Inflation is there, CHF must Rise

2021-07-19

Sight Deposits have risen by +0.2 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, July 13: Headline US CPI may Decline for the First Time in a Year

FX Daily, July 13: Headline US CPI may Decline for the First Time in a Year

2021-07-13

New record highs in the US S&P 500 and NASDAQ coupled with China allowing Tencent to acquire a search engine helped lift Asia Pacific equities. It is the first back-to-back by MSCI’s regional index for more than two weeks. Australia’s market was a notable exception.

FX Daily, July 02: US Jobs and OPEC+ Day

FX Daily, July 02: US Jobs and OPEC+ Day

2021-07-02

The US jobs report and OPEC+ decision are awaited. The dollar remains bid. Only the yen and Canadian dollar are showing a hint of resilience, though, on the week, the Scandis and dollar-bloc currencies are off between around 1-2%. The greenback is also firmer against the emerging market currency complex, and the JP Morgan index is off for the sixth consecutive session.

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

2021-06-10

The ECB meeting and the US May CPI report is at hand. The US dollar is consolidating at a higher level against most of the major currencies. Softer than expected, inflation readings are weighing on the Scandis, which are bearing the brunt. The US 10-year yield closed below 1.50% for the first time in three months yesterday, and this may have helped underpin the Japanese yen.

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

2021-06-08

The capital markets appear to be in a holding pattern ahead of this week’s big events, including the US CPI and the ECB meeting. Equities are little changed but with a heavier bias evident. Most of the large bourses in the Asia Pacific region were lower, except Australia, which eked out a small gain.

FX Daily, May 28: The Yuan Extends Gains, While Sterling’s First Close above $1.42 in Three Years Goes for Nought

FX Daily, May 28: The Yuan Extends Gains, While Sterling’s First Close above $1.42 in Three Years Goes for Nought

2021-05-28

The recovery of the US 10-year yield, so it is flat on the week near 1.61% coupled with month-end demand, is helping the US dollar firm. While the yen is bearing the burden on the week, with a 0.8% loss, the Antipodeans are leading the downside on the day.

FX Daily, May 27: Narrow Ranges in FX Prevail Amid Month-End Considerations

FX Daily, May 27: Narrow Ranges in FX Prevail Amid Month-End Considerations

2021-05-27

Dollar demand linked to the month-end gave the greenback a bit of a reprieve, helped by firmer bond yields. Some momentum players may have been forced out of the euro and yen when the $1.22 and JPY109 levels yielded. However, follow-through dollar buying has been limited, and it has come back a little softer but broadly so.

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

2021-05-12

The markets remain on edge. Asia Pacific and US equities have yet to find stable footing, and inflation fears are elevated. The foreign exchange market has turned quiet as the dollar consolidates its recent losses.

Tags: #USD,Canada,China,Currency Movement,Featured,infrastructure,Japan,newsletter,Poland,South Korea,Taiwan,U.K.