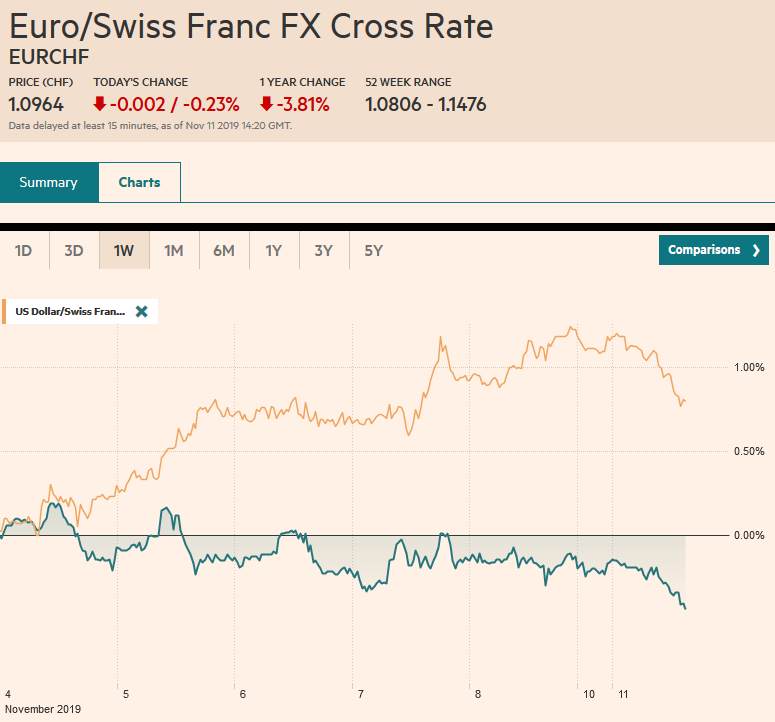

Swiss Franc The Euro has fallen by 0.23% to 1.0964 EUR/CHF and USD/CHF, November 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Escalating violence in Hong Kong and the continued fall in Chinese producer prices weighed on equities in Asia Pacific trading. The MSCI Asia Pacific Index has risen nearly 7% during the five-week rally and is off to a weak start this week. Hong Kong’s Hang Seng fell around 2.6%, its biggest loss in three months, and China’s CSI 300 was off 1.75%. Nearly all the local markets fell but Australia. European shares are also under pressure. The Dow Jones Stoxx 600 has also rallied for five consecutive weeks and is off about 0.25% through the morning. US equity markets will trade

Topics:

Marc Chandler considers the following as important: $CNY, 4.) Marc to Market, 4) FX Trends, brl, China, Currency Movement, EUR/CHF, Featured, FX Daily, Hong Kong, Japan Current Account, newsletter, U.K., U.K. Gross Domestic Product, U.K. Manufacturing Production, U.K. trade balance, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.23% to 1.0964 |

EUR/CHF and USD/CHF, November 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Escalating violence in Hong Kong and the continued fall in Chinese producer prices weighed on equities in Asia Pacific trading. The MSCI Asia Pacific Index has risen nearly 7% during the five-week rally and is off to a weak start this week. Hong Kong’s Hang Seng fell around 2.6%, its biggest loss in three months, and China’s CSI 300 was off 1.75%. Nearly all the local markets fell but Australia. European shares are also under pressure. The Dow Jones Stoxx 600 has also rallied for five consecutive weeks and is off about 0.25% through the morning. US equity markets will trade today, though the bond market is closed. In electronic trading, the S&P 500 is about 0.3% lower. Bond markets are narrowly mixed, though the risk-off mood has weighed on European peripheral bonds. We note that despite the inconclusive election, Spanish bonds are faring a little better than Italian bonds. The New Zealand dollar is the strongest of the major currencies, helped by some position adjusting ahead of the central bank meeting tomorrow after the shadow MPC recommended the RBNZ stand pat. Many had been looking for a 25 bp cut. However, the Australian dollar joins the Scandi currencies as the laggards today. The euro, yen, and sterling are posting modest gains. Most emerging market currencies are lower, and the dollar is popped back above CNY7.0. |

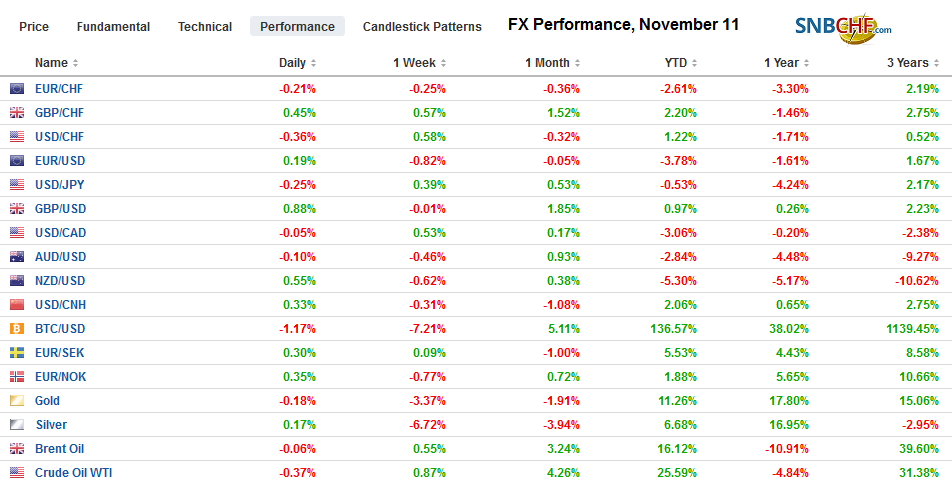

FX Performance, November 11 - Click to enlarge |

Asia PacificJapan reported a 2.9% slide in September core machinery orders (month-over-month) after a 2.4% decline in August. Most economists had been expecting an uptick. Core machinery orders, thought to be a lead indicator of capital spending, fell 3.5% in Q3 after a 7.5% gain in Q2. Businesses are optimistic about Q4 and project a 3.5% increase. Separately, the balance of payments data showed as the fiscal half-year ended, Japanese investors large sellers of Italian bonds and buyers of Spanish bonds. They also broadly preferred European bonds to the US. While nominal yields are lower, on a currency-hedged basis, they were higher. |

Japan Current Account n.s.a. September 2019(see more posts on Japan Current Account, ) Source: investing.com - Click to enlarge |

Following the death of a demonstrator in Hong Kong, violence escalated, and the police shot another protester. Some subways were shut, and most universities haled class. Chief Executive Lam is expected to make an announcement shortly. The tightening of the Emergency Powers is expected.

China reported falling producer prices and rising consumer prices. Consumer price rose 3.8% year-over-year in October. A Wall Street Journal poll found a median forecast of 3.5% after a 3% pace in September. However, this is largely a function of rising food prices (15.5% year-over-year, up from 11.12% in September), and this, in turn, is about pork prices, which rose over 100% year-over-year. It alone accounts for more than 2/3 of the headline inflation. Non-food prices rose 0.9% year-over-year after a 1.0% rise in September. Producer prices rose 0.1% in the month, but due to the base effect, the year-over-year decline accelerated to 1.6% from 1.2%. The takeaway is that the rise in pork prices because of the African Swine Flu is masking deflationary forces in China. Separately, China reported October lending figures well below expectations. Aggregate financing, which includes banking and shadow banking activity, rose by CNY619 bln after CNY2.272 trillion in September. A pullback had been widely anticipated, but it was roughly a third lower than expected. It was fully accounted for by the banking sector (new CNY loans rose CNY661 bln), suggesting that shadow banking activity actually contracted.

The dollar had been flirting with JPY109.50 in the last two sessions, but today is trading a little heavier. It has been unable to trade much above JPY109.20 but found bids in early European near JPY108.90. There is a roughly $350 mln option at JPY109 that expires today. Support is pegged in the JPY108.65-JPY108.75 area. The Australian dollar is trapped in narrow ranges in last week’s trough (~$0.6850). Initial resistance near $0.6870 has been tested and held. A move above $0.6900 is needed to improve the technical tone. The Chinese yuan took a five-week rally into this week and began off defensively. The US dollar has resurfaced above CNY7.0. The offshore yuan (CNH) retreated more than the onshore yuan.

EuropeMoody’s cut its outlook of UK’s creditworthiness to negative from stable. The rating itself was unchanged at Aa2, which is the equivalent of S&P and Fitch’s AA rating. They both also have negative outlooks. DBRS still has the UK at a AAA credit. Moody’s cited Brexit as a catalyst for the erosion of institutional strength. As the December election heats up, both of the leading parties are promising more public spending, jettisoning Osborne’s fiscal rule. At the same time, the BOE cut its growth and inflation forecasts and softened its neutral standing. The policy mix or easier fiscal and monetary policy is often associated with a weaker currency. |

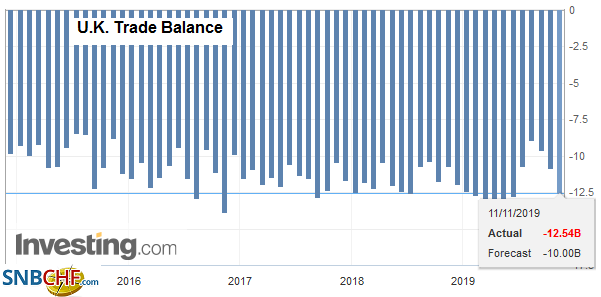

U.K. Trade Balance, September 2019(see more posts on U.K. Trade Balance, ) Source: investing.com - Click to enlarge |

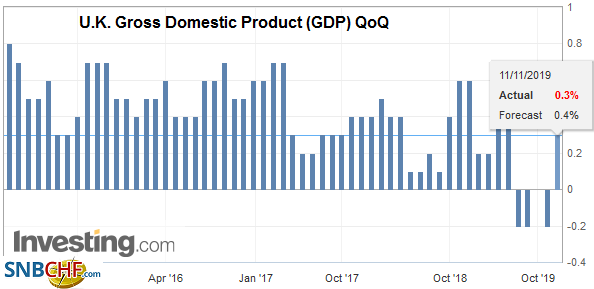

| The UK reported that a 0.1% decline in September GDP after a revised 0.2% contraction in August (from -0.1%). Nevertheless, in the quarterly calculations, the UK economy expanded by 0.3% in Q3 after a 0.2% decline in Q2. Yet no mistake can be made, the British economy finished the quarter with no momentum. Industrial output fell by 0.3% in September. The median forecast was for a 0.1% decline. Manufacturing output dropped by 0.4% after a 0.7% slide in August. Services were flat in September, and the trade balance deteriorated sharply. Construction also fell. |

U.K. Gross Domestic Product (GDP) QoQ, Q3 2019(see more posts on U.K. Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| The bookmakers in the UK and PredictIt show Johnson as around a 3-to-1 favorite to remain Prime Minister. However, the polling remains unclear whether the Tories can secure a majority. Spain’s fourth election in four years over the weekend does not look to have cleared up the logjam. The Socialists there remain the biggest party, even though it lost some seats. The surprise was the surge in the nationalist Vox party, which appears to have doubled its representation, while Podemos slipped. We are concerned that Spain shows that when the populous is divided, an election may not resolve the issue. The UK is clearly and closely divided on Brexit and what that really means. Ironically, in Northern Ireland, Johnson is campaigning on why it is a good thing that it remains part of the EU’s customs union. |

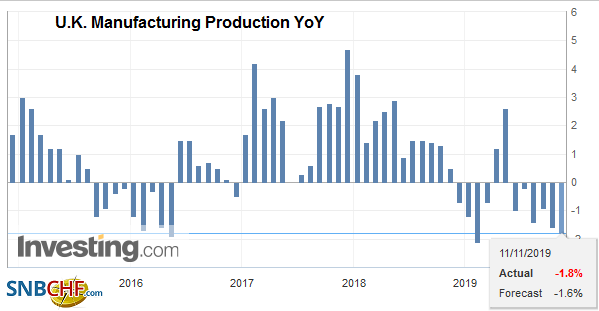

U.K. Manufacturing Production YoY, September 2019(see more posts on U.K. Manufacturing Production, ) Source: investing.com - Click to enlarge |

The euro fell every session last week and posting minor upticks today. A 625 mln euro option at $1.1050 that expires today may attract prices, though we suspect it might be too far as intraday technical readings are already getting stretched in the European morning with the euro a little above $1.1030. Sterling had traded down to around $1.2770 before the weekend and is consolidating its losses today by straddling the $1.28 area. The pre-weekend high was near $1.2825, which is where the five-day moving average is found.

America

The US made more forceful its pushback against ideas that a phase one agreement with China would result in a significant unwinding of existing tariffs. Word had already come out along these lines before the weekend, but investors took little notice. It looks like consummating the handshake agreement is proving more difficult than advertised. A deal this year is no longer a done deal.

Bolivia’s Morales resigned after the Organization of American States reported large irregularities in the October 20 election, and it became clear he lost the support of the army and police. Bolivia is one of several hot spots in the region.

With the partial holiday in the US today (stocks open, bonds closed), the busy week begins slowly. The economic data this week includes CPI, retail sales, and industrial production. Nearly all the regional Fed presidents and the Board of Governors speak this week, with the highlight being two-day of Powell speaking to Congress. Tomorrow President Trump speaks to the Economic Club of NY. Canada’s economic calendar is light this week. Mexico reports September’s industrial production figures today. It is expected to have edged higher, but not enough to offset the base effect, and year-over-year the contraction is expected to have deepened to -1.7% from -1.3% in August. It has averaged -3.0% in Q2. Mexico’s central bank is expected to cut its overnight target rate for the third time this year on November 14 to 7.5% from 7.75%.

Following the disappointing jobs report at the end of last week, which came after the central bank softened its neutral stance, the US dollar jumped from around CAD1.3175 to about CAD1.3235. The greenback is consolidating those gains in tight ranges so far today and has not been below CAD1.3215. Provided CAD1.3200 holds, the next target is near the 200-day moving average found a little above CAD1.3275. he US dollar remains rangebound against the Mexican peso. For nearly a month, it has traded between almost MXN19.00 and MXN19.25. It is around the middle of the range today. The dollar jumped 4.4% last week against the Brazilian real after the government’s plans to auction new oil fields found little foreign interest (outside of China). The release of former President Lula from prison, pending appeals of his conviction, also injected political uncertainty into the equation. The dollar is approaching the record high set four years ago near BRL4.2480. The more recent peaks are in the BRL4.19-BRL4.20 area.

Tags: #USD,$CNY,brl,China,Currency Movement,EUR/CHF,Featured,FX Daily,Hong Kong,Japan Current Account,newsletter,U.K.,U.K. Gross Domestic Product,U.K. Manufacturing Production,U.K. Trade Balance,USD/CHF