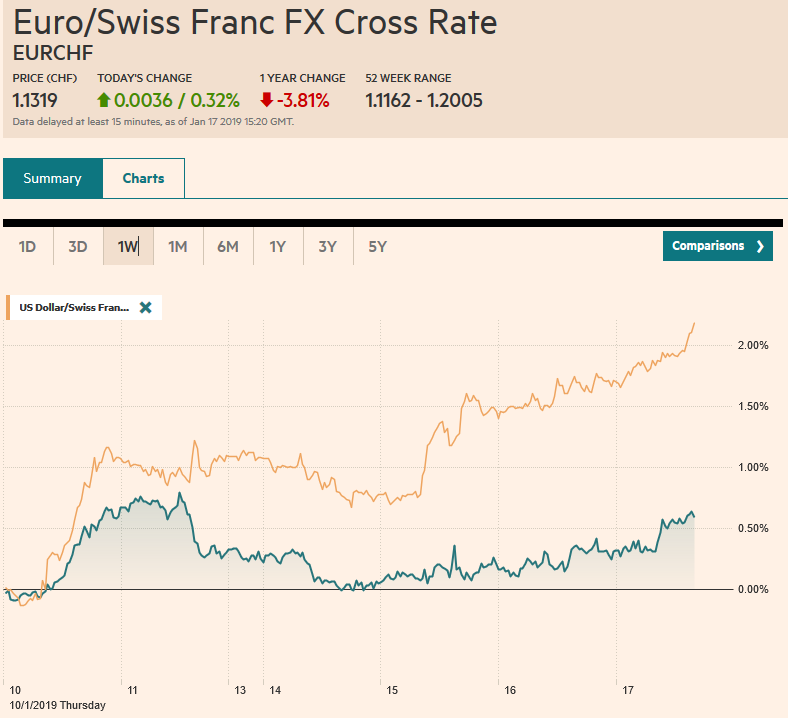

Swiss Franc The Euro has risen by 0.32% at 1.1319 EUR/CHF and USD/CHF, January 17(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The capital markets remain relatively subdued as fresh trading incentives are awaited, including US corporate earnings. Some of the enthusiasm for risk-assets has diminished. The MSCI Emerging Markets Index has stalled after trading at six-week highs yesterday, though most bourses in Asia were higher, but the Nikkei (Topix gained), China, and Singapore. The Dow Jones Stoxx 600 is a bit heavier but continued to bump against 350, the best since mid-December. US shares are trading lower, and the S&P 500 is poised to test previous

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, AUD, CAD, EUR, EUR/CHF and USD/CHF, Featured, GBP, JPY, MXN, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.32% at 1.1319 |

EUR/CHF and USD/CHF, January 17(see more posts on EUR/CHF and USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The capital markets remain relatively subdued as fresh trading incentives are awaited, including US corporate earnings. Some of the enthusiasm for risk-assets has diminished. The MSCI Emerging Markets Index has stalled after trading at six-week highs yesterday, though most bourses in Asia were higher, but the Nikkei (Topix gained), China, and Singapore. The Dow Jones Stoxx 600 is a bit heavier but continued to bump against 350, the best since mid-December. US shares are trading lower, and the S&P 500 is poised to test previous resistance now support near 2600. Benchmark bond yields are little changed. The dollar is mostly firmer, though it has been unable to sustain yesterday’s gains that carried it to JPY109.20, the highest since January 2. |

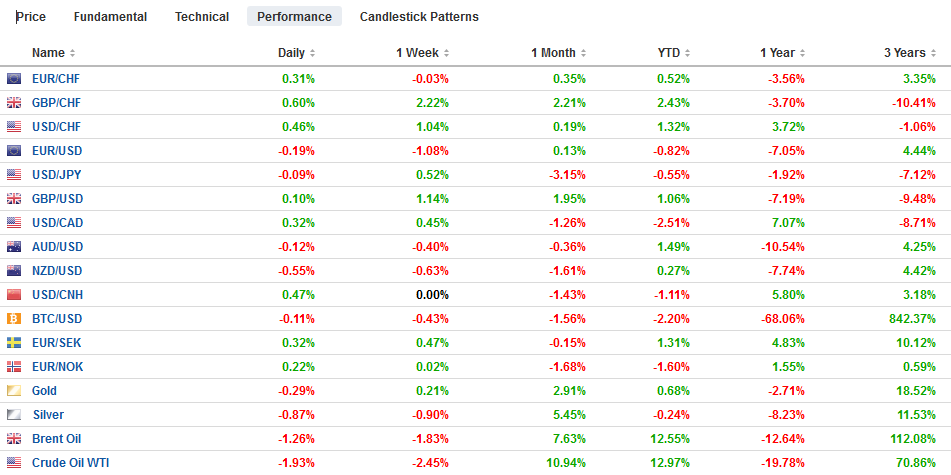

FX Performance, January 17 - Click to enlarge |

Asia Pacific

The limited news from the region was generally disappointing. Australia reported slower lending for both homes and investment and softer consumer inflation expectations. New Zealand reported a 12.9% year-over-year drop in house sales. National sales were the lowest for December in seven years. Weakness is concentrated but especially pronounced in Auckland. The takeaway here is that both countries are wrestling with the end of a housing boom and the economic consequences. Both central banks are on hold, but rate cuts later in the year cannot be ruled out.

Given Singapore’s role in the global division of labor as an entrepot, its December trade figures are jarring. Non-oil domestic exports were off 5.7% in December. The median forecast by economists in the Bloomberg survey looked for a 3% gain. On a year-over-year basis, they fell by 8.5%, the most in two years. Electronics exports, a reflection of world demand, slumped 11.2% year-over-year in December. Non-oil exports to China rose 15.4% and 31% to the US. Exports to the EU fell by 28.7%.

The dollar is trading inside yesterday’s range against the Japanese yen. It had risen to JPY109.20 yesterday, taking out last week’s high by around ten pips. Look for support in the JPY108.40-60 area to temper deeper declines, barring new volatility in equities. The Australian dollar recorded new lows for the week a little below $0.7150. It bounced in late-Asia/early Europe to $0.7170 but met a wall of offers. Last week’s low was near $0.7110. A break of $0.7100 is needed to lend credibility to ideas that a top is in place. The New Zealand dollar is off for the fourth consecutive session and is also holding above last week’s low a little above $0.6700. The Kiwi stalled today just ahead of $0.6780 and $0.6795 expiring options for almost NZD900 mln. The dollar rose by nearly 0.2% against the Chinese yuan, its biggest gain of the year. There is some concern that the US likely escalation of efforts against Huawei may hamper trade talks. China’s death sentence for a Canadian, allegedly for drug smuggling is seen by many as chiefly political and retaliatory.

Europe

Prime Minister May survived the vote of confidence after the historic defeat of the Withdrawal Bill by 19 votes. She made an impromptu statement late yesterday after meeting with a several opposition party leaders and expressed disappointment at Corbyn’s failure to participate (dis-May). The Labour leader demanded that May rule out a Brexit with no-agreement. She cannot do that formally without undermining what is left of the UK’s negotiating position with the EC. However, while preparations must continue, it does not appear to be the most likely scenario. It is in no one’s interest, despite what some MPs may say. Instead, we continue to believe a delay is the most likely scenario as the UK decides what to do next. Reports suggest the EC is willing to consider a delay into the second half. There does appear to be some momentum for a second referendum. Failing to defeat May in the vote of confidence yesterday means that Labour shifts to its fallback position–a second referendum. May will submit an amendable bill on Monday, which will lay out her new approach.

Greece’s Prime Minister Tsipras also survived a vote of confidence yesterday by a narrower margin than May (151-148). It is the fourth vote of confidence he has survived and could be his last ahead of national elections in September, which the polls show he will likely lose to the center-right New Democracy. However, like May, how he can proceed is not clear. There does not appear to be a majority that will ratify the accord with the Republic of Macedonia. The problem is that many Greeks disapprove of the name which is a state in Greece.

The euro slipped to a two-week low earlier today near $1.1370, and for the third consecutive session has straddled the $1.14 level. There is an almost 680 mln euro option struck there that expires today and 1.5 bln euro option that rolls off tomorrow. It is also the third session of lower highs and lower lows. The five-day moving average is falling below the 20-day moving average for the first time in a month. Sterling continues to consolidate. Ahead of May’s bill on Monday, look for the consolidation to continue, mostly with a $1.28 handle.

North America

The US reports the Philly Fed manufacturing survey and weekly initial jobless claims. Other data has been delayed by the government’s partial shutdown. The economic impact is growing. Many investors forget or are not aware of the extent that the government facilitates activity. Initial public offerings are being held back, various registrations cannot be done, and even approval for FHLC loans cannot be given. With the ITC closed, there is some risk to the start of trade negotiations with Japan and Europe that were supposed to start later this month. The Beige Book, prepared for the upcoming FOMC meeting, reflected concerns about trade and market volatility, while the government shutdown was too new to impact sentiment much. Most regions reported a modest pace of growth, while a few saw slower activity. Still, it did not read like a recessionary warning in any way. After a growth surge (peak) in Q2-Q3 18, the economy was expected to slow in Q4 but remain above trend. US corporate earnings reports today include more banks, and non-bank financial institutions, as well as Netflix and PPG.

The sharp downside pressure on the US dollar against the Canadian dollar, which took it from around CAD1.3660 on January 3 to CAD1.3130 in five sessions has eased. The greenback has remained above CAD1.3225 this week. It briefly traded above CAD1.33 earlier today for the first time since January 8. Initial support is seen near CAD1.3260 today. The dollar fell to fresh three-month lows against the Mexican peso today just below MXN18.88. A move above MXN19.05-MXN19.10 would be an early sign of that the downside momentum is easing. The technical indicators are extended, and a recovery in the dollar could leave bullish divergence (where technical indicators do not confirm the latest dollar lows).

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$CNY,$EUR,$JPY,EUR/CHF and USD/CHF,Featured,MXN,newsletter