Perspectives Pictet

Perspectives Pictet

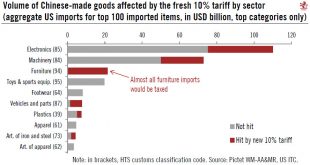

Latest Trump tariffs move beyond Chinese tech imports.This week, the Trump administration announced it would slap a 10% tariff on USD200 billion of imports from China, on top of the USD50 billion already announced. After a consultation period, the tariffs could come into force as soon as September (see our Flash Note ‘US-China trade update’, 11 July 2018). The US imported USD506 billion of merchandise from China in 2017.Officially, the new set of tariffs are a response to China’s...

Read More »Fresh tariffs on Chinese imports would fall disproportionately on furniture