Perspectives Pictet

Perspectives Pictet

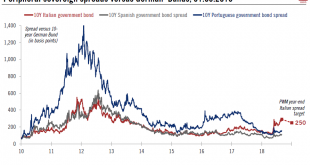

Pictet Wealth Management's latest positioning across asset classes and investment themes.Asset AllocationWe maintain our neutral stance on equities overall on a rolling three-to-six month basis. We do have a more upbeat assessment further out, but the autumn is shaping up to be a sensitive time for risk assets overall.Recent sell-offs validate our cautiousness regarding emerging-market (EM) assets in general. But valuations are becoming more interesting and we do have a bullish short-term...

Read More »House View, September 2018