Thomas Costerg

September 26, 2018

Perspectives Pictet

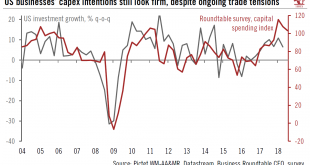

The upswing in US capex defies negative trade headlines.The torrent of coverage about trade tensions hides an important positive development: US corporate investment is flourishing, and there are increasing signs this upswing in capital expenditure (capex) could persist. This could in turn mean that the US business cycle has further room to run, despite its advanced age, and that recession is still some way off.A survey we like to watch, particularly to gauge capex trends, is the quarterly...

Read More »

Perspectives Pictet

September 26, 2018

Perspectives Pictet

Download issue:English /Français /Deutsch /Español /ItalianoFresh US tariffs against Chinese imports, followed swiftly by Chinese retaliation, are casting a shadow over prospects for the global economy. But just how much could they hurt growth? And what are the implications for various asset classes and for investors?In this special edition of Perspectives, experts at Pictet Wealth Management (PWM) set out to answer these questions.Christophe Donay, PWM’s Chief Strategist and Head of Asset...

Read More »

Cesar Perez Ruiz

September 24, 2018

Perspectives Pictet

The CIO office’s view of the week ahead.Today’s kicking in of US tariffs on an extra USD200bn of Chinese imports, and China’s retaliation, marks a notable escalation in the trade war between the two countries. But markets prefer to look at the robust US economy, with strong M&A activity also helping (of which Comcast’s winning bid for Sky is just the latest manifestation). Markets seem to be betting that trade tensions will eventually cool. There is indeed a possibility that trade...

Read More »

Thomas Costerg

September 21, 2018

Perspectives Pictet

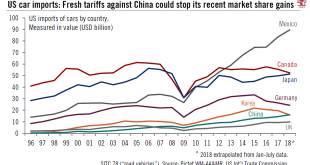

China’s ascent in the US car market could be stopped short by new tariffsUS President Donald Trump has shown a particularly strong interest in the US car industry – which carries both significant symbolic and political weight – and therefore in trade flows of foreign cars into the US. The recently negotiated trade agreement with Mexico is mostly about car manufacturing, particularly aimed at halting the ongoing displacement of US car production to Mexico. And Trump’s grievances against...

Read More »

Nadia Gharbi

September 21, 2018

Perspectives Pictet

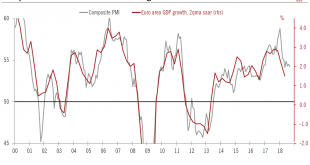

The services sector is proving resilient, but manufacturing disappoints.Euro area flash composite PMI dipped slightly in September, coming in slightly below consensus expectations. Activity in services picked up and weakened further in manufacturing, which continued its decline since the start of the year, falling to 53.3 in September from 54.6 in August. New export orders failed to grow for the first time since June 2013.Overall, euro area composite PMI remains consistent with our forecast...

Read More »

Nadia Gharbi

September 21, 2018

Perspectives Pictet

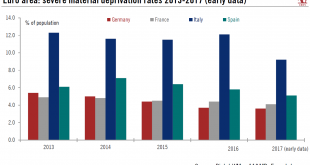

Latest poverty figures provide government with an argument for fiscal stumulus.Severe material deprivation rates gauge the proportion of people whose living conditions are severely affected by a lack of resources. According to Eurostat, “it represents the proportion of people living in households that cannot afford at least four of the following nine items: mortgage or rent payments, utility bills, hire purchase instalments or other loan payments; one week’s holiday away from home; a meal...

Read More »

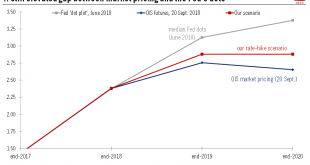

Thomas Costerg

September 21, 2018

Perspectives Pictet

Next week’s Fed policy meeting is likely to confirm that the central bank is still on the path of gradual rate hikes, but could also see some hawkish signals on future policy.The Fed is very likely to raise rates by 25bps on 26 September, dismissing the trade war risk and emphasising the strong domestic economy and healthy job market instead.With a rate widely anticipated, the focus will be on any signals about future rates. We expect Chairman Jerome Powell’s press conference and the update...

Read More »

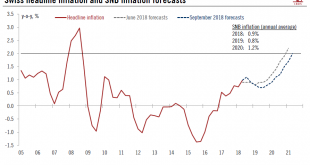

Nadia Gharbi

September 20, 2018

Perspectives Pictet

The Swiss National Bank has revised down its medium-term forecast for consumer inflation. We still expect a first SNB rate hike in September 2019.At the end of its quarterly monetary assessment meeting, the Swiss National Bank (SNB) left its main policy rates unchanged. Also unchanged from the last quarterly meeting in June was the central bank’s assessment of the Swiss franc as “high valued” and its characterisation of the situation on foreign exchange as “fragile”. The SNB emphasized that...

Read More »

Team Asset Allocation and Macro Research

September 19, 2018

Perspectives Pictet

While the recent economic ‘soft patch’ has hurt all the main euro area economies, some have been more affected more than others. A divergence in fortunes can be seen across asset classes.The four biggest euro area economies slowed in H1 2018 due to a number of factors, including weak exports. We expect a rebound in H2—except in Italy, where political uncertainty has been denting business confidence. Forward indicators show that Italy is the only of the four major euro area economies to face...

Read More »

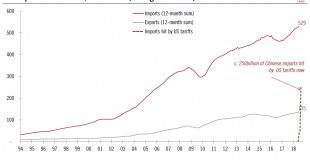

Thomas Costerg and Dong Chen

September 18, 2018

Perspectives Pictet

The latest US levies on USD200bn of Chinese imports could leave some room for negotiation before the tariff rate is increased.The Trump administration has announced new tariffs on USD200 billion of Chinese imports, initially at a rate of 10%, rising to 25% in January. This new wave of tariffs comes on top of the USD50 billion taxed over the summer at a rate of 25%. Trump has also threatened to impose levies on all remaining imports from China (worth an additional USD276 billion) if China...

Read More »

Perspectives Pictet

Perspectives Pictet