Senate Democrats are setting the table for passage of President Biden’s proposed $1.9 trln relief bill; there were glimmers of possible bipartisanship in some of the votes; US January jobs data is the highlight; Canada also reports January jobs data; Colombia reports January CPI

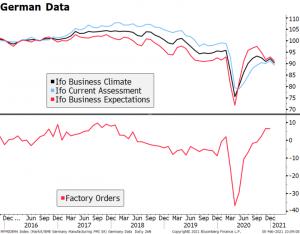

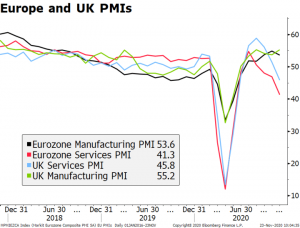

German data is showing further signs of weakness; BOE delivered a less dovish than expected hold; Deputy Governor Ramsden said he envisions slowing the pace of QE later this year

Japan reported December household spending; RBA released its quarterly Statement on Monetary Policy; Indonesia Q4 GDP data came in around expectations; India kept rates on hold at 4.00% as mostly expected; Chinese tech giant Alibaba placed $5 bln in international bonds in maturities of up to 40 years

The dollar is

Dollar Consolidates Its Gains Ahead of Jobs Report

February 5, 2021