Most EM currencies were up last week, once again taking advantage of broad dollar weakness. In addition, EM equities also performed well, with MSCI EM up for the third week in a row and for seven of the past eight. We expect EM assets to continue benefiting from the global liquidity story as well as the weak dollar trend. AMERICAS Brazil reports mid-November IPCA inflation Tuesday. Inflation is expected at 4.15% y/y vs. 3.52% in mid-October. If so, this would be the highest since mid-February and would move back into the top half of the 2.5-5.5% target range for the first time since that month. Next COPOM meeting is December 9 and rates are expected to remain steady at 2.0%. However, the CDI market is pricing in the first hike of the tightening cycle at the

Topics:

Win Thin considers the following as important: 5.) Brown Brothers Harriman, 5) Global Macro, Articles, emerging markets, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

![]() Most EM currencies were up last week, once again taking advantage of broad dollar weakness. In addition, EM equities also performed well, with MSCI EM up for the third week in a row and for seven of the past eight. We expect EM assets to continue benefiting from the global liquidity story as well as the weak dollar trend.

Most EM currencies were up last week, once again taking advantage of broad dollar weakness. In addition, EM equities also performed well, with MSCI EM up for the third week in a row and for seven of the past eight. We expect EM assets to continue benefiting from the global liquidity story as well as the weak dollar trend.

AMERICAS

Brazil reports mid-November IPCA inflation Tuesday. Inflation is expected at 4.15% y/y vs. 3.52% in mid-October. If so, this would be the highest since mid-February and would move back into the top half of the 2.5-5.5% target range for the first time since that month. Next COPOM meeting is December 9 and rates are expected to remain steady at 2.0%. However, the CDI market is pricing in the first hike of the tightening cycle at the January meeting. October current account and FDI data will be reported Wednesday. Central government budget data will be reported Friday, where a primary deficit of -BRL26.0 bln is expected.

Mexico reports mid-November CPI Tuesday. Inflation is expected at 3.63% y/y vs. 4.09% in mid-October. If so, this would be the lowest since June and would move back within the 2-4% target range for the first time since July. Banco de Mexico releases its quarterly inflation report Wednesday. Minutes from the November 12 meeting will be released Thursday. At that meeting, the bank surprised markets by keeping rates on hold at 4.0%, noting that the “pause provides necessary space” for inflation to converge back to the bank’s goal. Next policy meeting is December 17. October trade will be reported Friday.

Colombia central bank meets Friday and is expected to keep rates steady at 1.75%. The bank left rates steady at its last meeting October 30, ending a streak of cuts dating back to March that took the policy rate from 4.25% to the current 1.75%. Governor Echavarria implied that another cut was unlikely before his term ends in January. He is not seeking another term and so it will be up to his successor to restart the easing cycle if it’s warranted. Inflation was only 1.75% y/y in October, the lowest on record and below the 2-4% target range.

EUROPE/MIDDLE EAST/AFRICA

Poland reports October construction output and real retail sales Monday. The former is expected to fall -7.6% y/y vs. -9.8% in September, while the latter is expected to fall -0.8% y/y vs. +2.5% in September. Activity will likely be impacted by high virus numbers and the resulting lockdowns, though some measures have been eased. Shopping malls will reopen next weekend, but restaurants and bars will remain closed. Given downside risks, low inflation should allow the central bank to maintain loose policy for the foreseeable future. Next policy meeting is December 2 and no change is expected then.

South Africa reports October CPI Wednesday. Headline inflation is expected to remain steady at 3.0% y/y. If so, it would remain at the bottom of the 3-6% target range. SARB just left rates steady at 3.5% last week but it was a close call as the vote went 3-2. Even more surprising is that the SARB’s model suggests 50 bp of tightening in 2021 and another 75-100 bp in 2022. This seems highly unlikely. Next policy meeting is January 21. A lot can happen between now and then but if the recovery remains sluggish, the MPC could pivot to a rate cut then.

ASIA

Korea reports trade data for the first 20 days of November Monday. Of note, total exports rose 20.1% y/y for the first 10 days of the month while average daily exports rose 12.1% y/y. The strong won does not seem to be having a negative impact on exports and growth, at least for now. Bank of Korea meets Thursday and is expected to keep rates steady at 0.50%. However, we would expect some potential jawboning against the strong won. Last week, Finance Minister Hong said FX moves were one-sided and that policymakers may take active measures to stabilize the markets.

Singapore reports October CPI Monday. Headline inflation is expected to remain flat y/y. The MAS does not have an explicit inflation target but low price pressures will allow it to keep policy loose for the foreseeable future. Next scheduled policy meeting is not until April but he MAS can and will move intra-meeting if circumstances warrant. October IP will be reported Thursday and is expected to rise 7.5% y/y vs. 24.2% in September.

India reports Q3 GDP data Friday. The economy is expected to contract -8.7% y/y vs. -23.9% in Q2. Despite the weak economy, high inflation has kept the RBI on hold since the last 40 bp cut in May. Next policy meeting is December 4 and no change is expected. CPI rose 7.61% y/y in October, the highest since May 2014 and well above the 2-6% target range. the new members of the MPC are likely to tilt dovish but will likely wait for price pressures to ease before cutting rates.

You Might Also Like

Risk assets remain hostage to swings in market sentiment. Stronger than expected US jobs data last week was welcome news. However, the tug of war between improving economic data and worsening viral numbers is likely to continue this week, with many US states reporting record high infection rates.

This is likely to be one of the most eventful weeks we’ve had in a while. Not only do three major central banks meet, but four EM central banks also meet, and we get important June and July data from the US, the first Q2 GDP reading from China, an OPEC+ meeting, and an EU summit.

EM currencies took advantage of broad dollar weakness against the majors last week, with most gaining against the greenback. Yet the week ended on a bit of a risk-off note as concerns intensified about the resurgent virus and the impact on the still-weak global economy.

The dollar got some traction against the majors towards the end of last week. This weighed on EM FX, with the high best currencies TRY, BRL, CLP, and ZAR leading the losers. We downplay risk of contagion from Turkey, but we acknowledge it will keep investors wary of the countries with poor fundamentals.

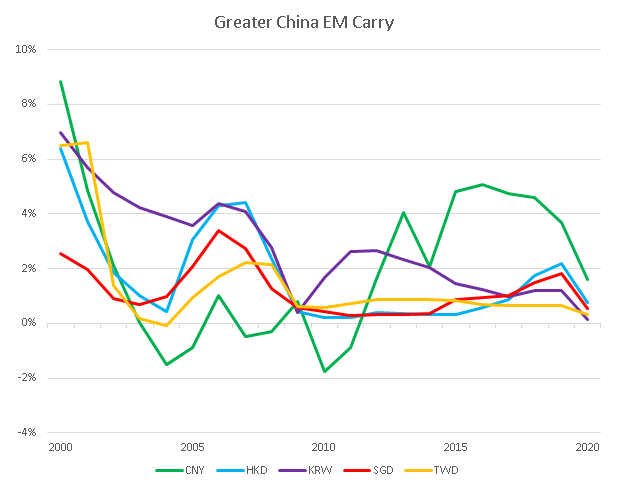

Where Has All the Carry Gone?

Where Has All the Carry Gone?

Despite broad-based dollar weakness, EM currencies have not fully participated in the risk on environment that’s now in place. The good news is that fundamentals matter again. The bad news is that there are a lot of EM countries with bad fundamentals, and the secular decline in carry no longer gives these weaklings any cover.

Persistent risk-off impulses weighed on EM last week and that may continue this week. The Asian currencies outperformed last week while MXN, ZAR, and COP underperformed, and we expect these divergences to continue. Despite optimism about a stimulus package in the US, we think it remains a long shot. Meanwhile, virus numbers are rising in Europe and the US, with data from both regions likely to continue weakening.

Risk assets are coming off a tough week. The dollar was bid across the board except for the yen, which outperformed slightly. The only EM currencies to gain against the dollar were KRW and CLP. The major US equity indices somehow managed to eke out very modest gains but stock markets across Europe sank as the viral spread threatens to slam economic activity again.

EM FX took advantage once again of broad dollar weakness. Most EM currencies were up last week against the dollar, with the only exceptions being ARS, TRY, INR, THB, PEN, and MYR. We expect the dollar to remain under pressure this week and so EM should remain bid.

Tags: Articles,Emerging Markets,Featured,newsletter