Swiss Franc The Euro has risen by 0.11% to 1.0837 EUR/CHF and USD/CHF, January 7(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: After the National Guard were called to put down an insurrection in Washington, DC, the dollar is having its best day in around a week. The euro’s three-day rally has been halted even though German factory orders surprised on the upside. The greenback is firmer against all the major and most of the emerging market currencies today. Equities are moving higher. All the markets in the Asia Pacific but Hong Kong rallied today after the 8-day advance stalled yesterday. Hong Kong appeared to have been dragged lower by concern that the US would delist Alibaba and Tencent. Europe’s Dow

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, Australia, China, Currency Movement, Featured, Germany, newsletter, USD

This could be interesting, too:

Eamonn Sheridan writes CHF traders note – Two Swiss National Bank speakers due Thursday, November 21

Charles Hugh Smith writes How Do We Fix the Collapse of Quality?

Marc Chandler writes Sterling and Gilts Pressed Lower by Firmer CPI

Michael Lebowitz writes Trump Tariffs Are Inflationary Claim The Experts

Swiss FrancThe Euro has risen by 0.11% to 1.0837 |

EUR/CHF and USD/CHF, January 7(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: After the National Guard were called to put down an insurrection in Washington, DC, the dollar is having its best day in around a week. The euro’s three-day rally has been halted even though German factory orders surprised on the upside. The greenback is firmer against all the major and most of the emerging market currencies today. Equities are moving higher. All the markets in the Asia Pacific but Hong Kong rallied today after the 8-day advance stalled yesterday. Hong Kong appeared to have been dragged lower by concern that the US would delist Alibaba and Tencent. Europe’s Dow Jones Stoxx 600 gapped up to new highs but has moved to close the gap. US shares are trading around 0.5% higher. Pressure remains in the debt markets. The MSCI Emerging Market equity index is at its best level since 2007. The US 10-year benchmark is firm near 1.05%, while most sovereign 10-year bonds are up to 3-4 bp higher today. Gold held $1900 in yesterday’s slump. It now meets resistance near previous support around $1930. Oil prices are firm, and the February WTI contract has pushed above $51. In early November, it was below $40. |

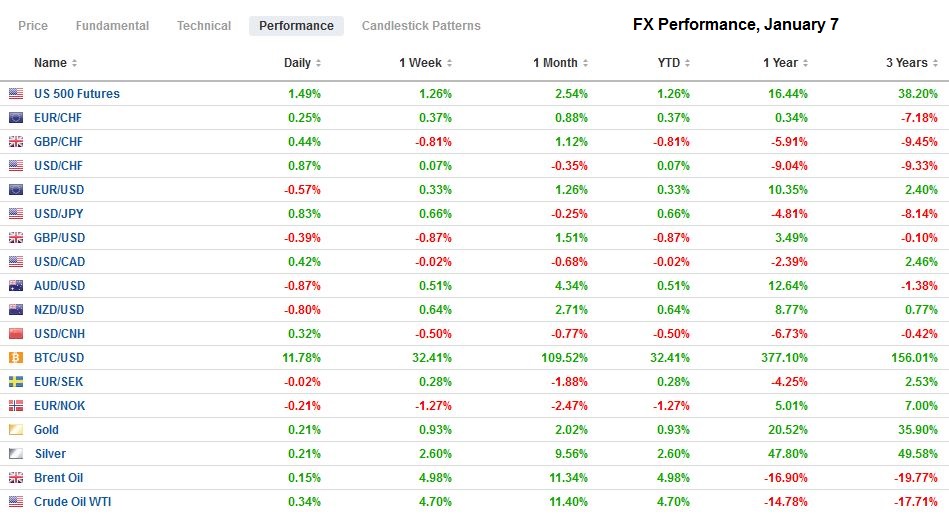

FX Performance, January 7 - Click to enlarge |

Asia Pacific

Japan’s Prime Minister Suga has declared Tokyo and the three surrounding prefectures to be in a state of emergency that will last at least until February 7. The emergency does not mean a stringent lockdown. The restrictions appear less than what was imposed last year. Still, Suga’s public support has waned. His personal conduct has been criticized. Hopes for an early election to secure his own mandate after Abe’s resignation looks to be pushed back, though an election must be held by late October. Meanwhile, the high-frequency data showed labor cash earnings dropped 2.2% in the year through November. This was considerably worse than the 0.9% median forecast in the Bloomberg survey and the fastest drop since last May. It is the eighth consecutive year-over-year drop and casts a pall over the consumption outlook. Household spending will be reported tomorrow. It rose in October (year-over-year) for the first time since September 2019 but likely fell in November.

China reported a slightly larger than expected rise in December reserves. Its reserves rose by $38 bln in December, following a $50.5 bln increase in November, to stand at $3.22 trillion. Bloomberg’s survey median forecast was for $3.20 trillion. The other major reserve currencies appreciated so valuation may have helped lift the reserve holdings. The challenge is that between the trade surplus and capital inflows, many economists would expect greater yuan appreciation (less than 1% in December) or stronger growth in reserves. The PBOC appears to have various levers that can be used, including policy banks and sovereign wealth fund. The US Treasury’s recent report was mostly critical of China for the lack of transparency in currency matters.

Objecting to Australia’s alliance with the US, Beijing has blocked a wide variety of its imports. However, Australia’s trade figures have been fairly resilient. Earlier today, it reported that November exports rose 3%. Economists surveyed by Bloomberg expected a 2% decline. Exports to China fell by about A$300 mln in November, but this was more than offset by the nearly A$1.3 bln increase in exports to the US and A$150 bln increase of shipments to Japan. Exports to Singapore also rose by around A$1 bln. Iron ore exports fell 7.9% from a record-high in October. Coal exports were off by nearly as much. Gold exports surged by almost 40% in the month (to A$2.6 bln). Australia’s imports jumped 10% in November, more than three times greater than expected. The trade balance was a A$5.02 bln surplus down from a revised A$6.58 bln in October.

The dollar bounced sharply yesterday after reaching a new 10-month low yesterday near JPY102.60. It managed to settle just above JPY103.00, and today reached almost JPY103.60 in the European morning. The jump in Treasury yields and the yen’s relative strength may be encouraging insurance companies and investors to step up their foreign bond buys. The dollar has not traded above JPY104 since mid-December. The Australian dollar poked above $0.7800 yesterday and tried again today, but the market looks a bit stretched after rallying by about two cents in a little more than a week. Initial support is seen near $0.7730, and a break could signal a leg lower toward $0.7640. The PBOC set the dollar’s reference rate at CNY6.4608. It is a little weaker than the models, but closer than it was yesterday. The dollar reached a low near CNY6.643 on Tuesday and has been consolidating in a narrow range since (~CNY6.4515-CNY6.4665) as officials are believed to have signaled a desire to temper or slow the yuan’s gains.

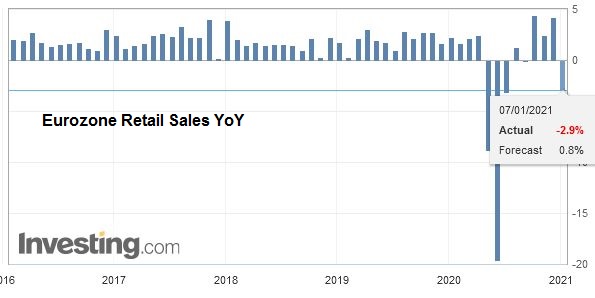

EuropeAlthough German retail sales had surprised on the upside (1.9% instead of a 2% decline as the median forecast in the Bloomberg survey implied), the aggregate figures for the region were depressing. Specifically, retail sales in November crashed by 6.1%. Here the median forecast was for a 3.4% decline. October’s 1.5% gain was shaved to 1.4%. |

Eurozone Retail Sales YoY, November 2020(see more posts on Eurozone Retail Sales, ) Source: investing.com - Click to enlarge |

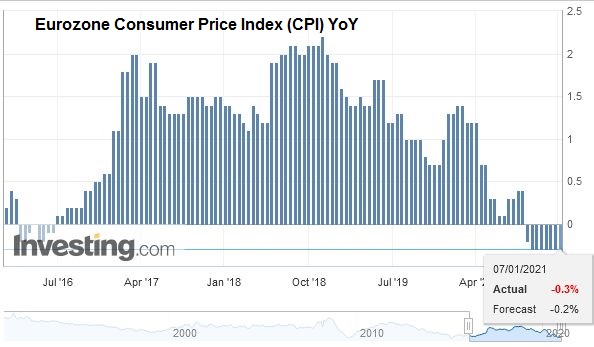

| Separately, the eurozone’s December CPI was in line with expectations. Headline prices are 0.3% below year-ago levels, where it has been stuck since September. |

Eurozone Consumer Price Index (CPI) YoY, December 2020(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

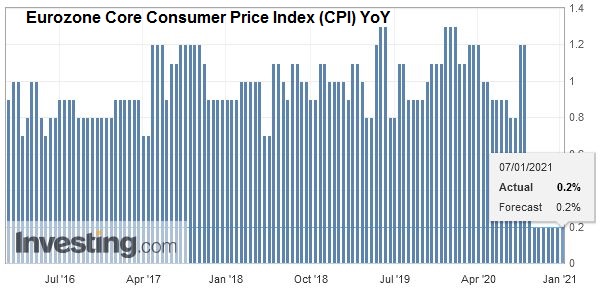

| Year-over-year inflation has not been positive since last July. The core rate has similarly been stuck at 0.2% for the fourth month in December. |

Eurozone Core Consumer Price Index (CPI) YoY, December 2020(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

Germany surprised again on the upside. Factory orders in November rose by 2.3%. Economists had been expected a modest decline. Adding to the upbeat message was the upward revision to the October series to 3.3% from 2.9%. Notable strength (6.1%) was seen in orders from within the eurozone, while domestic orders rose by a more modest but solid 1.6%. This comes not only on the heels of stronger retail sales but also an employment report that showed a decline in the unemployed queues. Some economists are beginning to talk about Germany possibly escaping a contraction in Q4. Tomorrow it reports industrial output figures. There is not always a tight fit, but rising orders are often associated with increased output.

The euro reached almost $1.2350 yesterday before stalling, and today it is nearly a cent lower in Europe. Support is seen in the $1.2200-$1.2220 area. The fact that it stalled after the wide miss of the ADP jobs estimate fits into the scenario we had suggested that the greenback was stretched by the recent sell-off, and much bad news was discounted. We had anticipated that resilience to a poor national jobs figure on Friday would signal the onset of the correction. Still, the intraday technicals suggest limited additional euro losses today. It closed last year near $1.2215. Sterling is quieter and within yesterday’s range (~$1.3540-$1.3670) and remains within the range set Monday (~$1.3540-$1.3705). It finished 2020 near $1.3670.

America

President Trump appears to have signaled a “peaceful transition” after yesterday’s chaos in the capital that shocked and dismayed (if not scared) the nation and world. Nevertheless, order has been restored, and there are reports of numerous staff resignations. Although there is talk of impeachment or invoking the 25th amendment to replace Trump with Pence, don’t expect much to come from it. At most, Congress may censure the President for seemingly encouraging yesterday’s actions and continues to press with the “election was stolen” rhetoric. Net-net, the economic consequences of the political theater are likely very limited.

The US reports weekly jobless claims. A small rise is expected, but the holiday-period may have distort, and the national employment report tomorrow trumps today’s report. The US also reports November trade figures. The average monthly shortfall through October was $53.67 bln in 2020. This is roughly 10% larger than the average in the first 10-months of 2020 (~-$49 bln). Lastly, the US also sees the December ISM services index. A decline from November’s 55.9 reading is expected.

Canada reports its November trade figures today too. Through October, its monthly trade deficit has averaged C$2.96 bln in 2020. It is almost double what it had averaged in the first ten months of 2019 (~-C$1.49 bln). Unlike its southern neighbor, it does not blame current account surplus countries for its deficit. Canada’s IVEY survey is also on tap, but it tends not to be a market-mover. Tomorrow, it reports December jobs, which are expected to have fallen by around 30k after rising 62k in November. Mexico reports December CPI figures, and the year-over-year pace is expected to have slipped for the second month after peaking near 4.10% in October.

The US dollar is recovering from a new low since April 2018, recorded yesterday near CAD1.2630. In Europe, it is trading above yesterday’s high (~CAD1.2725). A move above CAD1.2800 would suggest the anticipated greenback correction may be at hand. Similarly, the US dollar is recovering against the Mexican peso after falling to its lowest level since last March (~MXN19.60). The week’s high is around MXN20.10. Consolidation may be on tap, and the intraday technicals suggest the MXN19.90 area maybe a sufficient cap today.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

FX Daily, July 16: Equities Slide and the Greenback Bounces After China’s GDP and Before the ECB

2020-07-16

Overview: Profit-taking, perhaps spurred by disappointing retail sales figures, sent Chinese equity markets down by 4.5%-5.2% today, the most since early February. It appears to be triggering a broader setback in equities today. The Hang Seng fell 2%, and most other markets in the region were off less than 1%.

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

FX Daily, August 18: Canada Shrugs Off Loss of Morneau and Gold Reclaims $2000 Threshold

2020-08-18

The NASDAQ rallied 1% yesterday to record highs as the Dow Industrials struggled, and the S&P 500 was able to eke out a small gain. The coattails were short, and the strength of the yen may have contributed to a 0.2% loss of the Nikkei. Still, its 6.2% advance this month is the best among the G10.

FX Daily, August 27: After much Build-Up, Could Powell be Anti-Climactic?

FX Daily, August 27: After much Build-Up, Could Powell be Anti-Climactic?

2020-08-27

The strong rally in US equities yesterday, with the fifth consecutive gain in the S&P 500 and a big outside up day in gold, failed to spur follow-through buying today. Asia Pacific equities were mixed. China, Australia, and India rose while most of the rest of the regional markets fell.

FX Daily, October 15: Markets Shake and Dollar Goes Bid

FX Daily, October 15: Markets Shake and Dollar Goes Bid

2020-10-15

A combination of the surging virus, threatening the slow recovery that was already losing momentum, the lack of new stimulus in the US, and market positioning is seeing risk unwind in a big way today. Equities are selling off.

FX Daily, November 27: Dollar Offered Ahead of the Weekend

FX Daily, November 27: Dollar Offered Ahead of the Weekend

2020-11-27

Equities are finishing the week on a firm tone, while the US dollar remains heavy. In the Asia Pacific, only Australia and India did not end the week on a firm note. The MSCI Asia Pacific completed its fourth consecutive weekly gain, for around a 13% gain.

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

FX Daily, December 2: Euro Rally Stalls while Brexit Concerns Trip Sterling

2020-12-02

The selling pressure that drove the dollar lower yesterday has abated, and the greenback is paring yesterday’s loss, though the dollar-bloc currencies are showing some resilience. EC negotiator Barnier briefed ministers that the same three issues that have bedeviled the trade talks with the UK remain unresolved (fisheries, level playing field, and a conflict resolution mechanism).

FX Daily, December 15: The Bulls are Emboldened

FX Daily, December 15: The Bulls are Emboldened

2020-12-15

The S&P fell for the fourth consecutive session yesterday, the longest losing streak of the quarter, and this seemed to encourage profit-taking in the Asia Pacific region today. The MSCI Asia Pacific Index slipped for the second consecutive session, and even confirmation of the Chinese recovery failed to lift the Shanghai Composite.

FX Daily, December 17: Dollar Thumped

FX Daily, December 17: Dollar Thumped

2020-12-17

Overview: The prospects of a UK-EU deal and US stimulus continue to underwrite risk appetites and weigh on the dollar. Equity markets are moving higher. Led by Australia and China, the MSCI Asia Pacific Index rose to new record highs, while Dow Jones Stoxx 600 in Europe is at its best level since February.

Tags: #USD,Australia,China,Currency Movement,Featured,Germany,newsletter