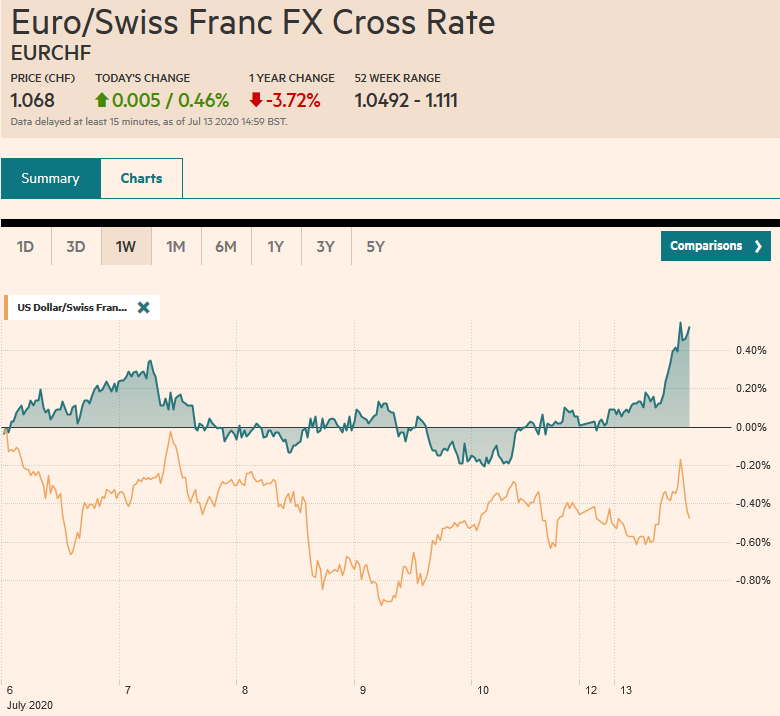

Swiss Franc The Euro has risen by 0.46% to 1.068 EUR/CHF and USD/CHF, July 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: Equities began the week on a firm note in the Asia Pacific region. The Nikkei gained more than 2%, and the profit-taking seen in China ahead of the weekend was a one-day phenomenon. The Shanghai Composite rose 1.8%, and the Shenzhen Composite surged 3.5%. Taiwan and South Korea markets also rallied more than 1%. European and US stocks enjoy more modest gains of around 0.5%-0.6%. Benchmark 10-year yields are mostly 2-3 bp higher, though the US 10-year Treasury yield is a little softer around 64 bp. European sovereigns are expected to sell around 36 bln euros of bonds this week, while

Topics:

Marc Chandler considers the following as important: $CNY, 4) FX Trends, 4.) Marc to Market, China, Currency Movement, Featured, newsletter, Oil, Poland, South Korea, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Krypto-Ausblick 2025: Stehen Bitcoin, Ethereum & Co. vor einem Boom oder Einbruch?

Connor O'Keeffe writes The Establishment’s “Principles” Are Fake

Per Bylund writes Bitcoiners’ Guide to Austrian Economics

Ron Paul writes What Are We Doing in Syria?

Swiss FrancThe Euro has risen by 0.46% to 1.068 |

EUR/CHF and USD/CHF, July 13(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: Equities began the week on a firm note in the Asia Pacific region. The Nikkei gained more than 2%, and the profit-taking seen in China ahead of the weekend was a one-day phenomenon. The Shanghai Composite rose 1.8%, and the Shenzhen Composite surged 3.5%. Taiwan and South Korea markets also rallied more than 1%. European and US stocks enjoy more modest gains of around 0.5%-0.6%. Benchmark 10-year yields are mostly 2-3 bp higher, though the US 10-year Treasury yield is a little softer around 64 bp. European sovereigns are expected to sell around 36 bln euros of bonds this week, while there may be $20 bln investment-grade bonds coming to market from US names this week. The dollar is narrowly mixed. The Swedish krona, Australian dollar, Canadian dollar, and euro are firmer, while the Norwegian krone, Japanese yen, and New Zealand dollar are nursing small losses. Emerging market currencies are similarly mixed, leaving the JP Morgan Emerging Market Currency Index virtually flat after rising by about 0.35% last week. Gold has come back firmer after slipping in the last couple of sessions and is trying to re-establish a foothold above $1800. OPEC+ may be ready to bring more output next month, and this is weighing on crude oil prices. The September WTI contract is struggling to hold above $40 a barrel. |

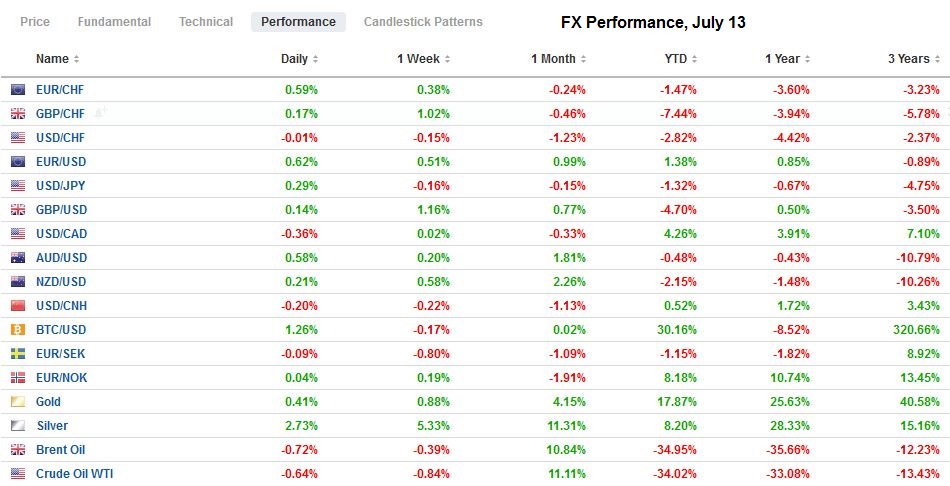

FX Performance, July 13 - Click to enlarge |

Asia Pacific

First officials in China stir the pot, buy stocks was patriotic. People bought stocks. Stocks soared. Then the regulator of banking and insurance sectors cautioned against “illegal speculation,” and stocks fell. Last week’s data showed total social funding (bank and nonbank financial intermediaries) has risen by almost 13% in H1 20. In addition to these funds, savings from the wealth-management products, that are often variable-rate fixed-income investments, may have been freed up as well as the risk of defaults increase.

South Korea’s trade in the first ten days of July suggest better regional trade is taking place. Exports fell 11% in June (year-over-year) but in the first part of July were off 1.7%. Semiconductor chip exports rose 7.7% after a flat showing in June,m though wireless device exports fell 9.7%. Auto exports increased by 7.3%, but parts shipments fell by a third. Ship exports soared by over 300%. Exports to China increased by 9.4%, and exports to the US rose by 7.3%. Shipments to Japan fell by more than 20%. Imports fell by 9.1%. Oil purchases slumped by nearly a third. Imports of chip fabrication machinery surged by 85%.

Japan’s tertiary activity (service sector) slipped 2.1% in May after a revised 7.7% decline in April (initially 6.0%). The revision fully made up for smaller than expected May decline, which had been anticipated closer to 3.8%. The BOJ’s two-day meeting starts tomorrow. All of the regions were downgraded in a BOJ branch report out late last week. The BOJ itself is not expected to change policy but can be expected to promise to take more action if necessary.

The dollar has been confined to about 15 bps on either side of JPY106.95. There are $1.2 bln of options expiring today between JPY106.75 and JPY106.85. On the upside, the JPY107.40-50 area looks to be a solid cap and backed by a $545 mln option expire today at JPY107.50. The Australian dollar is firm but is not going anyplace quickly, either. It is capped near $0.7000 and found support near $0.6920 at the end of last week. The greenback has stayed within 50-pips of CNY7.0. The PBOC set the dollar’s reference rate today a little weaker than the models suggested. It also injected CNY50 bln via “reverse repos,” the first open-market operation in 11 sessions, and helped ease money market rates. China’s 10-year yield edged a couple basis points higher to almost 3.05%.

Europe

Ahead this week’s summit that is to address the European Recovery Plan and the EU’s seven-year budget, European Council President Michel offered new compromises. One obvious take away is that a deal that would ensure unanimity has not been found. Michel offered a slightly smaller overall EU budget while keeping the 750 bln euro Recovery Fund intact. There is disagreement about how the funds should be distributed. How much of a veto should the countries retain?

The mix between loans and grants, and conditionality that should be attached, remain open issues too. A second take away from recent developments is that that the opposition is more than the Frugal Four (Denmark, Sweden, Austria, and the Netherlands). Finland stands them, but more, many others allied last week to defeat the German, French, Italian, and Spanish-backed candidate to lead the eurozone finance ministers. Ironically, there is not much debate about a common bond that seemed to have dominated earlier discussions. It appears, as a last resort, Michel is offering budget rebates that may be sufficient to allow some compromise. However, the decision needs to be unanimous, and the impact on domestic political consideration cannot be taken out of the equation.

In a closely contested election in Poland, it appears that President Duda will have another term. The voter turnout looks to be a modern record. The challenger, Trzaskowski, claimed victory too and may formally protest the results. Duda’s Law and Justice Party lost the upper house of parliament last year, but it has not compromised. It looks like another snub at Brussels ahead of the summit. The Polish zloty is virtually unchanged on the day and over the past month.

The US has announced a 25% tariff on $1.3 bln of French consumer goods (e.g., cosmetics, ceramics, cookware, and handbags, but not wine or cheese) over the digital tax, which the US argues, discriminates against US companies. The tax will be not be collected for 180 days as France has not begun collecting its digital tax. Hopes of a break-through at the OECD, seem ill-founded. European-US trade tensions are at risk of escalating in the coming months. That said, one area that the US does appear to be making headway is the banning of Huawei.

The euro has held about a 35-tick range above $1.1300 today. Last week’s high was near $1.1370. It looks too far to be re-tested today. An expiring option for a little more than 720 mln euros at $1.1350 may be a sufficient cap today. That said, the North American session seems to have been biased to the upside recently. Still, there is a 2.1 bln euro option at $1.13 that expires tomorrow. For the third consecutive session, sterling’s upside has been checked by sales around $1.2670. Support is seen a little below $1.2600, and it looks poised to try the upside again in North America.

America

The chock-filled US economic calendar begins slowly. The June budget statement and the Fed’s Williams and Kaplan speak. In the past, the NY Fed President was part of the troika of leaders, but Williams does not appear to be regarded in those terms. Some may link it to the seemingly petty personnel decisions, made early in his tenure at the NY Fed, left the execution arm of the Federal Reserve System, somewhat ill-positioned to deal the challenges both repo and Covid-related. The Treasury sells more bills this week but no coupons. Strong demand was seen at last week’s coupon auctions that saw the five-year yield fall to record lows, and the 10-year was sold at record-low yields. The US 30-year yield fell to 1.25% before recovering ahead of the weekend.

The financial focus may shift to Q2 bank earnings this week. Financials have underperformed the market. The slump in spending and investing squeeze lenders, and many current borrowers are stressed. Trading and underwriting, as well as re-financing, may have cushioned the blow. Net interest margin (similar to the gross margin of a non-financial business) appears to have widened too.

The tit-for-tat with China is likely to continue. Beijing has sanctioned Senators Rubio and Cruz over legislation they sponsored to sanction China and Chinese officials over human rights violations. The Trump Administration has signaled its intent to take additional action in the coming days. Apps, like TikTok and WeChat, reports suggest may be banned or curtailed.

The central bank meeting in the middle of the week is Canada’s highlight after a stronger than expected jobs report at the end of last week (952k vs. the median forecast in the Bloomberg survey for 700k). The Bank of Canada is expected to stand pat, but will likely attest to its willingness to scale its efforts if necessary. Mexico’s economic calendar is light this week.

The US dollar rose to about CAD1.3630 ahead of the weekend, the best level here in July. However, it looks poised to re-test support near CAD1.3500, which corresponds to last week’s lows and the 200-day moving average. A convincing break of CAD1.3500 could open the door to a re-test on last month’s low near CAD1.3315. With a few minor exceptions, the greenback has been confined between MXN22.00 and MXN23.00 for the past month. It was a little firmer in Asia and the European morning, but the relatively high rates (~4.8% on three-month cetes) remains attractive, especially given the implied volatility is near three-month lows (~15.5%).

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, June 8: Monday Blues: Consolidation Threatened

FX Daily, June 8: Monday Blues: Consolidation Threatened

Overview: The MSCI Asia Pacific Index rose for a sixth consecutive session. Japan, Taiwan, Singapore, and Indonesian markets advanced more than 1%. European bourses are mixed, with the peripheral shares doing better than the core, leaving the Dow Jones Stoxx 600 about 0.5% lower near midday after surging 2.5% ahead the weekend. US shares are firm, as is the 10-year yields, hovering near 92 bp.

FX Daily, July 10: Surge in Coronavirus Spooks Investors as China Takes Profits

FX Daily, July 10: Surge in Coronavirus Spooks Investors as China Takes Profits

Record fatalities in a few US states, coupled with new travel restrictions in Italy and Australia, have given markets a pause ahead of the weekend. News that two state-backed funds in China took profits snapped the eight-day advance in Shanghai at the same time as there is an attempt to rein in the use of margin.

FX Daily, February 19: Investors’ Confidence Snaps Back

FX Daily, February 19: Investors’ Confidence Snaps Back

Overview: After shunning risk yesterday, investors re-entered the fray today, and the animal spirits returned. The MSCI Asia Pacific Index snapped a four-day slide, and China’s markets were among the few losers in the region today. Europe’s Dow Jones Stoxx 600 recovered yesterday’s losses in full and is again at record highs. US shares are also trading firmer and are poised to recoup yesterday’s decline.

FX Daily, April 2: Optimism on Oil Deal Steadies Risk Appetites…for the Moment

FX Daily, April 2: Optimism on Oil Deal Steadies Risk Appetites…for the Moment

Overview: After US stocks dropped more than 4% yesterday, investor sentiment has improved, apparently sparked by ideas that the pain will force oil producers to find a way to reduce supply. Oil prices have surged, with the May WTI contract rallying around 7%. Asia Pacific equities were mostly higher, with Japan and Australia the notable exceptions.

FX Daily, May 11: Quiet Start to New Week

FX Daily, May 11: Quiet Start to New Week

Overview: The new week begins slowly in the capital markets. Many markets in the Asia Pacific region, including Japan, Hong Kong, and Australia, gained over 1%, but European and US shares are heavier. Benchmarks off all three regions rallied by 3.4%-3.5% over the past two weeks. Bond markets are also little changed, with the US 10-year benchmark just below 70 bp ahead of this week’s record refunding.

FX Daily, June 2: Greenback’s Slide Continues

FX Daily, June 2: Greenback’s Slide Continues

Overview: Liquidity trumps everything else. US equities shrugged off the national guard being called into action in nearly a third of US states, and the S&P 500 closed yesterday at nearly three-month highs. Asia Pacific markets followed suit. Most markets in the region rose by more than 1%. The notable exceptions were Australia and China, where benchmarks rose by 0.2%-0.3%. The Dow Jones Stoxx 600 is up more than 1% in the European morning.

FX Daily, July 1: Second Verse Can’t be Worse than the First, Can it?

FX Daily, July 1: Second Verse Can’t be Worse than the First, Can it?

The resurgence of the contagion in the US has stopped or reversed an estimated 40% of the re-openings, but the appetite for risk has begun the second half on a firm note, helped by manufacturing PMIs that were above preliminary estimates or better than expected. Except for Tokyo and Seoul, equities in the Asia Pacific region rose. The MSCI Asia Pacific Index rose almost 15.5% in Q2.

FX Daily, July 2: Dollar Thumped Ahead of US Jobs Report

FX Daily, July 2: Dollar Thumped Ahead of US Jobs Report

Market optimism over the possibility of a vaccine in early 2021 overshadowed the continued surge in US cases, where the 50k-a-day threshold of new cases has been breached. Following the NASDAQ close yesterday at record highs, global equities have advanced. Led by Hong Kong returning from yesterday’s holiday, Asia Pacific equities rallied. Most local markets rose by more than 1%, though Tokyo and Taiwan lagged.

Tags: #USD,$CNY,China,Currency Movement,Featured,newsletter,OIL,Poland,South Korea