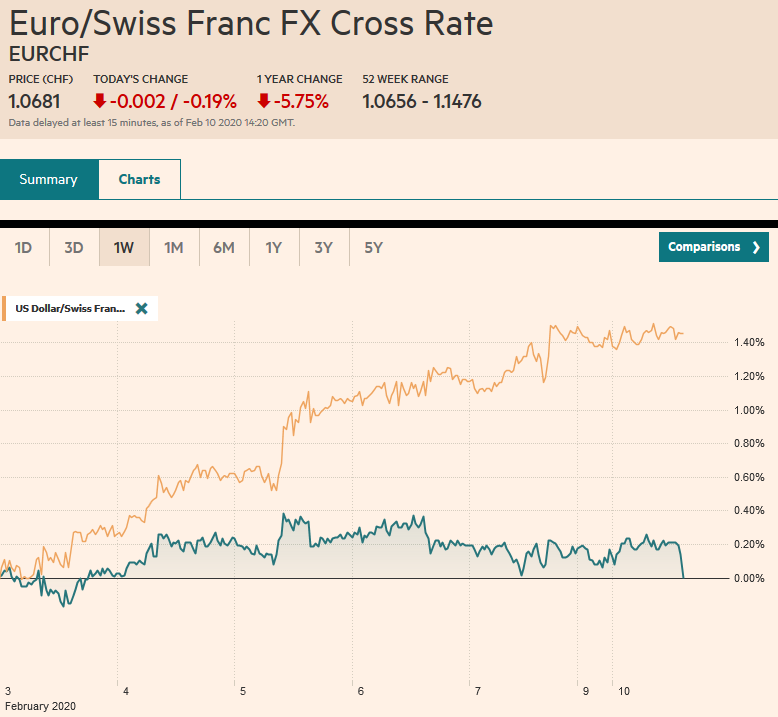

Swiss Franc The Euro has fallen by 0.19% to 1.0681 EUR/CHF and USD/CHF, February 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The global capital markets have begun the new week on a cautious tone as investors seek to assess the latest news on the new coronavirus. Nearly all the markets in Asia fell but China. European bourses are lower as well, with the Dow Jones Stoxx 600 off about 0.3%. US shares are soft but little changed. Benchmark yields are slightly lower in Europe after Asia Pacific bond yields eased to catch-up the move in the US ahead of the weekend. The US 10-year yield is around 1.57%, The dollar has a heavier bias today, slipping against most of the major currencies, led by the Norwegian

Topics:

Marc Chandler considers the following as important: 4) FX Trends, 4.) Marc to Market, China, Currency Movement, Featured, newsletter, Norway, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Krypto-Ausblick 2025: Stehen Bitcoin, Ethereum & Co. vor einem Boom oder Einbruch?

Connor O'Keeffe writes The Establishment’s “Principles” Are Fake

Per Bylund writes Bitcoiners’ Guide to Austrian Economics

Ron Paul writes What Are We Doing in Syria?

Swiss FrancThe Euro has fallen by 0.19% to 1.0681 |

EUR/CHF and USD/CHF, February 10(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The global capital markets have begun the new week on a cautious tone as investors seek to assess the latest news on the new coronavirus. Nearly all the markets in Asia fell but China. European bourses are lower as well, with the Dow Jones Stoxx 600 off about 0.3%. US shares are soft but little changed. Benchmark yields are slightly lower in Europe after Asia Pacific bond yields eased to catch-up the move in the US ahead of the weekend. The US 10-year yield is around 1.57%, The dollar has a heavier bias today, slipping against most of the major currencies, led by the Norwegian krone on the back of a surprisingly strong inflation report. Emerging market currencies are also mostly higher, with the Chinese yuan and Russian rouble vying for the top position, with both up almost 0.3%. After falling by 1.1% over the past two sessions, the JP Morgan Emerging Markets Currency Index is up by about 0.15%. Today late in the European morning. Gold is higher for the fourth consecutive sessions, and oil is in a 50-cent range on either side of the $50 a barrel mark. |

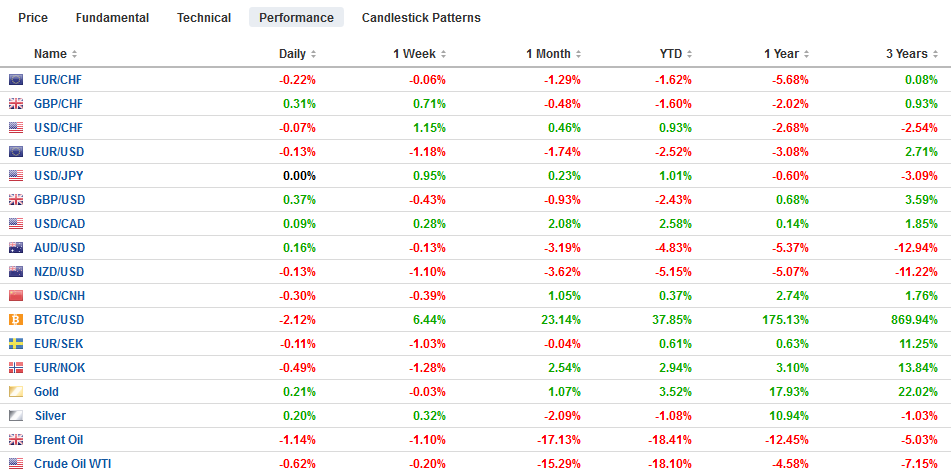

FX Performance, February 10 - Click to enlarge |

Asia Pacific

Reports suggest a mixed re-opening of China’s manufacturing companies. Some are extending the shutdown extension another week, and others are suggesting not re-starting until March. Manufacturing in China is labor-intensive, and there can be no work without masks. Two masks per day per worker are needed, and reports suggest shortages. Separately, reports indicate that officials have spent out half of the funds (CNY31.5 or ~$4.5 bln) that have already been allocated (CNY~72 bln) to combat the virus. The PBOC announced a new weekly facility to provide “re-lending” funds to major banks and several local banks that will be re-lend to businesses 100 bp below the one-year Loan Prime Rate of 3.15%.

China reported January CPI jumped to 5.4% from 4.5% in December. Economists had expected something a little shy of 5%. Food prices accelerated to 20.6% from 17.4%. Producer prices ended a six-month deflationary bout and rose 0.1% year-over-year. The news has little policy significance and does pick up the full impact of the coronavirus.

Reports indicate that China’s oil demand has fallen by about 3.2 mln barrel per day, and as some industry re-opens, the decline could fall to around 2.5 mln bpd. Next month, demand is projected to be about 1.4 mln bpd less than in Q4 19. OPEC+ awaits Russia’s decision whether it will go along with an extension of existing cuts until the end of the year and some additional cuts in H1 20. Meanwhile, Chinese commodity importers are declaring force majeure to turn back shipments, including reports of 35 liquid natural gas cargoes. Australia reportedly may be the most impacted.

The dollar is in about a third of a yen range above JPY109.50, where a nearly $610 mln option is placed that expires today. The 20-day moving average also comes in near there. On the topside, he JPY110 area capped upticks last week. The Australian dollar fell to a marginal new multi-year low of $0.6660 before rebounding and briefly poking through $0.6700 before encountering new sales. Support is now pegged near $0.6680, and resistance is spotted around $0.6720. The dollar was turned back from CNY7.0 and returned to the pre-weekend low near CNY6.9775. The CNY6.95 area may offer a near-term base.

Europe

The specter haunting Europe is not socialism, after all at least mixed economies or social markets prevail, but nationalism. In Germany, Merkel succeeded in unwinding the selection of FDP’s Kemmerich as Premier of Thuringia to oust the Left Premier, who seemed poised to continue leading a minority government with the support of the SPD and Greens. Kemmerich’s ascension was only possible with the help of the nationalist AfD, for which all the major parties have renounced cooperating. Berlin insisted on enforcing the national pact on the local government by sheer power. However, a political vacuum in Germany has opened as the dramatic decline in support for both the CDU and SPD reflects. A programmatic solution is necessary sooner or later. Meanwhile, Sinn Fein’s ability to recast itself as a populist-nationalist force seemed to have struck paydirt in Ireland. Its share of the vote appears to have jumped to a little more than 22% compared with 14% in 2016. Aside from the hubris of small differences, little separates the two main parties (Fine Gael and the Fianna Fail), which divided a little less than half of the vote. The preliminary results suggest that Sinn Fein, which ran candidates in 42 districts, may have secured as many as 37 seats in the new parliament.

Staying with the political theme, German politics took a bigger turn than the local government in an East German state. The national political situation was thrown open by the controversial head of the CDU, Annegret Kramp-Karrenbauer (AKK), Merkel’s handpicked successor indicating that she will step down and not replace Merkel as the Chancellor candidate. AKK and Merkel appear to have had a falling out over several issues, and it is not clear how much AKK is being pushed, but she does appear to have lost Merkel’s support.

Italy joined Germany, France, and Spain in reporting shockingly poor industrial production figures for December. Germany, France, and Spain reported last week and all widely missed estimates. Today it was Italy’s turn. Economists had expected a decline of around 0.6%, and instead, it plummeted by 2.7% on the month. It was the worst since January 2018, and November’s 0.1% gain was revised away. Italy’s industrial output has not risen since August. The data warns that 1) the economic downturn in Q4 could be steeper than the 0.3% reported, and 2) without improvement, Italy may have slipped into a recession (two contracting quarters). The political fallout could see more support for the League in spring local elections.

The euro has been confined to less than 10 ticks on either side of $1.0950, where an option for about 580 mln euros is set to expire today. The lower yields and low volatility makes the euro an attractive funding currency for levered accounts. Sterling slipped to fresh 2.5-month lows near $1.2870 before finding a bid that helped it resurface above $1.29. There is an option for almost GBP380 stuck there that will be cut today. The pre-weekend high was near $1.2960, and a move above there would help lift the technical tone. Norway’s January CPI was expected to be flat, but some basket-revisions and a jump in food prices say a 0.7% increase, which lifted the year-over-year rate to 1.8% from 1.4%. The underlying rate rose to 2.9% from 1.8%. The data reinforces ideas that Norway’s central bank, Norges Bank, will keep policy steady. The euro is testing support near NOK10.10. Sweden’s Riksbank meets this week and is expected to stand pat after hiking rates to zero at the end of last year. The Swedish krona has been sold for the Norwegian krone today.

America

It is a light diary for North America today. Three regional Fed presidents speak today (Bowman, Daly, and Harker. Despite the dissents during last year’s easing operation, there is a consensus now, and it favors a standpat policy. However, Powell is likely to open the door to a possible ease at his Congressional testimony that begins tomorrow. The idea is that the coronavirus could impact the world economy, given the size and linkages with China. It could lead to a retrenchment of risk, weigh on commodity prices, and fuel further dollar appreciation. The gap between the markets and the Federal Reserve interest rate expectations is wide. The December 2020 fed funds futures imply 1.235% effective average compared with the current average near 1.59%.

Canada reports January housing starts and December permits. These are not the data that typically moves the market. Canada’s employment data before the weekend was sufficient to keep expectations for the Bank of Canada steady. A rate cut is still anticipated, but not until later in Q2. Before Mexico’s central bank meets on Feb 13, it will report industrial output figures for December. Continued weakness will underscore the likelihood of another rate cut. Mexico’s high real and nominal rates underpin the peso, which is among the best-performing currencies this year and last.

Although the US dollar managed to close above CAD1.32 last week for the first time since last November, it does not necessarily signal a breakout. The greenback continues to consolidate. The technical indicators remain stretched and about to turn lower. We continue to look for a top around current levels. A break of CAD1.3260 would strengthen our conviction. The dollar is trading in a narrow range off of the pre-weekend high (~MXN18.8275) against the Mexican peso. Initial support for the US dollar is seen near MXN18.70.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,China,Currency Movement,Featured,newsletter,Norway