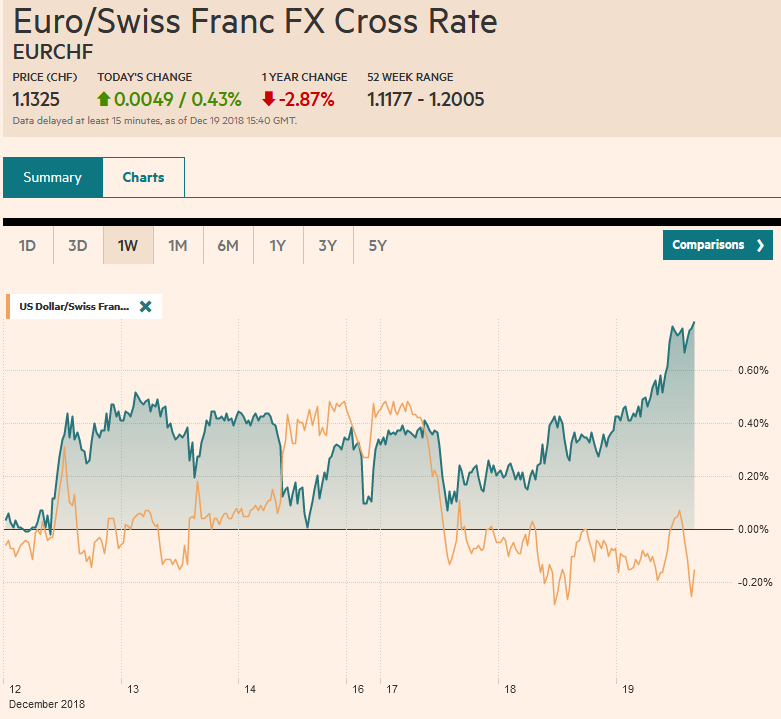

Swiss Franc The Euro has risen by 0.43% at 1.1325 EUR/CHF and USD/CHF, December 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The failure of the S&P 500 to sustain even modest upside momentum yesterday is keeping traders on edge today, though another attempt on the upside is likely. Asian equities were mixed, with Chinese and Japanese shares lower. The Nikkei closed below the 21000 support level. European shares are struggling to hold on it early gains, though Italy’s stocks and bonds have surged on reports of an agreement with the EU. The Bank of Japan and the Bank of England meet tomorrow, but neither is expected to change policy. That leaves today’s

Topics:

Marc Chandler considers the following as important: 4) FX Trends, AUD, CAD, EUR, Featured, GBP, JPY, newsletter, USD

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has risen by 0.43% at 1.1325 |

EUR/CHF and USD/CHF, December 19(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The failure of the S&P 500 to sustain even modest upside momentum yesterday is keeping traders on edge today, though another attempt on the upside is likely. Asian equities were mixed, with Chinese and Japanese shares lower. The Nikkei closed below the 21000 support level. European shares are struggling to hold on it early gains, though Italy’s stocks and bonds have surged on reports of an agreement with the EU. The Bank of Japan and the Bank of England meet tomorrow, but neither is expected to change policy. That leaves today’s FOMC meeting as the last big event of the year. The US dollar is trading heavily across the board amid market anticipation of dovish signals today. |

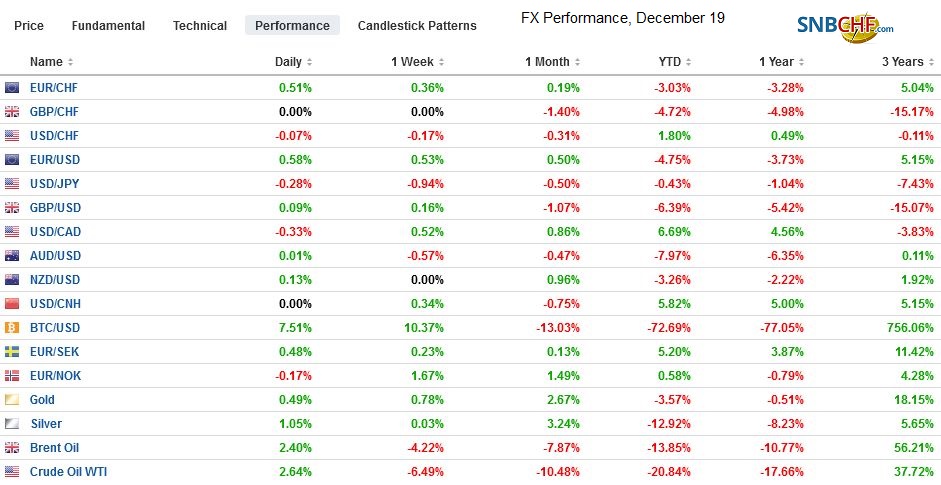

FX Performance, December 19 - Click to enlarge |

Asia Pacific

Japan reported a larger than expected November trade deficit. The JPY737.3 bln deficit compares with a JPY450 bln deficit in October and forecasts for a JPY630 bln shortfall. Exports dried up, eking out a 0.1% gain from a year ago, down from 8.2% growth in October. Imports slowed to 12.5% from nearly 20% in October. To put the numbers in perspective, consider that over the past 12-months, Japan has reported an average monthly deficit of JPY65.6 bln. Last November the 12-month average was a JPY265.6 bln surplus. Japan’s current account surplus, like Switzerland’s, is driven by the investment income account, not the trade balance. Exports to the US rose 1.6% and 3.9% to Europe. However, exports to China slowed to 0.4%. However, the volume of exports to China fell 5.8%, while overall export volumes fell (1.9%) for the second decline in three months.

China’s annual economic policy meeting continues, and it is here where new initiatives may be announced. Many observers bemoaned the fact that President Xi speech did not contain new stimulative measures. However, a speech to celebrate the 40th anniversary of the Deng Xiaoping reforms and the economic modernization of China is not the place to look for proposals on how to fix or reform that modernization. Reports suggest that the US and Chinese officials will resume their face-to-face trade talks next month.

The dollar slipped to a marginal new low below JPY112.20, for the first time since late October, when it traded near JPY111.30. Since then the greenback has been mostly in a JPY112.25-JPY114.00 range. There are almost $1.5 bln in JPY112.40-50 options that expire today several hours ahead of the outcome of the FOMC meeting. The Chinese yuan remains in tighter ranges that one would expect given the movement of other currencies against the dollar. The Australian dollar toyed with the $0.7200 level that had previously been support and now serves as resistance. The Aussie seems comfortable in around a 25-tick range on either side of it.

Europe

As the year winds down, the nationalist/populist government in Italy appears to have reached an agreement with the EU over next year’s budget. The details are not yet fully known, but it seems that some compromises have been made on both sides. Italian bonds and stocks have rallied strongly. The 10-year yield is off nearly nine basis points to 2.85%. The yield peaked almost 100 bp higher n mid-October. It was nearer 1.80% before the spring elections. The premium over Germany was less than 120 bp then before topping in October near 325 bp. Today it is slipping below 260 bp for the first time since September. Bank stocks have rallied strongly(3%+), but the volatility is such that, the bank share index has surged more than 3% in at least one session in each of the past three weeks as well. The challenges Italy faces have not gone away. The agreement with the EU ensures the problem is chronic rather than acute. With a budget agreement, which is still making its way through the Italian parliament, the next focus is likely politics with jockeying for position ahead of the EU Parliament elections next spring.

The UK November CPI was in line with expectations. The headline rose 0.2% for a 2.3% year-over-year pace, which is down slightly from 2.4%. The core rate also moderated slightly to 1.8% from 1.9%. The base effect points to a further softening of prices here in December before rebounding in January. Before the Bank of England meets tomorrow, the UK will report November retail sales. A modest recovery is expected after October declines. Meanwhile, overshadowing the macroeconomics, are EU (and UK) preparations for Brexit. The domestic brinkmanship drama continues, and the next window of resolution is about a month away.

The US two-year premium over Germany has trended lower since peaking on November 8 near 3.54%. It is quoted near 3.24% today, which has not been seen since early September. There is not a one-to-one correspondence between the interest rate differential and the exchange rate. We find the direction of movement is important for the foreign exchange market. Still, given the change in the rate differential, many expected the euro to firmer. In early September it was nearly two cents higher. The euro is firm as it poked above $1.14 in late morning trade on the Continent. It has toyed with this area on most days since mid-November, but the last time it closed above it ($1.14) was November 22. There is a nearly 800 mln euro option expiring today that is struck at $1.1450, which could come into play in the US session. On the downside, there are nearly 1.6 bln euros in options between $1.1360 and $1.1375 that will be cut today. For its part, sterling is in about a quarter-cent range around $1.2660, the previous low for the year. Yesterday’s high was a little above $1.2705. It stopped just in front of the 20-day moving average, which is found there today. It has not closed above this moving average for more than a month.

North America

The FOMC meeting is front and center today. The broad call for the Fed to be free less forceful in raising rates next year and being more flexible and data dependent is hardly controversial. However, it is also not particularly insightful. The Fed has indicated through its forecasts that it intended on raising rates three times next year rather than the four in anticipated for this year. That implies a slower pace than that once a quarter. This coupled press conferences after every meeting imply greater flexibility. These combined with the maturing business cycle and the proximity of the Fed’s targets implies greater data dependency than may have been evident.

Many observers who argue that the Fed should not raise rates note that price pressures are moderating not rising and that the decline in oil prices is deflationary. With full employment and the economy growing above trend (even as it slows from the unreasonably strong 4.2% annualized pace in Q2), a monetary setting that has the real fed funds target rate at zero is not appropriate. The drop in oil prices will hurt capex that has become dependent on the sector, but for the oil consumers, which includes households, the decline in oil prices will boost disposable income, which means consumption. Some observers note that the Fed has rarely hiked rates in the face of the pace and magnitude of the stock market decline or the decline in oil prices. Context matters and the fact that US asset prices valuation looked rich may a mitigating factor. Moreover, after the Great Financial Crisis, there is some desire to break the moral hazard associated with the idea of a central bank put.

That said, Fed officials will likely revise their forecasts. Rather than pencil in three hikes for next, we suspect that the median will slip to two. However, we still think it is unreasonable to expect the Fed to signal that the September hike or today’s is the last. Like forecasting other economic variables, there is a range of estimates for the neutral rate. Most Fed officials have it closer to 3.0%, the middle of the 2.5%-3.5% range that was provided in September. We continue to think movement toward there in this cycle is still the most likely scenario. A dovish hike seems to be the most widely expected outcome, and that still leaves room for buy the rumor sell the fact type of activity.

Not to be lost in the shuffle, Canada reports November CPI figures. The headline pace is expected to moderate to 1.8% from 2.4%, largely reflecting the drop in energy prices. The core rates are expected to be steady. The Canadian dollar fell to new lows for the year yesterday. The US dollar tested CAD1.35 and is consolidating in a narrow range today. Initial support near CAD1.3445 has been successfully tested in the European morning. The US reports existing home sales, and after a 1.4% rise in October, a small 0.4% decline is expected in November. Yesterday’s starts and permits figures were better than expected. Housing is among the most interest-rate sensitive sectors. It may be too soon to expect the decline in rates to boost affordability and activity.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,Featured,newsletter