Nadia Gharbi

October 19, 2018

Perspectives Pictet

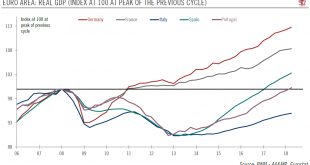

September growth and unemployment rates show how far it has come.In two decades, Portugal has gone through a boom (1996-2001), a slump (2002-2007), a deep recession (2008-2013), a timid recovery (2014-2016) and now a robust economic expansion. In 2017, real GDP grew by 2.8%, its fastest pace since 2000. This is even more remarkable when considering that the country exited its bailout programme only in mid-2014. Investment and robust exports were the main growth drivers in 2017.Starting in...

Read More »

Laureline Chatelain and Nadia Gharbi

October 18, 2018

Perspectives Pictet

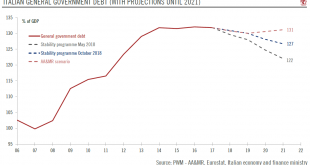

Rome’s budget plans put it on a collision course with the European Commission.The Italian government has submitted its 2019 draft budget plan (DBP) to the European Commission. The proposed DBP is not in line with European Union rules and sets the government on a collision course with the European authorities.Several elements within the Italian government’s budget plan have been raising eyebrows. First, the plans’ economic assumptions seem too optimistic to us, and there is a risk that the...

Read More »

Thomas Costerg

October 18, 2018

Perspectives Pictet

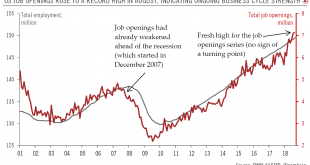

No sign of a let-up in the US business cycle as job openings continue to rise.We particularly like job openings data as an indicator for a turning point in the US macroeconomic cycle, even though this series has not much history (data start in December 2000), and in spite of its long lag to release (we just had data for August, i.e. it is more than two months old now).Still, job openings did a rather good job of indicating an inflexion point right before the global financial crisis: the US...

Read More »

Luc Luyet

October 17, 2018

Perspectives Pictet

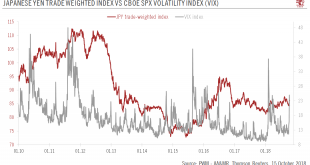

Limited upside for the dollar against the yen, but significant downside will take time.While widening interest rate differentials are supportive of the US dollar against the yen, if rates rise too far and too fast, they can help the yen against the dollar, as recent financial market volatility has shown. In October, the Japanese yen appreciated by 1.9% against the dollar and outperformed all other major currencies.Coupled with extreme fundamental yen undervaluation, the potential for the...

Read More »

Dong Chen

October 16, 2018

Perspectives Pictet

Inflation is unlikely to be a constraint on central bank’s policy.The headline consumer price index (CPI) in China picked up slightly in September, rising by 2.5% year-over-year (y-o-y) compared with 2.3% in August, driven by higher food price and fuel prices. Excluding food and energy, core inflation in China actually eased to 1.7% y-o-y in September from 2.0% in August.Looking forward, we see some moderate upward pressure on Chinese headline inflation due to tariffs on US imports and...

Read More »

Perspectives Pictet

October 16, 2018

Uncertainty is becoming the norm in our fast-changing world and business owners and investors are looking for answers in how to turn volatility into opportunity. A range of solutions were discussed in detail at the fifth edition of the Pictet Entrepreneur Summit, held in Geneva at the end of August. A key takeaway from this year’s event was put best by senior managing partner Nicolas Pictet, who said that established ideas about how business, trade and politics work are quickly shifting....

Read More »

Stéphane Bob

October 16, 2018

Perspectives Pictet

[embedded content]

Uncertainty is becoming the norm in our fast-changing world and business owners and investors are looking for answers in how to turn volatility into opportunity. A range of solutions were discussed in detail at the fifth edition of the Pictet Entrepreneur Summit, held in Geneva at the end of August. A key takeaway from this year’s event was put best by senior managing partner Nicolas Pictet, who said that established ideas about how business, trade and politics work are...

Read More »

Cesar Perez Ruiz

October 15, 2018

Perspectives Pictet

The CIO office’s view of the week ahead.US equities declined roughly 7% over six days up to last Thursday. While the decline is in line with the median drawdown level since 2007, it was notable for its length, given the average drawdowns over the same time period lasted 40 days, rather than six. Most likely, investors were reacting to the higher risk environment created by rising bond yields. However, compared with February’s sell-off, there is less exuberance on the technical side....

Read More »

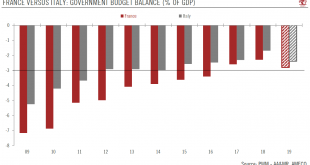

Nadia Gharbi

October 12, 2018

Perspectives Pictet

Italy’s structural weakness explain higher level of concern around its deficit target.Each EU member state is currently preparing 2019 budget plans for formal submission to the European Commission (EC) before mid-October. Among them, France and Italy’s budget plans have been raising eyebrows. Why is the EC concerned about Italy’s proposed 2.4% GDP deficit target for 2019 and not France’s target of 2.8%? Is Italy being treated unfairly by its European partners and by markets? Italy and France...

Read More »

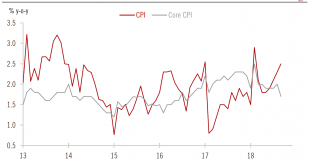

Thomas Costerg

October 11, 2018

Perspectives Pictet

While we await the effect of import tariffs, inflation has still not taken off in the US. The Fed is unlikely to be swayed from its current rate tightening routine.Core consumer-price index (CPI) inflation rose a modest 0.12% month on month (m-o-m) in September, again undershooting market expectations, and the year-on-year (y-o-y) print stayed unchanged at 2.2% –a relatively benign outcome given the flourishing US economy and the tight labour market.Core inflation (excluding energy and food...

Read More »

Perspectives Pictet

Perspectives Pictet