Perspectives Pictet

Perspectives Pictet

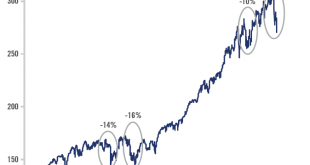

Political gridlock has been good news for US stocks in the past, but Tuesday’s midterm elections come at a time of rising doubts about market prospects.The US midterm elections take place on Tuesday 6 November. Based on recent polls, the most likely outcome is that the Democrats will regain a small majority in the House of Representatives, while the Republicans keep a small majority in the Senate.Should the Democrats take control of the House, Washington D.C. could be back to ‘gridlock as...

Read More »Gridlock in Washington and the markets