Perspectives Pictet

Perspectives Pictet

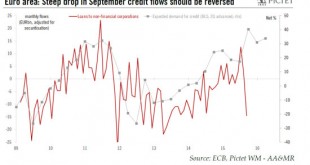

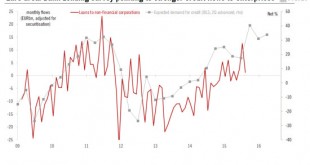

Despite September's setback in credit flows, the credit impulse improved further in Q3, still consistent with growth in domestic demand of close to 2%. Euro area M3 and credit data surprised on the downside in September, contradicting the positive message from the ECB’s Bank Lending Survey (BLS) published last week. Overall, we believe these volatile bank credit flows are likely to rebound strongly in the months ahead, closing the gap with upbeat leading indicators like the BLS (see chart...

Read More »Euro area: big drop in credit flows in September to be reversed