Perspectives Pictet

Perspectives Pictet

The Fed decided not to hike the Fed funds rate in September, but this did not hurt the dollar unduly. Even though the Fed decided against lifting the Fed funds rate in September, the US dollar did not really struggle much. The reason for this lies with the ECB which had overtly declared on 3 September its readiness to press ahead with further quantitative easing, a statement that dented the euro’s appeal. Moreover, too steep a rise in the yen’s value would have a particularly unwelcome...

Read More »Do not hesitate to contact Pictet for an investment proposal. Please contact Zurich Office, the Geneva Office or one of 26 other offices world-wide.

Precious metals: the “VW Effect”

The scandal that has engulfed the VW Group had a big impact on both platinum and palladium as both metals are used in catalytic converters in vehicles. VW’s deceptive practices as regards the real level of nitrogen oxide (NOx) emissions from its diesel vehicles have highlighted the un-ecofriendly features of diesel-powered cars, which can be expected to hit demand. It is also likely to boost the chances of stricter environmental standards on NOx exhaust emissions being pushed through in...

Read More »Equities: the correction rumbles on

Macroview Fears about economic growth have been spreading from China to other markets. “Just where is global growth heading?” seems to be the question uppermost in every investor’s mind. With no clear answers forthcoming to that question, the corrective spell on risk assets ran on through September, dragging all equity markets into the red zone. How steep the slides were can be traced to concerns to the fore at the moment. Markets reliant on demand from China tumbled: Latin America down...

Read More »Higher market volatility should not preclude a rebound in DM equities

After a long period when market volatility was relatively subdued, it has risen sharply this year. The Vix, a widely used measure of equity-market volatility, was in a systemic risk regime for 15 days this year, compared with just two days in 2014 and none at all in 2013, as shown by the chart below. This year’s experience of volatility is still not extensive in a historical comparison, but it still represents a marked change from very subdued conditions in the previous two years. What...

Read More »US ISM surveys: marked contrast between activity in manufacturing and services

The ISM indices are diverging quite noticeably. The Manufacturing index fell to almost 50% in September, whereas its Non-Manufacturing counterpart – though steeply down m-o-m in September – remained pitched at much higher levels. Taken together, they point towards economic growth running above 3.5% in Q3. We continue to expect healthy growth in H2 2015 and 2016. The US economy is currently being confronted simultaneously with strong negative forces (much firmer dollar; weak foreign...

Read More »The Pictet Entrepreneurs Summit

[embedded content] Published: Monday October 05 2015 This edition of “The Entrepreneurs” highlights some of the discussions that took place during the “Pictet Entrepreneurs Summit” held in Geneva in September 2015. This annual invitation-only conference is a platform of exchange for successful entrepreneurs at the crossroads of serial entrepreneurship, personal wealth, and social responsibility.

Read More »The Entrepreneurs, Geneva

This edition of The Entrepreneurs highlights some of the discussions that took place during the "Pictet Entrepreneurs Summit" held in Geneva in September 2015. This annual invitation-only conference is a platform of exchange for successful entrepreneurs at the crossroads of serial entrepreneurship, personal wealth, and social responsibility.

Read More »US employment: a clearly disappointing report

We revise down our GDP growth forecasts from 2.5% to 2.2% for Q3, and from 2.9% to 2.6% for Q4. Our forecast for 2015 remains unchanged at 2.5% whilst our forecast for 2016 is mechanically cut from 2.5% to 2.4%. September’s report was weak on all fronts. Job creation came in below expectations, numbers for previous months were revised down, wages were flat m-o-m and the proxy for household wage incomes fell m-o-m. We now believe the most likely scenario is for the Fed to wait till March...

Read More »Hedge funds: the added value of long/short equity

Macroview Long/short equity managers demonstrate positive alpha generation and protect on the downside as markets succumb to China-led global deflation fears. The end of the summer proved rather turbulent when China weakness caused global markets to freefall. Whilst equities worldwide nosedived, long/short equity managers trimmed their exposures only marginally and took advantage of the sell-off to add to core positions or adapt their short books, outperforming markets in relative terms....

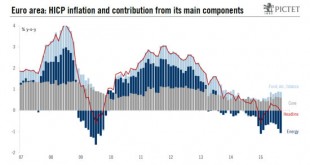

Read More »Euro area: Inflation turns negative in September

– It’s the energy, stupid! The euro area HICP ‘flash’ estimate fell, almost entirely due to the recent drop in commodity prices. But core HICP inflation remained unchanged. The ‘flash’ estimate of euro area Harmonised Index of Consumer Prices (HICP) confirmed what most economists, including at the European Central Bank (ECB), were expecting after the renewed fall in commodity prices over the summer, namely that inflation turned negative again in September. Having reached a trough at -0.6%...

Read More »