Perspectives Pictet

Perspectives Pictet

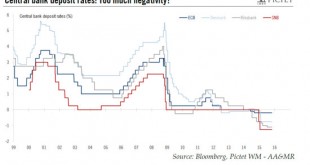

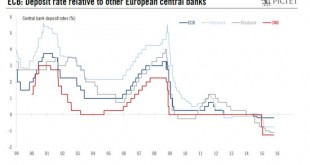

The ECB has explicitly (re-)opened the door to further cuts in the rate applied to its deposit facility, currently standing at -0.20%. The ECB is one of four major central banks to have lowered one of its policy rates into negative territory; the ECB’s rate on the deposit facility used to remunerate banks’ reserves – or the ‘depo rate’ – currently stands at ‑0.20%. The other negative experimenters, in Switzerland, Denmark and Sweden, have even lower repo and deposit rates (see chart below)....

Read More »Q&A on the ECB’s negative rates – Its decision to cut rates again should be FX-dependent