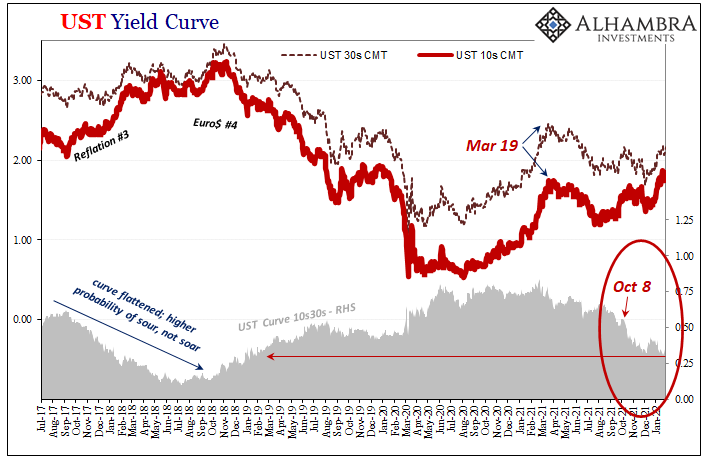

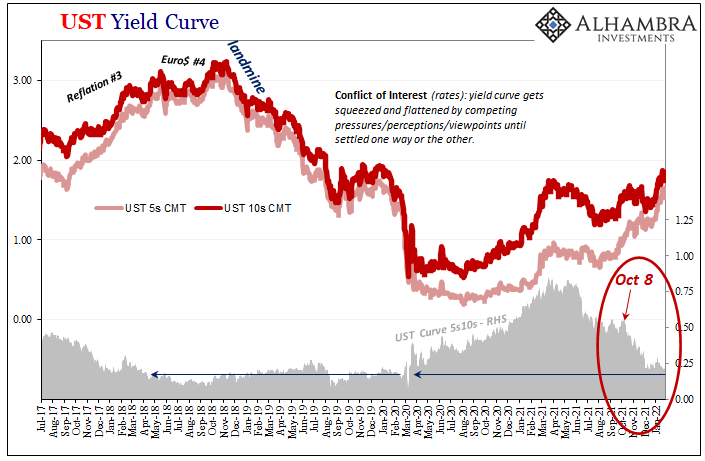

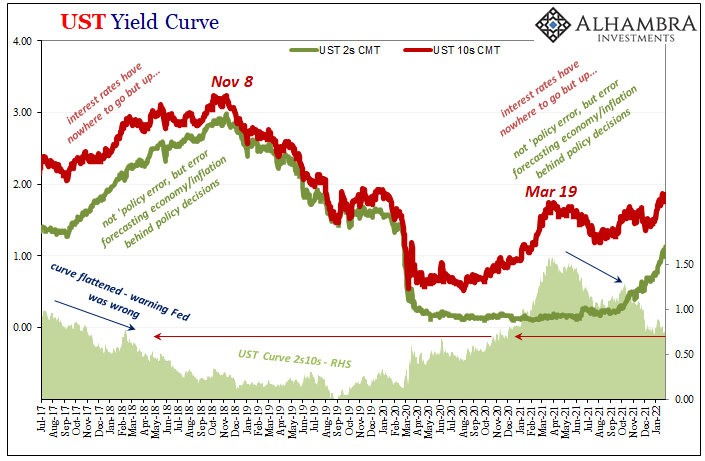

It’s not hard to reason why there continues to be this conflict of interest (rates). On the one hand, impacting the short end of the yield curve, the unemployment rate has taken a tight grip on the FOMC’s limited imagination. The rate hikes are coming and the markets like all mainstream commentary agree that as it stands there’s nothing on the horizon to stop Jay Powell’s hawkishness. And yet, on the other hand, growth and inflation expectations, the long end could not be more resolute that eventually policymakers are going to have to face what is already an incredibly high probability of authorities committing yet another awkward set of cumulative mistakes. . Over here, on this side of the divide, there’s China and now a flood of inventory rather than money.

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, bond yields, bonds, currencies, Deflation, economy, Featured, Federal Reserve/Monetary Policy, FOMC, inflation, Interest rates, jay powell, Markets, newsletter, rate hikes, U.S. Treasuries, Yield Curve

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| It’s not hard to reason why there continues to be this conflict of interest (rates). On the one hand, impacting the short end of the yield curve, the unemployment rate has taken a tight grip on the FOMC’s limited imagination. The rate hikes are coming and the markets like all mainstream commentary agree that as it stands there’s nothing on the horizon to stop Jay Powell’s hawkishness.

And yet, on the other hand, growth and inflation expectations, the long end could not be more resolute that eventually policymakers are going to have to face what is already an incredibly high probability of authorities committing yet another awkward set of cumulative mistakes. |

. |

| Over here, on this side of the divide, there’s China and now a flood of inventory rather than money.

This is all very familiar territory, an almost exact rerun of 2018. What’s unusual or different this time around isn’t encouraging, either. |

. |

. |

|

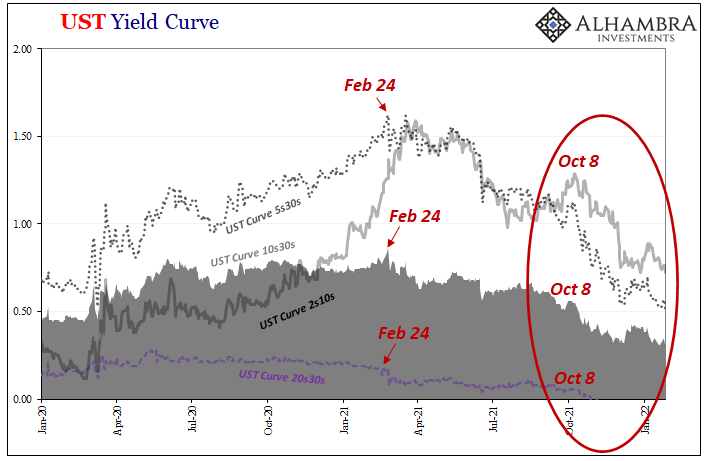

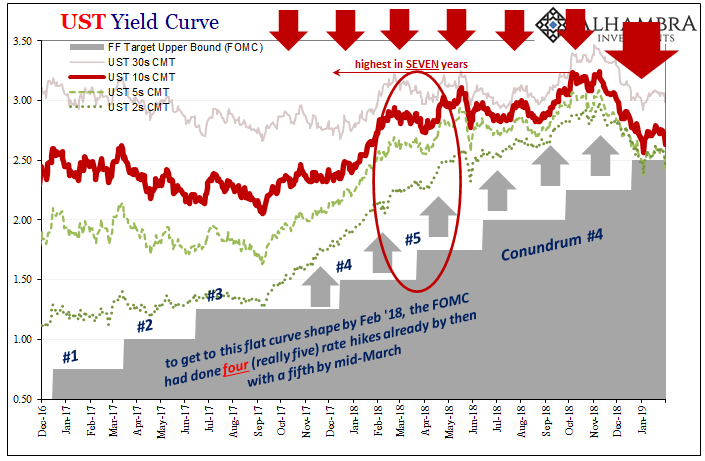

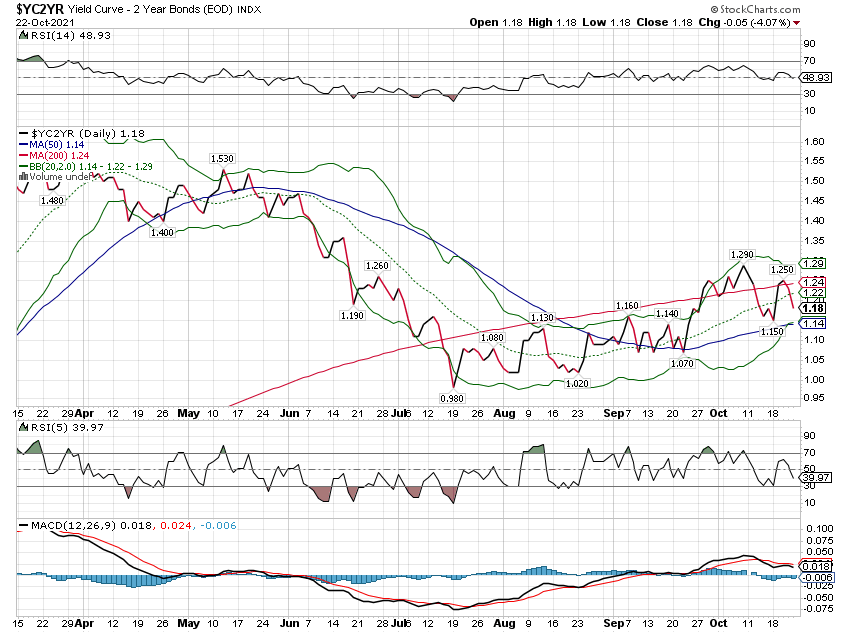

| To begin with, today with nominal rates up all across the curve on the FOMC’s announcements and projections, they were yet again higher more so in the front than the back. The crucial benchmark 10-year yield, for instance, it settled at 1.85%, up 7 bps on the day. The 5-year’s, it closed at 1.66% rising by 10 bps.

Therefore, the 5s10s calendar spread sunk by another trio of bps down to a minuscule difference of just 19 bps total. If the market was at all about to agree with the FOMC as to either growth or inflation let alone both, the long end would be rising quicker and go farther than the short end. The last time this particularly helpful part of the curve had been this flat (on the way down) it was the end of March 2018 (see: above). Same for pretty much everywhere else on the curve. The 10s30s, after the FOMC it was again at 31 bps which is the same as February 2018. Stretching out to the 5s30s, this part is now an even fifty which puts it in an equivalent shape also to March 2018. Even the wider and mainstream 2s10s flattened down to just 72 bps, same as February 2018. |

. |

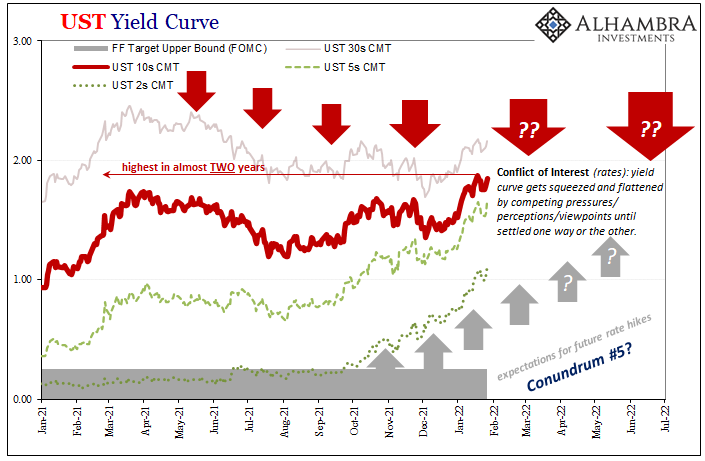

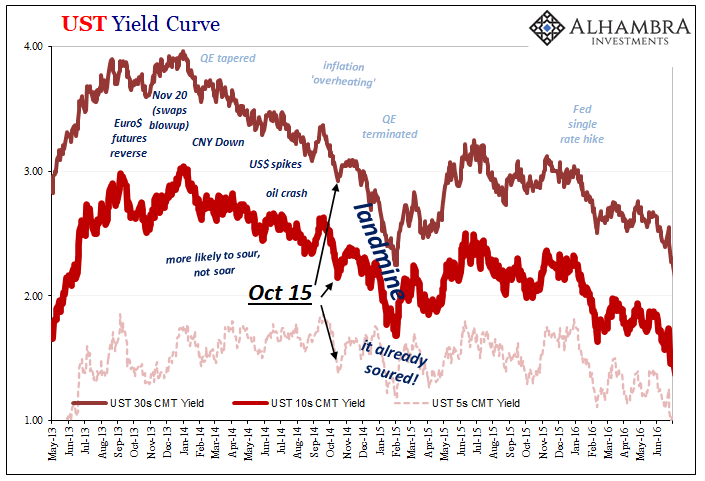

| This yield curve shape overall is priced like it is March 2018 all over again. Given how the entire world’s monetary, financial, and economic system fared from then on, this is not good sign at all.

And not just in comparison to what would happen after March 2018 but more so in the primary way in which this one is different from that one. Here’s the thing, the Federal Reserve had already raised their federal funds range four times (25 bps each) by February 2018, with a fifth undertaken right in mid-March. And I’m not even going to count the lone December 2015 hike for our purposes here, either. |

. |

| In other words, to get the yield curve as flat as it is now (where it really counts), policymakers had conducted four to five rate hikes during the last cycle (Conundrum #4). To state the obvious, the curve is in the same general shape right without yet a single one from Powell!It isn’t scheduled until the next meeting in March 2022.

What that says is as little faith as the market had in globally synchronized growth by early 2018 (remember, flattening means more likely to sour than soar; increasingly flat means far more likely to sour), it has priced materially less faith, far more determined skepticism right now even though CPI rates are (currently) the highest in four decades and everyone absolutely convinced (in mainstream commentary, anyway) this is going to continue. It is going to continue…for a little while. The curve is not predicting imminent recession, only that the balance of risks throughout the world, including the FOMC’s US base, have decidedly tilted toward the unfavorable and disinflationary. Remember, too, the eurodollar futures curve wouldn’t invert until June 2018. The market has already priced this overall adverse probability distribution even before the Fed gets started. |

. |

You Might Also Like

The Hawks Circle Here, The Doves Win There

The Hawks Circle Here, The Doves Win There

2022-01-26

We’ve been here before, near exactly here. On this side of the Pacific Ocean, in the US particularly the situation was said to be just grand. The economy was responding nicely to QE’s 3 and 4 (yes, there were four of them by that point), Federal Reserve Chairman Ben Bernanke had said in the middle of 2013 it was becoming more than enough, creating for him and the FOMC coveted breathing space so as to begin tapering both of those ongoing programs.A full and complete recovery he believed was on schedule if not getting way ahead of it.

Good Time To Go Fish(er)ing Around The Yield Curve

Good Time To Go Fish(er)ing Around The Yield Curve

2022-01-21

It should be as simple as it sounds. Lower LT UST yields, less growth and inflation. Thus, higher LT UST yields, more growth and inflation. Right? If nominal levels are all there is to it, then simplicity rules the interpretation. Visiting with George Gammon last week, he confessed to committing this sin of omission.

Conflict Of Interest (rates): 10-year Treasury Yield Highest in Almost Two Years

Conflict Of Interest (rates): 10-year Treasury Yield Highest in Almost Two Years

2022-01-12

The dollar was high and going higher. Emerging markets had been seriously complaining. In one, the top central banker for India outright warned, “dollar funding has evaporated.” The TIC data supported his view, with full-blown negative months, net selling from afar that’s historically akin to what was coming out of India and the rest of the world.

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century

One Shock Case For ‘Irrational Exuberance’ Reaching A Quarter-Century

2021-12-22

Have oil producers shot themselves in the foot, while at the same time stabbing the global economy in the back? It’d be quite a feat if it turns out to be the case, one of those historical oddities that when anyone might honestly look back on it from the future still hung in disbelief. Let’s start by reviewing just the facts.

This Is A Big One (no, it’s not clickbait)

This Is A Big One (no, it’s not clickbait)

2021-12-02

Stop me if you’ve heard this before: dollar up for reasons no one can explain; yield curve flattening dramatically resisting the BOND ROUT!!! everyone has said is inevitable; a very hawkish Fed increasingly certain about inflation risks; then, the eurodollar curve inverts which blasts Jay Powell’s dreamland in favor of the proper interpretation, deflation, of those first two.

Weekly Market Pulse: Inflation Scare!

Weekly Market Pulse: Inflation Scare!

2021-10-25

The S&P 500 and Dow Jones Industrial stock averages made new all time highs last week as bonds sold off, the 10 year Treasury note yield briefly breaking above 1.7% before a pretty good sized rally Friday brought the yield back to 1.65%. And thus we’re right back where we were at the end of March when the 10 year yield hit its high for the year.

The Curve Is Missing Something Big

The Curve Is Missing Something Big

2021-10-21

What would it look like if the Treasury market was forced into a cross between 2013 and 2018? I think it might be something like late 2021. Before getting to that, however, we have to get through the business of decoding the yield curve since Economics and the financial media have done such a thorough job of getting it entirely wrong (see: Greenspan below).

Taper *Without* Tantrum

Taper *Without* Tantrum

2021-08-17

Whomever actually coined the term “taper”, using it in the context of Federal Reserve QE for the first time, it wasn’t actually Ben Bernanke. On May 22, 2013, the central bank’s Chairman sat in front of Congressman Kevin Brady and used the phrase “step down in our pace of purchases.” No good, at least from the perspective of a media-driven need for a snappy one-word summary.

Tags: bond yields,Bonds,currencies,Deflation,economy,Featured,Federal Reserve/Monetary Policy,FOMC,inflation,Interest rates,jay powell,Markets,newsletter,rate hikes,U.S. Treasuries,Yield Curve