The unemployment rate wins again. In a saner era, back when what was called economic growth was actually economic growth, this primary labor ratio did a commendable job accurately indicating the relative conditions in the labor market. You didn’t go looking for corroboration because it was all around; harmony in numbers for a far more peaceful and serene period. Ever since the Great “Recession”, however, the unemployment rate has really struggled. Nearly the entire way during this supposedly record-length labor market win streak the measure was entirely alone in its optimism. Even the Establishment Survey took (more than) a few breaks along the way (including since mid-2018). It didn’t start out like this; the unemployment rate behaved itself during the first

Topics:

Jeffrey P. Snider considers the following as important: 5.) Alhambra Investments, currencies, economy, employment, establishment survey, Featured, Federal Reserve/Monetary Policy, GFC1, GFC2, household survey, labor force, Labor market, Markets, newsletter, payrolls, unemployment rate, workers

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

|

The unemployment rate wins again. In a saner era, back when what was called economic growth was actually economic growth, this primary labor ratio did a commendable job accurately indicating the relative conditions in the labor market. You didn’t go looking for corroboration because it was all around; harmony in numbers for a far more peaceful and serene period. Ever since the Great “Recession”, however, the unemployment rate has really struggled. Nearly the entire way during this supposedly record-length labor market win streak the measure was entirely alone in its optimism. Even the Establishment Survey took (more than) a few breaks along the way (including since mid-2018). It didn’t start out like this; the unemployment rate behaved itself during the first part of GFC1. The labor force, which is what all this fuss comes down to, performed as anyone would’ve expected for a cyclical peak. Though the economy had fallen into recession way back in December 2007, the labor force kept rising with the population level until its peak was finally reached in October 2008, almost a year into the thing. That was somewhat normal; even if you get laid off during a recession you are still part of the labor force looking for work. During 2001’s dot-com recession, for example, the labor force level wasn’t substantially changed by the contraction – only the number of American workers had shrunk. Laid off employees continued to participate by remaining in the job market. It was shaping up to be that way in 2008, too, until AIG. The big crash changed everything. From October 2008 forward an astounding number of workers stopped looking for work. Not that anyone could’ve blamed them, there weren’t any jobs being offered. But a decline of this magnitude is and was a statement from inside the labor market about perceptions of longer run prospects. |

. |

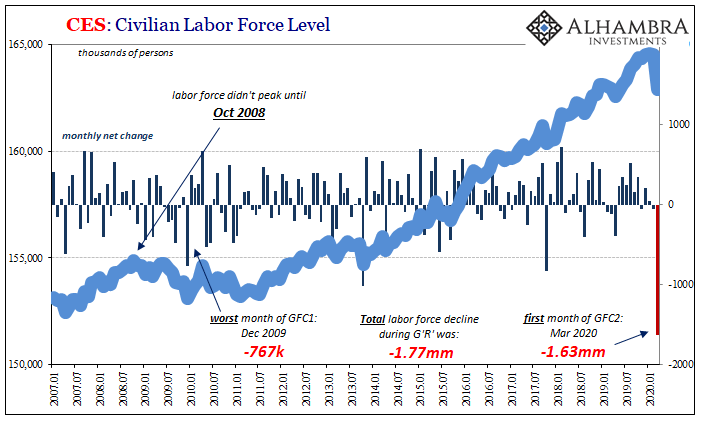

| Between October 2008 and December 2009, the US labor force actually shrank by 1.77 million.

This was the beginning of the participation problem leaving the unemployment rate unsuited to its original purpose. I don’t really know how to properly frame the latest employment data from the BLS for the month of March 2020. What the government just reported, if anywhere close to accurate, is remarkably depressing. I keep saying that the current economic data doesn’t matter; and it shouldn’t. But then these numbers show up and it’s difficult to see how what’s becoming so much greater of a downside won’t make a difference in the ability of the economy to bounce back. We all knew there’d be a deep hole to climb out of; this is a chasm approaching an abyss.More and more it is being shown how the US government, as well as those around the world, have made a grave miscalculation. The “strong” economy of Jay Powell’s dream was every administration’s insurance policy to take the most extreme coronavirus countermeasures. They’d prioritize total shutdowns on the belief the economic (and financial) system could handle them. Everyone, and I mean everyone, had listened to Economists and central bankers talk up the situation in late 2019. What recession scare, they asked by December. The economy’s in great shape moving into 2020. Nope. It wasn’t true and now we’re going to pay the price. |

CES: Civilian Labor Force Level, 2007-2020 - Click to enlarge |

| The most depressing statistic is the level of the labor force. In the first month of GFC2, not even the full thing yet, and the number of Americans reporting that they are looking for work plummeted by more than 1.6 million. That’s almost as many in a single month, just the first month, as the whole Great “Recession” start to finish.

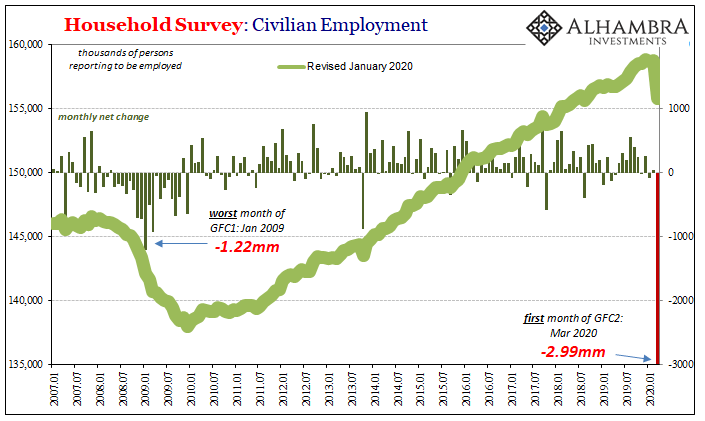

These are not layoffs or furloughs, instead potential workers who no longer see any potential. They’re out of the game entirely and it’s just the first inning. While the headline Establishment Survey finally produced a negative number, at -701k the monthly change in payrolls actually makes the economy seem strong by comparison. That comparison is the Household Survey which suggested the number of American workers reporting to be working dropped by 3 million. I’m struggling to find the words here. The payroll figure is at least comparable even if to the worst months of the Great “Recession.” The Household Survey is, well… |

Household Survey: Civilian Employment, 2007-2020 - Click to enlarge |

Therefore, while the unemployment rate rose sharply it still understates the severity of the chasm; meaning it continues to overstate resilience and strength. It went from 3.5% to 4.4%, sure, but had the labor force not collapsed the rate would’ve been 5.3% last month!

The statistic is unsuited to our era – which is now one that includes more than one GFC. Coronavirus, sure, but that’s not all to what happened in the labor market during March. As the economic (and monetary) hole gets even wider and deeper in the coming weeks (hopefully not months), it’s going to be that much harder and require that much bigger of a miracle just to get back to even again.

GFC2 will make it impossible, especially if, like GFC1, it creates the same kind of long-term damage – which is already being indicated by just the very first monthly data. No wonder 1.6 million workers bugged out of the labor force. They can see what’s ahead because, unlike Jay Powell, they probably weren’t so thoroughly fooled about where we were coming from.

You Might Also Like

Disposable (Employment) Figures

Disposable (Employment) Figures

If last month’s payroll report was declared to be strong at +128k, then what would that make this month’s +266k? Epic? Heroic? The superlatives are flying around today, as you should expect. This Payroll Friday actually fits the times. It wasn’t great, they never really are nowadays (when you adjust for population and participation), but it was a good one nonetheless.

Very Rough Shape, And That’s With The Payroll Data We Have Now

Very Rough Shape, And That’s With The Payroll Data We Have Now

The Bureau of Labor Statistics (BLS) has begun the process of updating its annual benchmarks. Actually, the process began last year and what’s happening now is that the government is releasing its findings to the public. Up first is the Household Survey, the less-watched, more volatile measure which comes at employment from the other direction. As the name implies, the BLS asks households who in them is working whereas the more closely scrutinized Establishment Survey queries establishments as to how many are on their payrolls.

Three Short Run Factors Don’t Make A Long Run Difference

Three Short Run Factors Don’t Make A Long Run Difference

There are three things the markets have going for them right now, and none of them have anything to do with the Federal Reserve. More and more conditions resemble the early thirties in that respect, meaning no respect for monetary powers. This isn’t to say we are repeating the Great Depression, only that the paths available to the system to use in order to climb out of this mess have similarly narrowed.

That’s what’s ultimately going to matter the most, not what comes next but what comes after what’s next. This is why it is paramount to pay close attention to longer term indications (and stocks are not among this group).

Those three positive factors begin with the intense buying interest in stocks including short covering. Apparently, the sharp drop on Wall Street has left many especially

It’s Not About Jobless Claims Today, It’s About What Will Hamper Job Growth In A Few Months

It’s Not About Jobless Claims Today, It’s About What Will Hamper Job Growth In A Few Months

You’ve no doubt heard about the jobless claims number. At an incomprehensible 3.28 million Americans filing for unemployment for the first time, this level far exceeded the wildest expectations as the economic costs of the shutdown continue to come in far more like the worst case. And as bad as 3mm is, the real hidden number is likely much higher.

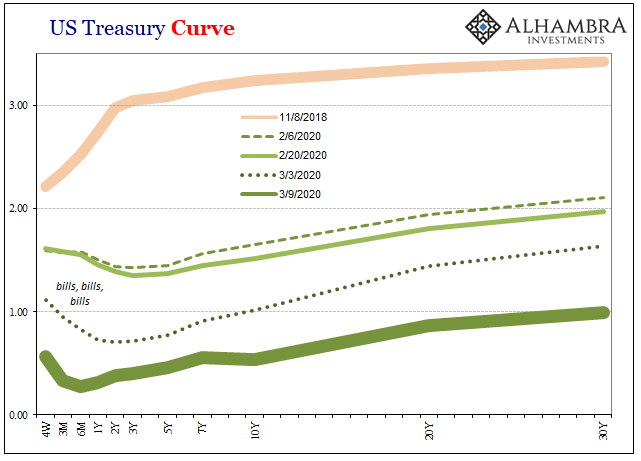

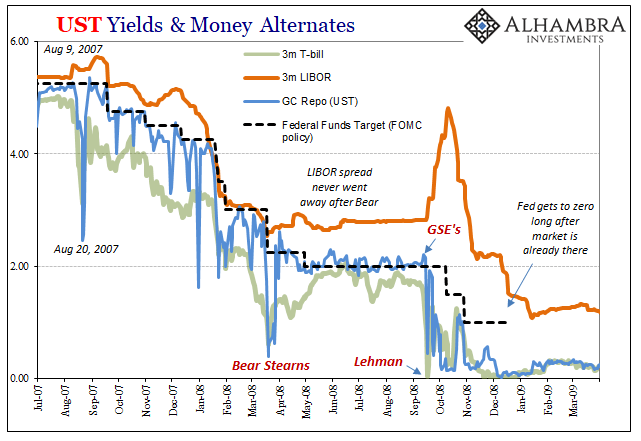

Banks Or (euro)Dollars? That Is The (only) Question

Banks Or (euro)Dollars? That Is The (only) Question

It used to be that at each quarter’s end the repo rate would rise often quite far. You may recall the end of 2018, following a wave of global liquidations and curve collapsing when the GC rate (UST) skyrocketed to 5.149%, nearly 300 bps above the RRP “floor.” Chalked up to nothing more than 2a7 or “too many” Treasuries, it was to be ignored as the Fed at that point was still forecasting inflation and rate hikes.

Like Repo, The Labor Lie

Like Repo, The Labor Lie

The Federal Reserve has been trying to propagate two big lies about the economy. Actually, it’s three but the third is really a combination of the first two. To start with, monetary authorities have been claiming that growing liquidity problems were the result of either “too many” Treasuries (haven’t heard that one in a while) or the combination of otherwise benign technical factors.

Stagnation Never Looked So Good: A Peak Ahead

Stagnation Never Looked So Good: A Peak Ahead

Forward-looking data is starting to trickle in. Germany has been a main area of interest for us right from the beginning, and by beginning I mean Euro$ #4 rather than just COVID-19. What has happened to the German economy has ended up happening everywhere else, a true bellwether especially manufacturing and industry.

China’s Back!

China’s Back!

The Washington Post began this week by noting how the US economy seems to have lost its purported zip just when it needed that vitality the most. Never missing a chance to take a partisan swipe, of course, still there’s quite a lot of truth behind the charge. An actual economic boom produces cushion, enough of one that President Trump and his administration may have been counting on it when opting for full-blown shutdown.

Tags: currencies,economy,employment,establishment survey,Featured,Federal Reserve/Monetary Policy,GFC1,GFC2,household survey,labor force,Labor Market,Markets,newsletter,payrolls,unemployment rate,workers