Swiss Economicblogs.org

Swiss Economicblogs.org

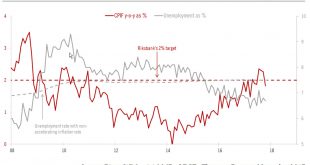

The Fed is expected to raise rates again this week. But it continues to wrestle with low core inflation, while the impact of tax cuts will need to be monitored. After the quarter-point rate rise expected on 13 December, the Federal Reserve will have pushed through the three rate hikes it signalled earlier in the year. For once, it has not under-delivered. Meanwhile, the gradual, ‘passive’ decline in the Fed’s balance sheet has been mostly ignored by...

Read More »A crucial step towards US tax cuts

Approval of the Senate tax bill paves the way for a final congressional bill that leads to tax cuts. Although unchanged, we now see some upside risks to our 2018-19 scenario for US growth and inflation. With the approval of the Senate tax bill in the early hours of Saturday 2 December, a key step has been taken toward tax cuts. The next chapter in the process is to reconcile this tax bill with the House of Representatives’ version, most likely in a...

Read More »Euro area forecast to grow 2.3% in 2018

We have upgraded our growth projection for this year and next. There are upside risks to our forecast that the ECB will start hiking rates in Q3 2019. Taking account of stronger growth momentum, the carryover effect and upward revisions to past data, we have upgraded our euro area annual GDP growth forecasts to 2.3% both in 2017 and 2018. Our forecasts remain consistent with a very gradual slowdown in the quarterly pace of GDP growth, to 2% by...

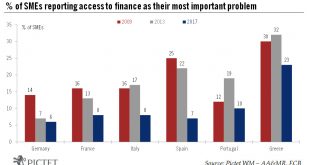

Read More »Further improvement in financial situation of euro area SMEs

The improvement and better access to credit bodes well for investment spending in the euro area as we move into 2018.Small and medium-sized entreprises (SMEs) are crucial for the euro area economy. They constitute about 99% of all euro area firms, employ around 70% of the workforce, and generate around 60% of value added. Their economic importance is above the euro area average in Italy, Spain, Portugal and Greece. Unlike large firms, which have access to alternative sources of finance, such...

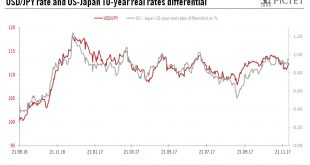

Read More »US likely to peak against yen in first half of 2018

Our 2018 scenario of a deceleration in US economic activity and a slightly less accommodative Bank of Japan should weigh on the dollar versus the yen.From 6 November to 28 November, the Japanese yen gained 2% against the US dollar, outperforming all G10 currencies but the euro.In our view, the key driver of the USD/JPY rate is the 10-year real rate differential, especially since the introduction of the yield-curve-control (YCC) framework by the Bank of Japan (BoJ) on 21 September 2016.In...

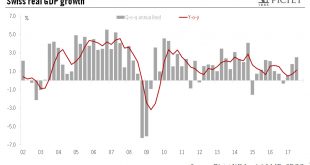

Read More »Switzerland: stronger and broader growth

After posting its fastest growth rate in almost three years in the third quarter, the Swiss economy is set to accelerate in 2018.According to the State Secretariat for Economic Affairs (SECO), Swiss real GDP expanded by 0.6% quarter-on-quarter (q-o-q) in Q3 2017, in line with consensus expectations and our own forecasts. This comes after several quarters of poor performance. As we mentioned in our previous Flash Note, the downturn in previous GDP figures was exacerbated by special...

Read More »Debt energised

The energy sector in the US climbs back onto the high-yield issuance podium.As 2017 draws to a close, it is worth taking stock of this year’s highlights. On US financial markets, this year will probably be remembered as ‘Goldilocks’ time. Financial conditions have been very accommodative. Initial fears about the impact of the Federal Reserve’s monetary tightening have faded, since the Fed has hiked rates very gradually amid modest inflation. There has been a noticeable uptick in activity on...

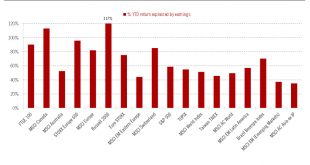

Read More »Developed-market equities continue to price hard data

Recent hard macro data confirm the resiliency of the business cycle into year end and 2018.The momentum behind hard macro data is improving investors’ visibility on corporate profit growth in developed markets (DM), which we expect to be the main market risk factor driving equity markets over 2018.According to our analysis, 96% of year-to-date returns of the Stoxx Europe 600 have been due to earnings growth and 59% of the S&P 500’s (see chart). By way of comparison, only 37% of the MSCI...

Read More »Good things come to those who wait

Scandinavian currencies have lost ground lately against the euro, but a favourable economic and policy backdrop point to strengthening of the Swedish krona.Recent months have not been kind to Scandinavian currencies: the Swedish krona and the Norwegian krone lost, respectively, 4.3% and 4.7% against the euro from the start of September to 24 November.The weakness of the Swedish krona could be explained by some disappointment at the re-election of the very dovish Stefan Ingves as Riksbank...

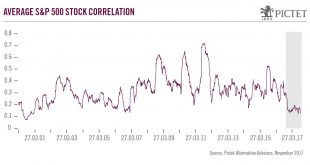

Read More »Hedge funds: alpha at the end of the QE tunnel

The performance of hedge funds has been bolstered in 2017 by the reversal of the tight market correlations of recent years. The gradual reversal of quantitative easing offers further opportunities to shine.A few years back, news that the Fed was reducing its balance sheet and considering rate rises would have prompted a severe market reaction. Today, as the ECB sets out plans for shrinking its own quantitative easing (QE) programme, the calm on financial markets is striking, affording, we...

Read More »