Thomas Costerg

June 12, 2018

Perspectives Pictet

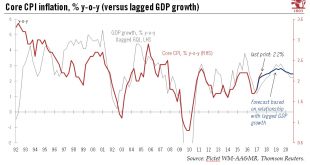

Leaving aside energy prices, there was only modest upward pressure on inflation in May.Rising energy prices continued to push up US inflation in May, but excluding this volatile category, underlying inflationary pressures remained tame, in contrast with the very solid labour market and above-potential GDP growth. This modest inflation picture is echoed by still-soft wage growth (below 3% y-o-y) and well-anchored consumer inflation expectations. In other words, there are still no signs that...

Read More »

Frederik Ducrozet

June 12, 2018

SNB & CHF

The ECB has had essentially two options going into the June meeting: either a dovish decision but a hawkish communication (hinting at an imminent QE tapering), or a hawkish decision but a dovish communication (counterb alancing a tapering announcement with dovish sweeteners).

Ever since economic indicators have started to deteriorate this year and risks to global trade have accumulated, ECB rhetoric has been...

Read More »

Thomas Costerg

June 11, 2018

Perspectives Pictet

Policy makers’ forecast for rate hikes this year likely to be raised, but central bank will be much more cautious on view further out.The Federal Reserve’s 12-13 June meeting takes place amid a strong economic backdrop at home, and the Fed is unlikely to hesitate about hiking rates by another quarter-point to a range of 1.75-2.00% this week. The US labour market is particularly solid: the unemployment rate dropped to 3.8% in May, the lowest rate since April 2000. The three-month average gain...

Read More »

Cesar Perez Ruiz

June 11, 2018

Perspectives Pictet

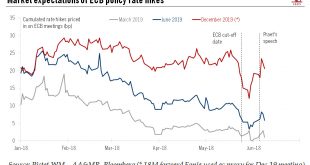

The CIO office’s view of the week ahead.The ECB’s chief economist, Peter Praet, hinted that there could be an announcement on the winding-down of the bank’s bond-buying programme this week rather than in July, as many had thought, with Praet expressing confidence that inflation would rise toward the ECB’s 2% target. Coming at a particularly sensitive time, with the euro area economy continuing to work through a prolonged soft patch and the new populist government in Italy still an unknown...

Read More »

Frederik Ducrozet

June 11, 2018

SNB & CHF

This is not what we ordered!

German factory orders collapsed in April, suggesting that the economic slowdown could extend into Q2.

The underlying pace of domestic demand expansion looks more resilient. The main downside risks relate to net exports, in our view.

Still, the most recent data releases have not been fully consistent with the ECB’s “hawkish moderation” scenario. A rebound in soft and hard data will be...

Read More »

Frederik Ducrozet

June 8, 2018

Perspectives Pictet

This is not what we ordered!German new orders were weak across the board in April, contracting for a fourth consecutive month and by a larger-than-expected 2.5% m-o-m following a downwardly-revised 1.1% drop in March. As a result, total manufacturing orders are off to an extremely weak start in Q2 (-3.3% q-o-q after -2.2% q-o-q in Q1). What is more, the decline in demand for German goods in April was fairly broad-based across countries and sectors.Beneath the surface of horrible headline...

Read More »

Frederik Ducrozet

June 8, 2018

Perspectives Pictet

An announcement on quantitative easing is looking likely as early as next week. But the jury is out on what the central bank will actually say.Peter Praet’s hawkish comments on inflation this week did not surprise us in terms of substance but did in terms of timing. The view of the (usually dovish) ECB chief economist carries significant weight, and therefore an announcement on QE is now likely at the 14 June meeting.We expect the staff projections to be revised lower in terms of GDP growth,...

Read More »

Thomas Costerg

June 7, 2018

Perspectives Pictet

While there are plenty of signs we are in the late stage of the business cycle, and while the Fed is tightening policy, we do not expect a recession in the US.The US economy is doing fine and we continue to expect solid growth in the coming quarters. The strength of corporate profits versus still-subdued unit labour costs is a sign of the robustness of the underlying US business cycle.One risk sometimes evoked is a sudden acceleration in inflation. But we forecast that core PCE inflation...

Read More »

Thomas Costerg

June 7, 2018

Perspectives Pictet

Growth in US jobs marches on: openings now exceed the numbers of unemployed.The US job market is going from strength to strength. The unemployment rate dropped to 3.8% in May, the lowest since April 2000. And another milestone has been reached as the number of job openings rose to 6.70 million in April, exceeding the number of unemployed people (6.1 million in May, 6.3 million in April)Job openings remain a good leading indicator for future US employment growth, and the ongoing momentum in...

Read More »

Jean-Pierre Durante

June 6, 2018

Perspectives Pictet

A slowdown in global business sentiment is not too worrying at this stage, but further deterioration will trigger downward revisions to GDP projections.Markit’s world manufacturing purchasing managers index (PMI) dropped from 53.5 in April to 53.1 in May. All in all, the world PMI declined in four of the first five months of 2018. No region has been spared the decline in business sentiment. Nonetheless, the index is still well above the 50 threshold that separates expansion from...

Read More »

Swiss Economicblogs.org

Swiss Economicblogs.org