Swiss Economicblogs.org

Swiss Economicblogs.org

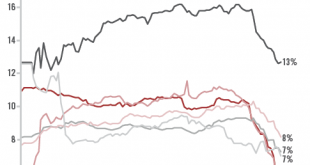

With further deterioration in the global manufacturing Purchasing Manager's Index (PMI) to 50.7 in January, the global economy is flirting with recession.January’s deterioration in sentiment was widespread, with the notable exception of the US. However, it is possible that January pessimism was largely caused by December’s poor financial markets. If this is indeed the case, it is likely that we will see a bounce in sentiment in the months ahead, following January’s rebound in markets.The...

Read More »GLOBAL INDICATORS