Swiss Economicblogs.org

Swiss Economicblogs.org

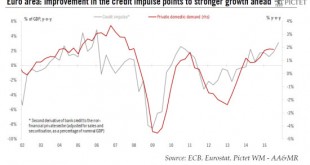

The easing package delivered by the ECB at its 3 December policy meeting fell short of market expectations. However, the new measures are still likely to boost the on-going recovery. The ECB’s President Mario Draghi was under a great deal of pressure not to disappoint today. In the end, the ECB delivered a policy package that was largely in line with our baseline, but fell short of (extremely high) expectations. However, we would not get carried away by short-term market disappointment....

Read More »European monetary policy: a mild disappointment, but the easing show is not over