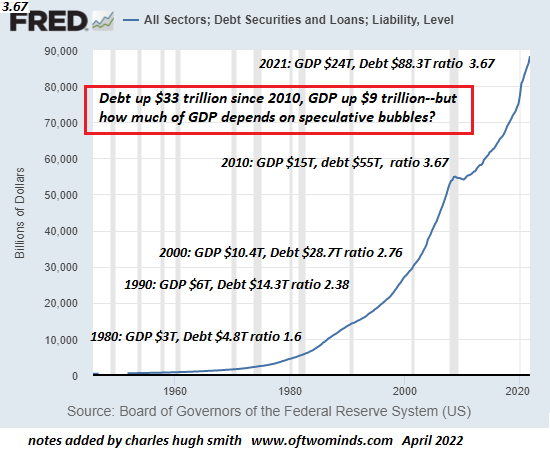

Putting this all together, it’s clear that the source of the current housing bubble is the explosion of financial speculation fueled by central bank policies. Those benefiting from speculative bubbles have powerful incentives to deny the bubble can bust.Rationalizations abound as bubbles inflate, and the continued ascent of speculative bets seems to “prove” the rationalizations are correct. But bubbles arise from speculative excesses, and once these reach extremes and reverse, bubbles burstand all the self-serving rationalizations are revealed as rationalizations. Let’s start with some caveats I’ve already covered in Is Housing a Bubble That’s About to Crash? (May 2, 2022): 1. Housing is local, so there may be locales where prices are still rising due to

Topics:

Charles Hugh Smith considers the following as important: 5.) Charles Hugh Smith, 5) Global Macro, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Putting this all together, it’s clear that the source of the current housing bubble is the explosion of financial speculation fueled by central bank policies.

Those benefiting from speculative bubbles have powerful incentives to deny the bubble can bust.Rationalizations abound as bubbles inflate, and the continued ascent of speculative bets seems to “prove” the rationalizations are correct. But bubbles arise from speculative excesses, and once these reach extremes and reverse, bubbles burstand all the self-serving rationalizations are revealed as rationalizations. Let’s start with some caveats I’ve already covered in Is Housing a Bubble That’s About to Crash? (May 2, 2022): 1. Housing is local, so there may be locales where prices are still rising due to unquenchable demand and low supply and other places where demand is low and supply ample where prices plummet. |

. |

| 2. The wealthiest 1% on a global scale is a very large number, and wealthy buyers seeking a safe haven in North America come with cash and don’t care about mortgage rates. Desirable enclaves could see home prices climb even as the national bubble pops. (World population: 7.8 billion X 1% = 78,000.000 or roughly 30,000,000 households.)

3. Wealthy investors are holding a large number of dwellings off the market as investments. These empty units consequentially reduce the supply in desirable locales, and create an artificial scarcity that would not exist if central banks hadn’t inflated the Everything Bubble. 4. The number of homes bought by corporations has soared. This has driven demand in many markets, but if rents dive due to recession, corporate buyers become corporate sellers. With those caveats out of the way, let’s look at the foundation of home ownership for the bottom 95%: income and mortgage rates. As mortgage rates rise, more income must be devoted to the monthly payment. If household income lags the increase in housing prices, price eventually exceed what the bottom 95% can afford once mortgage rates rise. |

. |

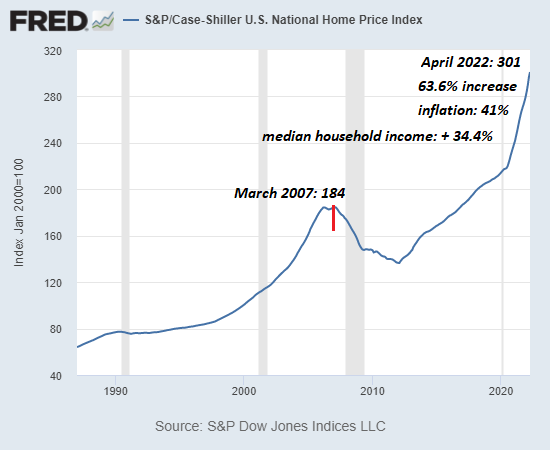

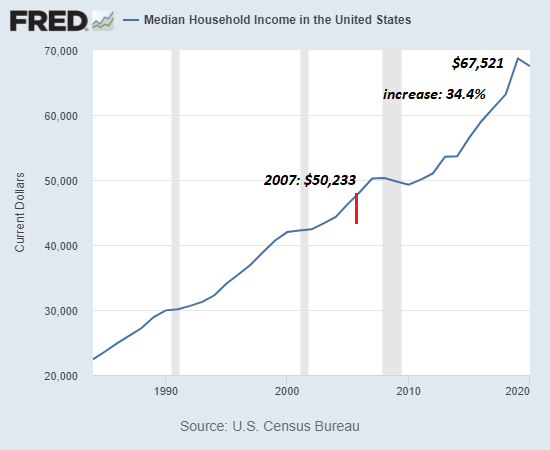

| The first chart below is the national Case-Shiller Index. Note that housing prices have soared 63.6% since the previous housing bubble peak in 2007, outpacing inflation (up 41%) and median household income (up 34%), the second chart.

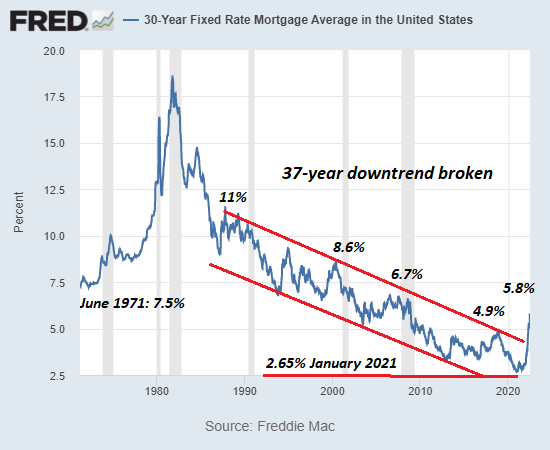

The third chart shows mortgage rates have broken out of a 37-year downtrend. It is noteworthy that mortgage rates were in the 7% to 8% range in previous economic booms (late 1960s, the 1990s) but now 6% mortgages are considered the end of the world. That suggests a dependence on cheap money / low rates is the primary support of the current bubble rather than an organic economic expansion such as we enjoyed in the 1990s. |

. |

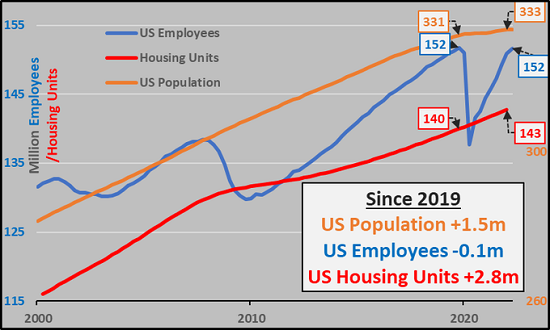

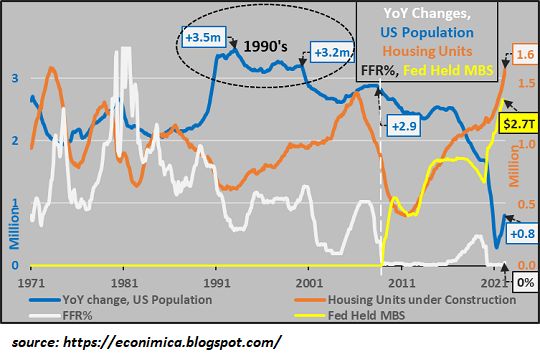

| Courtesy of my colleague CH at Econimica, the next three charts shed light on housing fundamentals. The first Econimica chart shows the rate of growth in population, employment and housing units. The U.S. population increased by a scant 1.5 million since 2019, the number of employed was flat and the number of housing units increased by 2.8 million.

The second Econimica chart shows the Fed Funds Rate (FFR), the staggering increase of mortgage-backed securities purchased by the Federal Reserve to keep mortgage rates low (from zero to $2.7 trillion), declining rate of population growth year-over-year and the remarkable rise in the number of housing units under construction. |

. |

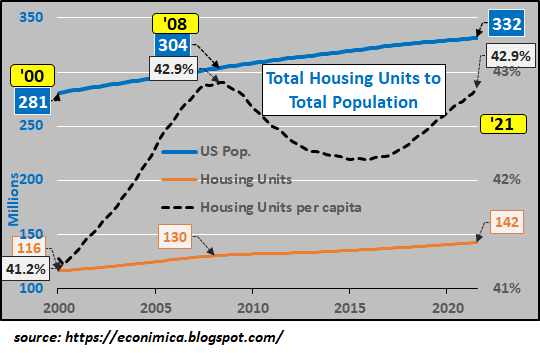

| The third Econimica chart shows housing units per capita (per person), which has reached the same level as the previous housing bubble peak in 2007-08.

As CH observed: “Housing units (per capita) against US population should suggest not a shortage of housing units but a surplus of dollars with which to buy them.” Putting this all together, it’s clear that the source of the current housing bubble is the explosion of financial speculation fueled by central bank policies. Housing prices that far exceed the growth of household incomes are not sustainable, and neither are housing prices that rose solely on the basis of unprecedentedly low mortgage rates. |

. |

| It’s also clear that those with access to the (temporary) wealth created by central banks’ trillions in new credit have poured many of these “free money” trillions into housing globally as a hedge against inflation, a safe-haven investment or for corporations, for rental income. All of these factors exacerbate an artificial demand and equally artificial scarcity.

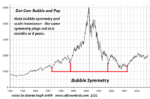

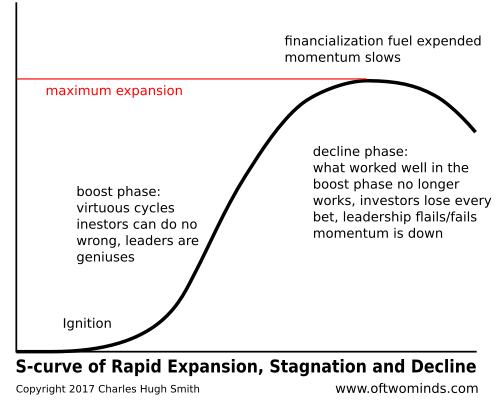

As I’ve noted in the past, bubbles typically manifest a symmetry in their ascent and decline. All the gains are eventually reversed, and if the system is destabilized by the bubble bust, then prices drop far below previous lows. Setting aside rationalizations in favor of fundamentals, the housing bubble’s bust is already baked in. Cost of Living Is Really All About Housing: Places where the rent really is too damn high. |

. |

You Might Also Like

Herd on the Street

Herd on the Street

2022-05-15

The casino has become complex and there are no easy answers or predictable paths.

The Wall Street herd had it easy from 2009 to 2021. Life was simple and life was good: markets were easy to predict.

What’s Your Plan A, B and C?

What’s Your Plan A, B and C?

2022-04-22

Nothing unravels quite as dramatically as systems which are presumed to be rock-solid and forever.

Here’s the default Bullish case for stocks and the economy: let’s call it Plan Zero.

1. The economy and equities can grow forever (a.k.a. infinite growth on a finite planet in a waste-is-growth Landfill Economy)

Debt Saturation: Off the Cliff We Go

Debt Saturation: Off the Cliff We Go

2022-04-19

When the system can’t borrow more and distribute the insolvency, it implodes. I started writing about debt saturation back in 2011. The basic idea is we can continue to borrow and spend as long as one of two conditions hold: 1) real (inflation-adjusted) income is rising, so there’s more income to service additional debt, or 2) the cost of borrowing declines so the same income can support more debt.

Calm Before the Storm?

Calm Before the Storm?

2022-03-28

Stocks don’t vanish when sold; somebody owns the shares all the way to the bottom. These owners who refuse to sell because they have convinced themselves the next dip will be the hoped-for resumption of the bullish trend are called "bagholders."

Autocracy’s Fatal Weakness

Autocracy’s Fatal Weakness

2022-03-23

This desire for compliance and consensus dooms the autocracy to failure and collapse because dissent is the essence of evolutionary churn and adaptation. The various flavors of autocracy (theocracy, kleptocracy, dictatorship, etc.) look remarkably successful at first blush but they all share a fatal flaw.

The Upside of a Crushing Recession

The Upside of a Crushing Recession

2022-03-11

Unbeknownst to those trembling in fear of a crushing recession, the crushing recession they fear is the only curative for a fatally distorted system which has lost touch with reality. Everyone looking at the inevitability of recession with alarm is forgetting the many upsides of recession, especially one that crushes all attempts to reverse it with the usual tricks.

Our Leaders Made a Pact with the Devil, and Now the Devil Wants His Due

Our Leaders Made a Pact with the Devil, and Now the Devil Wants His Due

2022-02-22

The unprecedented credit-fueled bubbles in stocks, bonds and

real estate are popping, and America’s corrupt leaders can only stammer and spew excuses and empty promises.

Unbeknownst to most people, America’s leadership made a pact with the Devil: rather than face the constraints

and injustices of our economic-financial system directly, a reckoning that would require difficult choices and

some sacrifice by the ruling financial-political elites, our leaders chose the Devil’s Pact: substitute

the creation of asset-bubble "wealth" in the hands of the few for widespread prosperity.

The Devil’s promise: that some thin trickle of the trillions of dollars bestowed on the few would magically

trickle down to the many. This was as visibly foolish as the promise of immortality on Planet Earth,

Tags: Featured,newsletter