Summary:

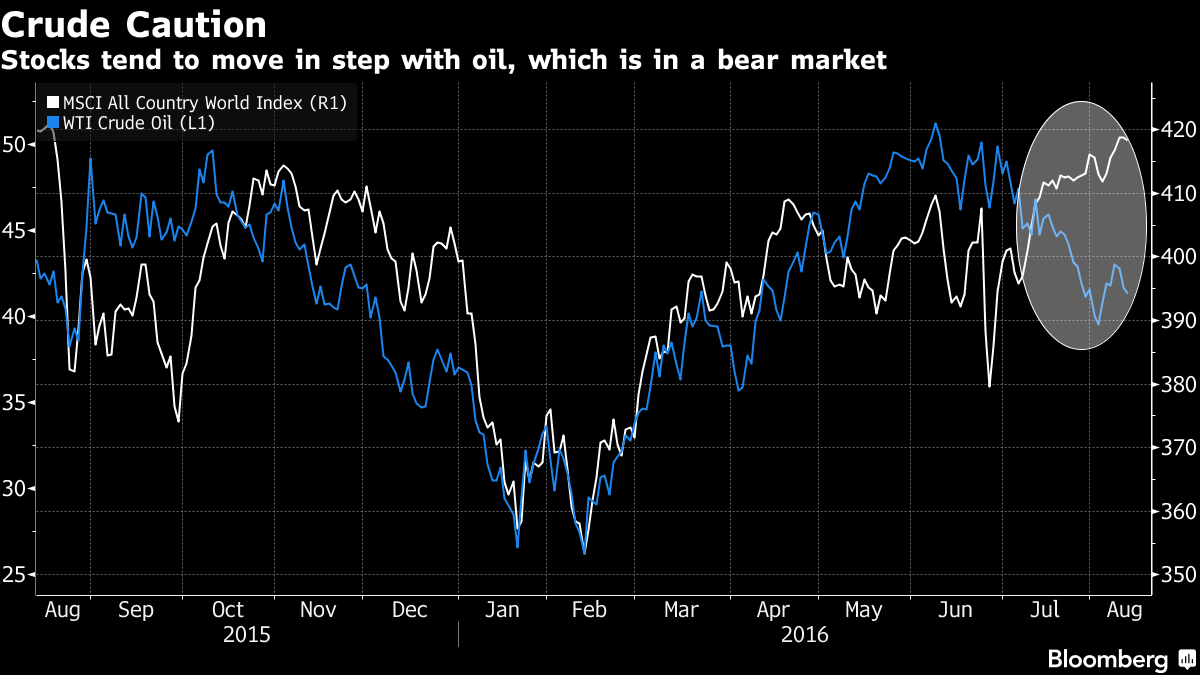

The summer doldrums continue with another listless overnight session, not helpd by Japan markets which are closed for holiday, as Asian stocks fell fractionally, while European stocks rebounded as oil trimmed losses after the the IEA said pent-up demand would absorb record crude output (something they have said every single month). S&P futures have wiped out almost all of yesterday's losses and were up over 0.2% in early trading. Europe's Stoxx 600 rose 0.4% with miners and energy producers trimming losses, as crude pared a drop of as much as 1.5 percent after the IEA forecast, Bloomberg reports. Asian equities fell. New Zealand’s dollar surged to a one-year high after the country’s central bank cut interest rates and signaled a more gradual easing path than some investors had anticipated. Nickel snapped a four-day advance. Ukraine’s 2019 Eurobond fell the most since June amid signs tension is increasing with Russia. The modest rebound in oil could not have come at a more important time, just as the black gold was sliding and set to retest the support level, below which JPM believes SWF would resume liquidation.

Topics:

Tyler Durden considers the following as important: Abenomics, Bank of England, Bear Market, BOE, Central Banks, Chrysler, CPI, Crude, Equity Markets, European Central Bank, Federal Reserve, fixed, Ford, Foreign Central Banks, France, Freddie Mac, Futures market, Gilts, Hong Kong, Housing Market, Initial Jobless Claims, International Monetary Fund, Iran, Ireland, Italy, Japan, Jim Reid, Market Conditions, Market Sentiment, Market Share, Mexico, natural gas, New Zealand, OPEC, Price Action, RANSquawk, Reality, Saudi Arabia, Shenzhen, Twitter, Unemployment, Unemployment Benefits, World Gold Council, Yen, Yuan, Zurich

This could be interesting, too:

The summer doldrums continue with another listless overnight session, not helpd by Japan markets which are closed for holiday, as Asian stocks fell fractionally, while European stocks rebounded as oil trimmed losses after the the IEA said pent-up demand would absorb record crude output (something they have said every single month). S&P futures have wiped out almost all of yesterday's losses and were up over 0.2% in early trading.

Europe's Stoxx 600 rose 0.4% with miners and energy producers trimming losses, as crude pared a drop of as much as 1.5 percent after the IEA forecast, Bloomberg reports. Asian equities fell. New Zealand’s dollar surged to a one-year high after the country’s central bank cut interest rates and signaled a more gradual easing path than some investors had anticipated. Nickel snapped a four-day advance. Ukraine’s 2019 Eurobond fell the most since June amid signs tension is increasing with Russia.

The modest rebound in oil could not have come at a more important time, just as the black gold was sliding and set to retest the $40 support level, below which JPM believes SWF would resume liquidation. Crude entered a bear market last week and the outlook remains clouded as Saudi Arabia and Iran refuse to give ground in their war for market share, with both boosting output just days after OPEC announced an informal meeting to discuss ways to stabilize falling prices. Exacerbating the problem is global demand, which remains weak even as policy makers from Frankfurt to Tokyo engage in unprecedented stimulus to boost their economies. A strengthening jobs market in the U.S. has yet to convince traders that the world’s biggest economy is strong enough for the Federal Reserve to raise interest rates this year.

"The biggest risk to the market at the moment is a huge drop in oil prices,” James Woods, strategist at Rivkin Securities in Sydney, said by phone. “Recent gains, particularly in U.S. equities, are becoming exhausted. We’ll see some near-term weakness in the coming weeks. Investors are likely to be buying on these dips as central bank policies remain supportive of equities.”

The summer doldrums continue with another listless overnight session, not helpd by Japan markets which are closed for holiday, as Asian stocks fell fractionally, while European stocks rebounded as oil trimmed losses after the the IEA said pent-up demand would absorb record crude output (something they have said every single month). S&P futures have wiped out almost all of yesterday's losses and were up over 0.2% in early trading. Europe's Stoxx 600 rose 0.4% with miners and energy producers trimming losses, as crude pared a drop of as much as 1.5 percent after the IEA forecast, Bloomberg reports. Asian equities fell. New Zealand’s dollar surged to a one-year high after the country’s central bank cut interest rates and signaled a more gradual easing path than some investors had anticipated. Nickel snapped a four-day advance. Ukraine’s 2019 Eurobond fell the most since June amid signs tension is increasing with Russia. The modest rebound in oil could not have come at a more important time, just as the black gold was sliding and set to retest the support level, below which JPM believes SWF would resume liquidation.

Topics:

Tyler Durden considers the following as important: Abenomics, Bank of England, Bear Market, BOE, Central Banks, Chrysler, CPI, Crude, Equity Markets, European Central Bank, Federal Reserve, fixed, Ford, Foreign Central Banks, France, Freddie Mac, Futures market, Gilts, Hong Kong, Housing Market, Initial Jobless Claims, International Monetary Fund, Iran, Ireland, Italy, Japan, Jim Reid, Market Conditions, Market Sentiment, Market Share, Mexico, natural gas, New Zealand, OPEC, Price Action, RANSquawk, Reality, Saudi Arabia, Shenzhen, Twitter, Unemployment, Unemployment Benefits, World Gold Council, Yen, Yuan, Zurich

This could be interesting, too:

Lance Roberts writes CAPE-5: A Different Measure Of Valuation

Lance Roberts writes CAPE-5: A Different Measure Of Valuation

Lance Roberts writes Estimates By Analysts Have Gone Parabolic

Lance Roberts writes The Impact Of Tariffs Is Not As Bearish As Predicted

In another reminder that Brexit may not be contained, a gauge of U.K. home sales pointed to the fastest decline in transactions since the global financial crisis in 2008, Royal Institution of Chartered Surveyors data showed on Thursday. As a result, sterling snapped lower and cable dropped below 1.3000, trading at 1.296 at last check. Singapore cut the top end of its 2016 growth forecast after the economy expanded less than previously estimated in the second quarter.

Asia started off on the wrong goot, with the MSCI Asia Pacific excluding Japan Index falling 0.2 percent, down from a one-year high. Australia’s S&P/ASX 200 Index dropped 0.6 percent as benchmarks lost ground in Shanghai and Taiwan. Hong Kong’s Hang Seng Index climbed 0.4%, led by financial companies, after the head of the city’s bourse operator told CNBC an exchange trading link with the Chinese city of Shenzhen will soon be announced. Hong Kong Exchanges & Clearing Ltd. jumped 2.9 percent, its biggest increase since May. The MSCI Emerging Markets Index slipped 0.1 percent after advancing five days to the highest close since July 2015. Gulf stocks declined on Thursday, with the Bloomberg GCC 200 Index losing 0.4 percent, trimming this week’s gain to 1.3 percent.

The rebound in the commodity complex translated into strength for European equities, as the Stoxx 600 rebounded from a decline of as much as 0.2%, as miners and oil companies came off session lows. Volume remains lethargic, and the number of shares changing hands was about a third less than the 30-day average according to Bloomberg. Zurich Insurance Group AG added 4.2 percent after saying earnings fell less than projected. KBC Group NV advanced 5.5 percent after posting better-than-expected profit and revenue and cutting its forecast for 2016 loan-loss provisions in Ireland. K+S AG, Europe’s biggest potash producer, plunged 9.2% after saying it expects lower earnings in 2016. Thyssenkrupp AG lost 0.7 percent after Germany’s biggest steelmaker reported a decline in quarterly profit.

S&P 500 futures rose 0.2% after the underlying equity benchmark declined 0.3 percent on Wednesday, retreating from a near-record high.

The yield on 10Y U.S. Treasuries rose two bps to 1.51%. It fell on Wednesday as 10-year notes were auctioned at the lowest yield in four years amid near-record demand from a group of buyers that includes foreign central banks and mutual funds. The U.S. is scheduled to sell $15 billion of 30-year bonds Thursday. U.K. 10-year bonds were little changed, after a three-day rally in the securities pushed yields to a record low on Wednesday. Gilts have been boosted this week on signs the Bank of England may need to pay higher prices to purchase enough to meet the target for its expanded quantitative-easing program.

Investors will look Thursday to earnings from retailers including Macy’s Inc. for indications of the health of the American consumer, as well as the latest weekly jobless claims report, where 265k Americans are expected to have filed unemployment benefits.

* * *

Markets Snapshot

In another reminder that Brexit may not be contained, a gauge of U.K. home sales pointed to the fastest decline in transactions since the global financial crisis in 2008, Royal Institution of Chartered Surveyors data showed on Thursday. As a result, sterling snapped lower and cable dropped below 1.3000, trading at 1.296 at last check. Singapore cut the top end of its 2016 growth forecast after the economy expanded less than previously estimated in the second quarter.

Asia started off on the wrong goot, with the MSCI Asia Pacific excluding Japan Index falling 0.2 percent, down from a one-year high. Australia’s S&P/ASX 200 Index dropped 0.6 percent as benchmarks lost ground in Shanghai and Taiwan. Hong Kong’s Hang Seng Index climbed 0.4%, led by financial companies, after the head of the city’s bourse operator told CNBC an exchange trading link with the Chinese city of Shenzhen will soon be announced. Hong Kong Exchanges & Clearing Ltd. jumped 2.9 percent, its biggest increase since May. The MSCI Emerging Markets Index slipped 0.1 percent after advancing five days to the highest close since July 2015. Gulf stocks declined on Thursday, with the Bloomberg GCC 200 Index losing 0.4 percent, trimming this week’s gain to 1.3 percent.

The rebound in the commodity complex translated into strength for European equities, as the Stoxx 600 rebounded from a decline of as much as 0.2%, as miners and oil companies came off session lows. Volume remains lethargic, and the number of shares changing hands was about a third less than the 30-day average according to Bloomberg. Zurich Insurance Group AG added 4.2 percent after saying earnings fell less than projected. KBC Group NV advanced 5.5 percent after posting better-than-expected profit and revenue and cutting its forecast for 2016 loan-loss provisions in Ireland. K+S AG, Europe’s biggest potash producer, plunged 9.2% after saying it expects lower earnings in 2016. Thyssenkrupp AG lost 0.7 percent after Germany’s biggest steelmaker reported a decline in quarterly profit.

S&P 500 futures rose 0.2% after the underlying equity benchmark declined 0.3 percent on Wednesday, retreating from a near-record high.

The yield on 10Y U.S. Treasuries rose two bps to 1.51%. It fell on Wednesday as 10-year notes were auctioned at the lowest yield in four years amid near-record demand from a group of buyers that includes foreign central banks and mutual funds. The U.S. is scheduled to sell $15 billion of 30-year bonds Thursday. U.K. 10-year bonds were little changed, after a three-day rally in the securities pushed yields to a record low on Wednesday. Gilts have been boosted this week on signs the Bank of England may need to pay higher prices to purchase enough to meet the target for its expanded quantitative-easing program.

Investors will look Thursday to earnings from retailers including Macy’s Inc. for indications of the health of the American consumer, as well as the latest weekly jobless claims report, where 265k Americans are expected to have filed unemployment benefits.

* * *

Markets Snapshot

- S&P 500 futures up 0.2% to 2178

- Stoxx 600 up 0.4% to 345

- FTSE 100 down 0.4% to 6841

- DAX up 0.5% to 10704

- German 10Yr yieldunchanged at -0.11%

- Italian 10Yr yield up less than 1bp to 1.08%

- Spanish 10Yr yield down less than 1bp to 0.94%

- S&P GSCI Index down less than 0.1% to 341.5

- MSCI Asia Pacific down 0.2% to 139

- Nikkei 225 closed

- Hang Seng up 0.4% to 22581

- Shanghai Composite down 0.5% to 3003

- S&P/ASX 200 down 0.6% to 5508

- US 10-yr yield up less than 1bp to 1.51%

- Dollar Index up 0.18% to 95.82

- WTI Crude futures down 0.6% to $41.47

- Brent Futures down 0.4% to $43.88

- Gold spot down less than 0.1% to $1,346

- Silver spot up 0.2% to $20.20

- Valeant Reported to Be in Criminal Probe Over Pharmacy: Prosecutors are pursuing legal theory that Valeant, its mail-order pharmacy, Philidor Rx Services LLC, allegedly defrauded insurers by hiding their close relationship, WSJ said.

- Wal-Mart Sells Mexico Clothing Chain to Liverpool for $1b: WMT’s Mexican unit agreed to sell Suburbia clothing chain to El Puerto de Liverpool in deal valued at MXN19b; WMT Said to Require Jet.com CEO to Stay for 5 Yrs: Recode

- Williams Partners Sees $820m Upfront Cash From Chesapeake Pact: Co. says deal will bring back natural gas exploration there, make money-losing wells profitable again.

- Cheap Loonie Not Helping Business Case for Canada: GM: Ford, Fiat Chrysler, GM are starting negotiations with Unifor, which represents ~23k workers those at 3 cos., against backdrop of declining production in Canada.

- Marcato Pushes Goodyear to Return $4.5b to Investors: WSJ: Activst seeking returns over next 3 years.

- Twitter Ruled Not Liable for ISIS Tweets Leading to Attack: U.S. law protects Twitter from being treated as publisher of any information provided by another content provider, federal judge in S.F. ruled.

- Alphabet GV CEO Maris to Leave Venture Capital Arm: Maris’ last day to be Friday.

- Singapore Cuts Top End of 2016 GDP Forecast on Weak Outlook: Economy grew less than previously estimated in 2Q

- New Zealand Cuts Interest Rates to Record Low; Kiwi Soars: Governor Wheeler signals at least one more rate reduction

- BOK Holds Key Rate at Record Low as It Assesses Economy: Governor Lee Ju Yeol says central bank still has policy room

- Australia Bars Power Grid Sale to Foreigners on Security Concern: State Grid Corp., CKI are vying for state distributor Ausgrid

- China Mobile Profit Beats Estimates on 4G Subscriber Gains: World’s largest phone carrier added 116m 4G accounts

- Pitfalls of Global Hunt for Yield Highlighted in Mongolia Crisis: Govt 2022 bonds fall most on record after FinMin warning

- Brexit Hits U.K. Housing as Property Sales Drop Most Since 2008: Brexit undermining near-term outlook for U.K. housing market, with both demand, sales dropping in July.

- Sports Direct Worker Exodus Adds to Woes for Founder Ashley: Turnover among Sports Direct’s salaried U.K. staff rose by more than 300bps last year to 22%.

- Symrise Profit Beats as CEO Bertram Boosts Goal for Margins: Co. reported profit that beat analysts’ estimates and said its target for profitability is now set at >20%

- French Voters’ Islamism Fears Put Hollande in Political Bind: He’s stuck between desire for tougher measures to provide security amid historic reluctance by his own party to impinge on basic democratic freedoms.

- European equities trade mostly higher, albeit modestly so with newsflow once again remaining on the light side

- The main mover in FX overnight was the NZD after the RBNZ cut rates by 25bps as expected but said there was no discussion of a 50bps cut

- Looking ahead, highlights include the weekly US jobs data

- Treasuries slightly lower in overnight trading, European equities near seven-week high (Japan closed for Mountain Day)while oil and gold move lower; auctions conclude with $15b 30Y bonds, WI 2.25%, last sold at 2.172% in July, lowest 30Y auction stop on record.

- New Zealand’s central bank cut interest rates to a fresh record low of 2% and flagged more easing to combat low inflation, disappointing some investors who were looking for a more aggressive signal. The local dollar surged

- The central bank said markets missed the downside risks to the outlook for interest rates in Thursday’s policy document and got ahead of themselves by driving the currency to a one-year high

- The European Central Bank may need to rely more on asset purchases for monetary stimulus as its negative interest rates approach the limit of their effectiveness, economists at the International Monetary Fund said

- BOE’s asset purchase plan has U.K. gilts storming down the path carved out by their Japanese peers as yield premium offered by 10-year gilts over similar-maturity Japanese bonds shrank to the lowest on record

- South Korea’s central bank held its key interest rate at a record low 1.25% as board members deferred further policy action until they have a clearer picture of the economy’s path

- Investors who piled into some of the world’s riskiest bonds to escape near-zero interest rates got a reality check on Wednesday when Mongolia sent its debt plunging by sounding the alarm on its economic crisis

- Japanese distrust of Abenomics, negative interest rates and a rising yen have all combined to boost their investment in bars and coins, the World Gold Council said in a report

- 8:30am: Import Price Index, July, est. -0.4% (prior 0.2%)

- 8:30am: Initial Jobless Claims, Aug. 6, est. 265k (prior 269k)

- 9:45am: Bloomberg Consumer Comfort, Aug. 7 (prior 43)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change