Global stocks are lower across the board to start the week, as concerns about Trump's administration to pull off a material tax reform plan finally emerge, pressuring S&P futures some 20 points lower this morning, following European and Asian shares lower, while crude oil prices fall unable to find support in this weekend's OPEC meeting in Kuwait where a committee recommended to extend oil production cuts by another 6 months. Safe havens including the yen and bonds climbed as did gold, which continued its advance above the key resistance level of ,250, while industrial commodities dropped. So-called "Trumpflation trades" - bets that Trump's pro-business policies would stoke growth and inflation in the U.S. and global economies, boosting assets such as commodities - came under heavy selling pressure. The dollar, whose index had surged more than 6 percent in the aftermath of Trump's election to hit 14-year highs at the start of 2017, slipped to its lowest since Nov. 11, two days after the results of the presidential vote. "Investors are viewing this setback as a broader loss of faith in the Trump administration’s ability to deliver on other campaign pledges - namely tax and spending policies, which have underpinned asset prices since the U.S. elections," said ING currency strategist Viraj Patel, in London. U.S.

Topics:

Tyler Durden considers the following as important: Android, ASX, ASX 200, Australia, Bain, Bank of England, Bank of Japan, Basic Resources, Bloomberg Dollar Spot, BOE, Bond, Borrowing Costs, British Pound, BSE 30, Business, Carry Trade, Case-Shiller, CDU party, Central Banks, Chicago PMI, China, Congress, Consumer Confidence, Consumer Sentiment, Copper, CPI, Crude, Crude Oil, Dallas Fed, Donald Trump, economy, Equity Markets, Euro, European Central Bank, European Union, Eurozone, Federal government, Finance, fixed, flash, Fox News, France, FT Westinghouse Chapter, Futures contract, Futures markets, Germany, goldman sachs, Hang Seng 40, headlines, Hong Kong, India, Initial Jobless Claims, Japan, Jim Reid, Kuwait, M3, Market Sentiment, Michigan, Monetary Policy, Money Supply, MSCI Asia Pacific, New Zealand, Nikkei, Nikkei 225, Obamacare, OPEC, Organization of Petroleum-Exporting Countries, Pentagon, People's Bank Of China, Personal Income, Precious Metals, Price Action, Price of oil, Pricing, Reality, recovery, Republican Party, Richmond Fed, Risk Premium, S&P, S&P 500, S&P futures, S&P/ASX 200, Saxo Bank, Scottish parliament, SMI 20, Social Democratic party, Stoxx 600, Stress Test, Topix, Trade Balance, Trump Administration, Trump's administration, U.S. Treasury, Unemployment, University Of Michigan, VIX, Volatility, West Texas, Wholesale Inventories, Yen, Zurich

This could be interesting, too:

investrends.ch writes Neuer Vertriebsleiter bei Goldman Sachs kommt von Invesco

investrends.ch writes Goldman Sachs lanciert aktiven ETF auf grüne und soziale Anleihen aus Schwellenländern

investrends.ch writes Goldman Sachs verdient mehr als erwartet

investrends.ch writes Bank J. Safra Sarasin kauft 70 Prozent der Saxo Bank

Global stocks are lower across the board to start the week, as concerns about Trump's administration to pull off a material tax reform plan finally emerge, pressuring S&P futures some 20 points lower this morning, following European and Asian shares lower, while crude oil prices fall unable to find support in this weekend's OPEC meeting in Kuwait where a committee recommended to extend oil production cuts by another 6 months. Safe havens including the yen and bonds climbed as did gold, which continued its advance above the key resistance level of $1,250, while industrial commodities dropped.

So-called "Trumpflation trades" - bets that Trump's pro-business policies would stoke growth and inflation in the U.S. and global economies, boosting assets such as commodities - came under heavy selling pressure. The dollar, whose index had surged more than 6 percent in the aftermath of Trump's election to hit 14-year highs at the start of 2017, slipped to its lowest since Nov. 11, two days after the results of the presidential vote.

"Investors are viewing this setback as a broader loss of faith in the Trump administration’s ability to deliver on other campaign pledges - namely tax and spending policies, which have underpinned asset prices since the U.S. elections," said ING currency strategist Viraj Patel, in London.

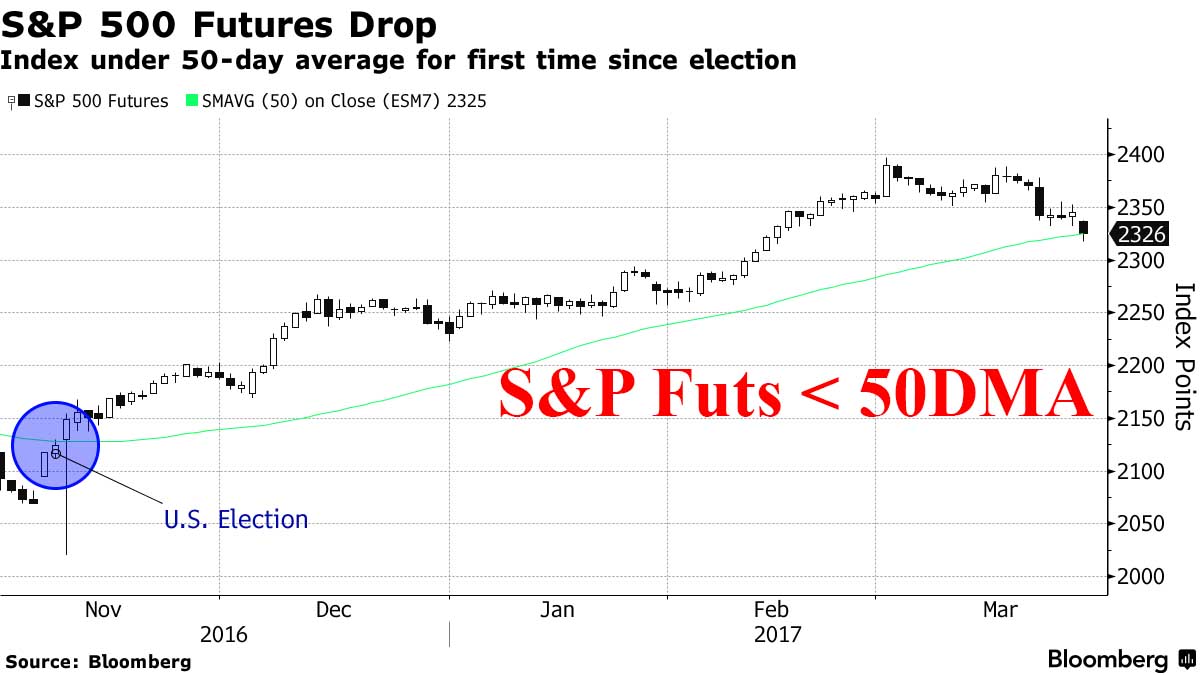

U.S. equity index futures suggested stocks would retreat for the seventh time in eight days, with S&P futures sliding below the 50 DMA for the first time since the election.

The fall in risk appetite dominated European stockmarkets, with the pan-European STOXX 600 index falling 0.8 percent on the day led by the Basic Resources index which was the biggest sectoral loser, down 2 percent to a two-week low as copper prices slipped, while the banking index was down 1.3 percent. The Euro rose to the highest level of 2017...

... on the heels of a strong German IFO Business Climate reading, which rose to 112.3, beating expectations and above the last 111 print, indicative of a 3% GDP German print.

However, a potential red flag emerged in the latest monetary aggregate data out of the Eurozone, where M3 growth dipped from 4.9% to 4.7%, below the 4.9% expected, despite the ECB continuing its monetary blast at record levels, not to mention last week's massive TLTRO.

Bucking the weaker trend among European stocks were precious metal miners such as Randgold and Fresnillo, both up more than 1 percent, as risk aversion boosted gold. Gold prices climbed more than 1 percent to a one-month high of $1,259 an ounce.

Attention today will remain fixed on Trump’s inability to push through the Republican healthcare bill through the House, which as noted last night, has derailed investor hopes that his pro-business agenda will pass smoothly through Congress. Reflation trades sparked by his election are faltering, with the dollar retreating and the S&P 500 Index headed for its worst month since October.

“Trump’s failure to get the health care bill through a Republican majority led Congress has raised some concerns about the President’s ability to implement his agenda of cutting taxes and raising infrastructure spending,” Ole Hansen, chief commodity strategist at Saxo Bank, told Bloomberg.

“Failure would deflate further the months-long rally in stocks while reducing the need for further Fed action. The result of this has seen the dollar, stocks and bond yields lower which are all good news for investors looking for gold as an alternative.”

The market reaction has been uniformly negative, with the MSCI Asia Pacific Index falling 0.3 percent, with more than three shares falling for every one advancing. Japan’s Topix led declines, dropping 1.3% to the lowest since Feb. 9 and almost wiping out gains for 2017. Chinese shares traded in Hong Kong fell 1.1% and India’s Sensex index slid 0.4 percent.

Futures on the S&P 500 lost 0.9 percent, or 20 points, to 2,324 as of 10:12 a.m. in London. The underlying gauge last week tumbled 1.4%, its worst week of 2017. The Stocks Europe 600 Index fell 0.6 percent as it was dragged down by miners and banks. In terms of relative valuations, U.S. stocks are trading well above their historical averages while Asia stocks are still broadly in line with theirs despite a recent bounce.

WTI and Brent both dropped as markets looks past producers' soft committment to extend oil production cuts. A pledge by crude producers to consider extending their output-cut deal failed to excite oil bulls, with prices dropping as more time seen needed to trim swollen global stockpiles. Five OPEC producers joined with non-member Oman to voice support for prolonging supply curbs past June, with Kuwait saying it should be for an additional six months. Committee of ministers from Kuwait, Algeria and Venezuela and their counterparts from Russia and Oman that met over the weekend asked OPEC to review the market and give them a recommendation in April on rolling over the output reductions. Russia said it needs more time before making a decision.

Oil prices rallied as OPEC, 11 other major producers including Russia agreed last year to slash production; the rally stalled this month as U.S. output, supplies have continued to grow. Libya’s biggest oil terminal was loading its first tanker since fighting earlier this month halted shipments. “There’s a lot of impatience when we continue to see builds in inventory and growing U.S. output,” Daniel Hynes, an analyst in Sydney at Australia & New Zealand Banking Group, says in a Bloomberg Television interview. “The market’s definitely asking for it,” he says, referring to a deal extension.

In rates, U.S. Treasury yields fell to a one-month low of 2.35%, while borrowing costs across the euro zone also fell sharply, as investors ditched riskier assets and unwound bets on higher inflation and interest rates.

Bulletin Headline Summary

- European equities slip after US President Trump's healthcare bill collapsed, with markets now questioning whether Trump's other proposals can come to fruition.

- USD is on the backfoot, while EUR finds support early on with a data heavy week for the Eurozone kicking off to a strong start as German IFO data beats expectations.

- Looking ahead, highlights include comments from Fed's Evans and Kaplan

Market Snapshot

- S&P 500 futures down 0.8% to 2,325.00

- MXAP down 0.3% to 147.70

- MXAPJ down 0.1% to 478.21

- Nikkei down 1.4% to 18,985.59

- Topix down 1.3% to 1,524.39

- Hang Seng Index down 0.7% to 24,193.70

- Shanghai Composite down 0.08% to 3,266.96

- Sensex down 0.5% to 29,284.04

- Australia S&P/ASX 200 down 0.1% to 5,746.70

- Kospi down 0.6% to 2,155.66

- STOXX Europe 600 down 0.7% to 374.02

- German 10Y yield fell 2.5 bps to 0.378%

- Euro up 0.6% to 1.0865 per US$

- Brent Futures down 0.7% to $50.47/bbl

- Italian 10Y yield fell 4.8 bps to 2.224%

- Spanish 10Y yield rose 0.4 bps to 1.697%

- Brent Futures down 0.7% to $50.47/bbl

- Gold spot up 1.1% to $1,257.71

- U.S. Dollar Index down 0.5% to 99.13

Top Overnight News

- German Business Confidence Increases to Strongest Since 2011

- Trump Policy Travails Could Boost the Appeal of Asia’s Markets

- Lockheed’s $29 Billion Copter Poised to Win Pentagon’s Approval

- Apicorp in JV With Goldman Sachs for Energy Investments

- Goldman Sachs Said to Be in Talks for Saudi Equities License

- China Southern Says in Strategic Talks With American Airlines

- MoneyGram Enters Confidentiality Pact With Euronet Worldwide

- Fitbit Moves Toward Trial in Jawbone Trade Secrets Theft Case

- Coca-Cola to Add Fruit Juice to Fanta, Sprite in India: Standard

- Google Plans to Start Android Pay in S. Korea in May: ETNews

- Google Faces Demands for Ad Discounts After YouTube: FT

- Westinghouse Chapter 11 Filing May Come March 28: Nikkei

Asia equity markets traded mostly lower as the region digested the cancellation of the American Health Care Act vote on Friday due to insufficient support and the implications on the Trump reflation trade. This pressured US equity futures and Asia-Pac indices alike, with ASX 200 (-0.1%) also weighed by mining names after iron ore prices extended on last week over 7% declines. Nikkei 225 (-1.4%) underperformed on a firmer currency, while Shanghai Comp. (-0.1%) and Hang Seng (-0.7%) were choppy for much of the session as downside had been initially counterbalanced by several upbeat earnings and a 31.5% increase in Chinese Industrial Profits. 10yr JGBs traded higher as the cautious risk tone spurred safe-havens flows. However, upside was limited after the BoJ Summary of Opinions provided no surprises and the central bank also refrained from a Rinban announcement.

Top Asian News

- Bonds Surge in India as Rupee Rally Spurs Bets of More Inflows

- China Said to Approve Carbon Quota Plans for National Market

- PBOC’s Zhou Signals Financial Opening Will Require Negotiation

- Don’t Fear This Selloff Is Investors’ Bold Call: Markets Live

- Skylark’s Largest Shareholder Bain to Sell Part of Its Stake

- Zhou Signals China Financial Opening Will Need Negotiation

- Korean Prosecutors Seek to Arrest Park on Graft Allegations

- Noble Group’s Elman Mixes Mea Culpa and Optimism Before Exit

- Hong Kong Stocks Decline as Developers Drop Amid Curb Concerns

European equities slip after US President Trump's healthcare bill collapsed, with markets now questioning whether Trump's other proposals can come to fruition. As such, there has been a notable broad based sell off as the negative sentiment spares no sector with very few stocks trading in positive territory include precious metal miners, which are being supported by their link with higher gold prices, while financials are providing the biggest drag to EU bourses. In terms of equity specific newsflow, Zurich underperforms in the SMI amid reports that the insurance firm is seeking raise EUR 8.6bIn via a capital increase. Fixed income markets have benefited from the risk averse tone, although the price action among spreads have been somewhat modest. Of note, as we approach the quarter-end, there has been notable corporate issuance.

Top European News

- Oil Producers Consider Extending Output Cuts as Support Grows

- London Mansion Owners Turn to Airbnb as Buyers Turn Up Noses

- BOE Cites Brexit Among Financial Stability Risks for U.K.

- Cecabank Hires BBVA’s Head of Cash Equity Execution for New Unit

- Minsheng Investment Targets Elderly Care Groups Across Globe

In currencies, the Bloomberg Dollar Spot Index fell 0.5 percent. The yen rose 0.9 percent to 110.32 per dollar. The euro gained 0.5 percent to $1.0857 and the British pound added 0.8 percent. There is only one overriding theme the FX markets are trading off, and that is the failure of the Trump administration securing a vote to repeal Obamacare, abandoning proceedings late Friday. The initial response was to be ignored given liquidity issues, but this morning, traders have been left in no doubt as to where market sentiment lies. US Treasuries have been bid up as fiscal stimulus plans in the US have clearly suffered a blow, and watching the cash open on Wall Street, the latest sell off in risk/carry trade does not bode well. USD/JPY is an obvious casualty, but demand still reported ahead of 110.00, and given rate differentials, does not look out of place. EUR/USD has moved higher accordingly, pushing through 1.0850, but as noted, strong resistance levels of note at 1.0900 and 1.0950. Improving economic data in the EU has been a firm driver of trade, with last week's healthy PM! stats across the region backed up by a better than expected German Ifo survey today. Merkel's win in Saarland also supportive.

No jitters over Wednesday's scheduled activation of Article 50 as the Pound remains on the front foot. Cable has tested up to 1.2580 today, supported by the USD backdrop, but EUR/GBP also edging back under 0.8650 to put in a strong showing this morning.

In commodities, gold rose 1.1 percent to $1,257.28, heading for the highest close since Nov. 10. West Texas Intermediate oil slipped 0.7 percent to $47.62 a barrel, erasing an earlier gain of as much as 0.7 percent. Crude producers pledged to consider extending their pact limiting supply. Iron ore futures slid 3.9 percent, after briefly erasing gains for the year. The commodity surged in the opening weeks of 2017 following a surprise rally last year amid optimism about the demand outlook in China. Copper fell 1.3 percent and tin dropped 2 percent. A mixed bag of drivers in the commodity markets at the moment, but a clear move in precious metals in response to the USD drop as a result of the failure to secure a positive health care vote for the Trump administration. US Treasuries have garnered a bid and this has sent Gold cleanly through USD1250.00, trading a little shy of USD1260.00. Sliver still unable to regain USD18.00 however. Base metals largely in the red, but platinum and palladium getting real money demand out of the European car-makers. Copper has dipped below USD2.60, with a (temporary) resumption in the Escondida mine having a modest positive impact. Iron ore prices in China are taking a hit as reports of China stockpiles at the major ports unsettle the supply/demand balance — demand still relatively steady though. Oil prices continue to look on the heavy side, as any recovery now looks to rest on whether OPEC/non OPEC decide to extend the production cut agreement. Some argue that the existing output adjustments have not fed through to inventory levels.

We kick off things this morning in Europe with Germany where the March IFO printed at 112.3, beating expectations and rising from February's 111. The latest M3 money supply reading for the Euro area was released, and disappointed when it dipped from 4.9% to 4.7%, missing expectations. Over in the US the sole release is the Dallas Fed’s manufacturing survey for March. The Fed's Evans and Kaplan speak later in the day.

US Event Calendar

- 10:30am: Dallas Fed Manf. Activity, est. 22, prior 24.5

- 1:15pm: Fed’s Evans Speaks on Economy and Policy in Madrid

- 6:30pm: Fed’s Kaplan Speaks in College Station, Texas

* * *

DB's Jim Reid concludes the overnight wrap

It'll be interesting to know what words Mr Trump spoke on Friday night after the healthcare bill vote was abandoned. Even though defeat is not encouraging for markets there's an element of "healthcare reform is dead, long live tax reform". I write this this morning fairly confused as to how to think about markets in the near term though. The best way to benchmark my thoughts is perhaps to look back at what we expected for 2017 at the end of last year and work out what's occurred relative to expectations and whether anything has changed. The view then was that ultimately central banks pulling back from extreme policy was good for animal spirits and also that Trump was ultimately good for growth. We also thought Europe would have lots of political near misses without a fatal blow.

A combination of these near misses and the fact that there was plenty of opportunity to doubt the ability of Trump to be radical growth wise meant we thought we'd have plenty of pockets of volatility without it changing the end result of the year. So as we approach the end of the first quarter where do we stand. Well the aborted health care bill is such an example of doubting Trump's legislative abilities. However so far all it's done is cause a -1.44% sell off in the S&P 500 last week (only the second down week in nine and the worst week since November last year) and a spike intraday on Friday of the VIX to 14.16 and briefly to the highest point of the year. It's still very low historically though so as yet there is no major damage done. This morning S&P futures are -0.50% and as we'll see below sentiment has been a bit softer in Asia.

Although the healthcare bill was always going to be a huge test of the new administration's ability to peruse aggressive legislation Mr Trump has so far refrained from being too confrontational in defeat and there seems to be a desire to 'learn' from any mistakes and move on to tax. However he did blame the Freedom Caucus in a tweet yesterday and before that cryptically tweeted that his followers should watch Jeanine Pirro on Fox News on Saturday. On the show she called for Paul Ryan to step down. So this is perhaps some sign of tension and frustration without things blowing up directly.

Friday's failure does now increase the risks of further difficult negotiations going forward which Ryan hinted at on Friday night but the reality is that tax reform is of far more economic consequence than healthcare so the market could give the GOP some benefit of the doubt. Event risk should be higher now though and volatility should be higher. However while global growth numbers continue to be decent then the risk premium increases will be probably be more muted than we thought they might be when we published our 2017 outlook. Although we thought growth would hold up in 2017 it's probably surprised on the upside relative to our expectations.

So net net it leaves us with similar views to the outlook. A decent year for risk but with the technicals slightly negative for credit and thus encouraging mildly wider spreads. We think Euro IG will outperform HY from this starting point and we expect higher yields. However perhaps the vol we were expecting won't be quite as large even if we think it's still coming.

Moving on to the immediate future, this week will see the UK activate article 50 on Wednesday with the Scottish Parliament debating the proposed second independence referendum tomorrow. So watch out for plenty of headlines on these topics. I can't help but think that PM May will have something up her sleeve for announcement day. What I'm not too sure.

While on the topic of politics, Mrs Merkel got an unexpected boost yesterday following a relatively comfortable victory in the state election in Saarland. Merkel’s CDU party secured 40.7% of the vote which is up from 35.2% in the 2012 election. The Social Democratic Party, led by new leader Martin Schulz, took home 29.6% which is down from 30.4% five years ago. The anti-immigration Alternative for Germany secured 6.2% of votes. While Saarland is small with just 1 million people, the strong result for Merkel comes following rising support for the SPD following the announcement of Schulz as the leader of the party. Indeed the last 2 opinion polls (Emnid and Infratest dimap) show that support between the two parties at a national level is tied. This compares to the start of the year when the CDU held a double digit lead over the SPD across the vast majority of pollsters. So it’s worth seeing if this result is reflected in the next round of polls. Two more regional elections are due to be held in May (Schleswig-Holstein and Northrhine Westpahlia) before the national election in September.

Over in markets this morning there is definitely a slightly more negative tone sweeping through Asia to start the week. That is being reflected in the bid for safe havens with the Yen (+0.89%), Gold (+1.07%) and Treasuries (10y -4.8bps) all stronger. In equities the rally for the Yen isn’t helping the Nikkei (-1.51%) while the ASX (-0.25%) and Kospi (-0.57%) are also in the red. The Hang Seng and Shanghai Comp are little changed however.

Staying in Asia for a second, another interesting story from the weekend comes from China where, in a bid to clamp down on further capital flows out of China, banks are asking property agents in Hong Kong not to accept mainland China issued UnionPay cards for home purchases. This follows similar curbs on high priced insurance products and speculative offshore corporate acquisitions.

Moving on and quickly recapping Friday’s session. Despite the abandoned healthcare vote coming to a head late in the day the S&P 500 did only finish down a fairly paltry -0.08% and with that in fact had its second best day in the last seven sessions. That said there’s plenty asking the question about whether or not we’re starting to see the unwind of Trump trades and while the headline moves haven’t been particularly eye catching, there is some evidence of it coming through at a domestic and stock specific level. The biggest loser on Friday in the S&P was a company which supplies gravel for roads - Martin Marietta Materials which tumbled -2.93% - which perhaps reflects some fading hopes in the infrastructure trade. Meanwhile, while the move lower in rates has also clearly had a big impact US Banks declined -4.81% last week and are off nearly 8% from the March highs. Small caps – a decent barometer of domestic performance – also tumbled -2.65% last week and fell for the fourth week in five. So perhaps some evidence of pockets of weakness but the overall magnitude of the selloff has still been fairly muted in the grand scheme of things.

At the other end of the risk spectrum Gold, which did actually edge down -0.13% on Friday, rallied +1.16% last week and is now back into positive territory month to date. In rates Treasuries didn’t move much on Friday but the 10y yield still finished down 8.8bps last week and is now down around 22bps from the intraday highs just two weeks ago. Finally the US Dollar, measured by the Dollar index, fell -0.67% last week and is now down -2.68% from the early month highs.

Closer to home on Friday it was economic data rather than politics which stole the spotlight in Europe. Indeed it was the release of the flash March PMI’s which were the focus with the big news being a further improvement in the Euro area composite PMI this month to 56.7 (vs. 55.8 expected) – a rise of 0.7pts from February. With that the reading notched up a second consecutive cyclical high and encouragingly the growth appeared to be broad-based with both the services (+1pt to 56.5) and manufacturing (+0.8pts to 56.2) PMI’s rising. Regionally both France (+1.7pts to 57.6) and Germany (+0.9pts to 57.0) led the way for the acceleration with the data suggesting a marginal decline (-0.2pts) on average for the composite of the non-core. All in all our economists in Europe highlight that they see a more significant risk from the positive PMIs relative to their view as being for Q2. At its latest level, the euro area composite PMI is in line with the economy growing at between 0.7% and 0.8% qoq. Our economists’ moderate Q2 growth view (0.3%) is predicated on some slowdown in activity due to the political calendar. However, surveys have shown no sign of this having an effect thus far. With less reason to expect temporary effects to weigh on activity as in Q1 (e.g. the very cold January), they see the PMIs as presenting a clearer upside risk to their Q2 view than for Q1.

Wrapping up the remaining data on Friday, in the US headline durable goods orders rose a slightly better than expected +1.7% mom in February (vs. +1.4% expected) however largely as a result of a surge in aircraft orders. Indeed core capex orders were -0.1% mom (vs. +0.5% expected). Meanwhile the flash March composite PMI in the US declined 0.9pts to 53.2 and a six month low with both the manufacturing (-0.8pts to 53.4) and services (-0.9pts to 52.9) readings lower.

To this week’s calendar now. We’re kicking off things this morning in Europe with Germany where the March IFO survey is due out. The latest M3 money supply reading for the Euro area is also due this morning. Over in the US this afternoon the sole release is the Dallas Fed’s manufacturing survey for March. With little to highlight in Europe tomorrow, the focus will be on the US where we get the advance goods trade balance for February, wholesale inventories for February, consumer confidence for March, S&P/Case-Shiller house price index for January and Richmond Fed manufacturing survey for March are due. Wednesday kicks off in Japan where retail sales and small business confidence data is due. Over in Europe the focus will be on the UK with the February money and credit aggregates data. In the US on Wednesday the only data due out is pending home sales. Turning to Thursday, during the European session the most notable data is due out of Germany where the first estimate of CPI in March is due. Also due out are various March confidence indicators for the Euro area. In the US on Thursday the early data is the third estimate of Q4 GDP and Core PCE, while initial jobless claims data is also due. The busiest day looks set to be reserved for Friday. In Japan we will get February CPI, industrial production and employment data, while in China the official manufacturing and non-manufacturing PMI’s for March are due. In Europe we’ll get CPI reports for France and the Euro area along with Q4 GDP in the UK and unemployment in Germany. In the US data due includes February personal income and spending reports, PCE core and deflator readings, the Chicago PMI for March and the final University of Michigan consumer sentiment reading revision.

Away from the data the Fedspeak diary this week is packed. Today we see Evans and Kaplan speak, tomorrow we have George, Kaplan and Powell speaking along with Fed Chair Yellen (albeit at a conference which doesn’t suggest a focus on the economy or monetary policy), Wednesday see’s Evans, Rosengren and Williams speak, Thursday has Mester, Williams and Kaplan scheduled and Friday finishes with Kashkari. Away from that other important events this week include the BoE bank stress test scenarios today, a Scottish Parliament debate on a possible independence vote tomorrow and of course UK PM Theresa May officially triggering Article 50 on Wednesday.