Our earlier articles on bitcoin discuss the crypto asset as a currency and a commodity. Both papers focused on the consequences of bitcoin’s defining feature: the asymptotic supply limit of 21 million coins. This gives it an unusual juxtaposition of demand uncertainty and supply certainty (as well as inelasticity). As a currency, it gives rise to a tension between its use as a store of value and as medium of exchange. Like commodities, it has a mining cost of production that both influences and is influenced by price. Finally, we explored bitcoin’s demand dynamics and the problems posed by rising transaction costs and their potential to trigger price crashes. This paper explores bitcoin as an equity, and more

Topics:

Erik Norland considers the following as important: Alan Greenspan, Alternative currencies, Bitcoin, Blockchain technology, Blockchains, Business, Central Banks, Crude, Crude Oil, Cryptocurrencies, currency, Decentralization, Digital currency, Economics of bitcoin, faster computing technology, Featured, Federal government, Finance, Ford, Futures market, Global Economy, Gold and Bitcoin, Housing Bubble, integrated circuit, Legality of bitcoin by country or territory, Meltdown, Monetary Policy, Money, NASDAQ, Nasdaq 100, natural gas, New Zealand, newsletter, Recession, Swiss Franc, Volatility, Yen

This could be interesting, too:

investrends.ch writes Bitcoin nach Kurseinbruch mit fulminantem Comeback

investrends.ch writes Ford und Renault bauen gemeinsam günstige E-Autos für Europa

investrends.ch writes Welche Rolle spielen gehebelte Produkte beim jüngsten Einbruch der Krypto-Währungen?

investrends.ch writes «Die Nerven liegen derzeit blank»

Our earlier articles on bitcoin discuss the crypto asset as a currency and a commodity. Both papers focused on the consequences of bitcoin’s defining feature: the asymptotic supply limit of 21 million coins. This gives it an unusual juxtaposition of demand uncertainty and supply certainty (as well as inelasticity). As a currency, it gives rise to a tension between its use as a store of value and as medium of exchange. Like commodities, it has a mining cost of production that both influences and is influenced by price. Finally, we explored bitcoin’s demand dynamics and the problems posed by rising transaction costs and their potential to trigger price crashes. This paper explores bitcoin as an equity, and more specifically as the first equity ever launched by a non-hierarchical “teal” organization, a self-driving entity with an independent force and purpose, its role in promoting blockchain and the potential consequences of bitcoin and blockchain for the economy.

While bitcoin is most commonly described as a currency, one can argue that it also has equity-like characteristics. These arguments can be both narrow and legal in nature as well as deeper and more philosophical. From a legal perspective, many governments are moving to regulate initial coin offerings (ICOs) of cryptocurrencies as they do initial public offerings (IPOs) of equity and other securities. Bitcoin’s ICO occurred in 2009 and at the time was largely overlooked by regulators. No longer. With over 1,000 additional cryptocurrencies being launched during the past two years, regulators worldwide are playing catch up, considering their response to this occurrence.

On an economic and financial level, bitcoin also exhibits equity-like characteristics. The rewards that miners and those validating transactions on the bitcoin blockchain receive are analogous to stock grants made to employees by corporations. The stock of a company can be seen as an internal currency used to compensate and motivate employees, aligning their interests with those of the organization. To that end, the number of bitcoins in existence is comparable to the “float” of a corporation – the number of shares issued to the public.

When bitcoin forks into a new currency, such as bitcoin cash, the move is comparable to a corporate action such as a spin out. In a spin out, a corporation can give each of its shareholders new shares in a division of the firm that is being released to the public as separate and independent entity. In September 1996, for example, shareholders of the communications giant AT&T found themselves owning two stocks: that of AT&T services business, and that of Lucent Technologies, a phone equipment maker, of which AT&T (wisely) divested itself. Likewise, when bitcoin most recently forked, the owner of each bitcoin received one bitcoin cash, a new and separate cryptocurrency.

While bitcoin is not by any means a traditional corporate entity with earning statements and a board of directors, it could be seen as an equity in its own ecosystem whose value derives from the size and health of that community. What is clear is that if bitcoin is equity, it represents a radically different corporate form than has ever created before.

| It appears to be one of the first examples of what sociologist and organizational development specialist Frederic Laloux describes as a “teal organization”: an organization with fluid hierarchy that is adaptive and rules-based where authority is decentralized and distributed among members. That such an organizational form would arise around a distributed ledger is perhaps not surprising but it does, nevertheless, represent a radical new experiment in human organization. In his book, Reinventing Organizations, Laloux describes five organizational types: red, amber, orange, green and teal (Figure 1). Red organizations are primitive tribal groups led by a single person. Street gangs and the mafia are modern examples. By their nature they are unstable: when the leader dies or becomes impaired, there is a fight for control and the organization can disappear or split if a new leader does not emerge. See Francis Ford Coppola’s “The Godfather” series for details. |

Organizational Theorist Frederic Laloux’s Five Kinds of Human Organizations - Click to enlarge |

Amber organizations, the world’s first and oldest bureaucratic form, represent a radical innovation: an immutable organizational command-and-control hierarchy that survives and outlasts any member. Organized religion, government bureaucracies and militaries are examples of amber organizations.

Most corporations are either orange or green organizations. Compared to amber organizations, orange ones feature additional agility. While they maintain strict hierarchies, they form more ad hoc project groups, have greater differentiation in expertise, and change the size, scope and form of their hierarchies in conjunction with needs. They can also merge and split apart peaceably. Green organizations take this approach further, often decentralizing decision-making to frontline employees. They tend to be somewhat flatter and management is meant to enable the success of frontline employees in a partial reversal of (or at least a more two-way version of) the usual top-down reporting lines.

Until the creation of bitcoin, teal organizations were mostly theoretical, although Wikipedia could be considered an example. What Wikipedia and bitcoin have in common is that both are essentially non-hierarchical organizations in which users make voluntary contributions to the development of the entity. For Wikipedia, this comes in the form of writing and editing articles on millions of subjects in dozens of languages in accordance with the rules of the organization. For bitcoin, the voluntary contributions come in the form of mining bitcoin and validating transactions. What differentiates bitcoin from Wikipedia is that the latter is a not-for-profit organization that requires periodic, voluntary monetary contributions from supporters. Bitcoin, by contrast, rewards contributors economically in a manner somewhat analogous to orange or green corporations but with much stricter, and less political, rules for who gets paid what and why. Little wonder that bitcoin and its crypto peers are described as “the internet of money.”

Bitcoin’s limit on supply to 21 million coins is also open to a useful equity analogy. This limit on the number of coins is one of the reasons why we think that bitcoin is useless as a medium of exchange and is being treated, rightly or wrongly, as a highly volatile store of value, sort of like gold on steroids. Bitcoin could become a more useful medium of exchange if it increased the cap on the total number of coins. So, why doesn’t it? Corporations have the option of issuing more shares. For example, in the early days of the Great Recession, many banks issued more shares to recapitalize themselves. The problem with issuing more shares is that it dilutes the value of the existing equity holders and usually lowers the price of a stock. As such, aside from compensating themselves and some of the employees with share options and share grants, corporate managements avoid issuing more shares like the plague. And normally, equity holders want such share grants to be limited so as not to be excessively dilutive.

We don’t know if the bitcoin user community will one day allow for the creation of more than 21 million bitcoins. If they do, it would improve the value of bitcoin as a medium of exchange but it would likely come at the expense of bitcoin holders’ value. As such, we are not sure why existing bitcoin holders would agree to such a change. Nor is it clear why the miners and transaction validators would agree to such a change, which would likely lower their profit margins.

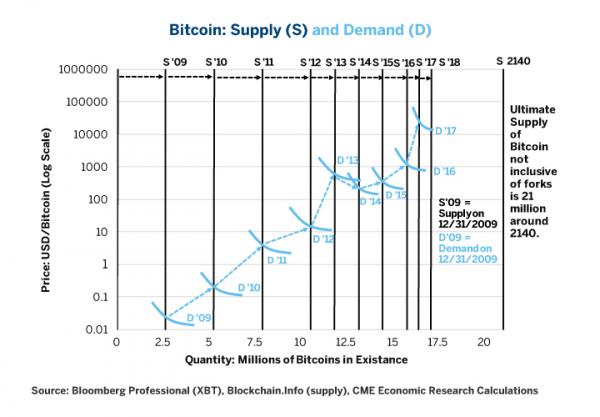

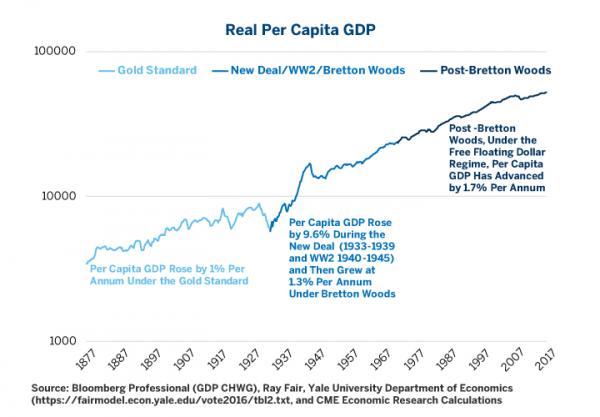

Bitcoin’s Equity Bubble and The MacroeconomyAs of this writing, bitcoin has a market cap of around $280 billion. While that’s substantial, it’s relatively small compared to the biggest corporations, which are valued north of $500 billion each. It also pales in comparison to the $75-trillion global economy. If bitcoin’s price collapsed to zero tomorrow, economic impact would be negligible. But what would happen if bitcoin rises another 1,000%, as it has thus far in 2017? If it achieves a $3 trillion market cap and then suffers a price collapse of, say, 80-90%, as it has twice thus far in its short history, what impact will it have on the economy then? Still probably fairly minimal. U.S. equities alone are valued at $25 trillion. If U.S. equities fall 10% and wipe out $3 trillion in value, that alone would not likely cause a recession. Let’s pursue a truly extreme and hypothetical case to illustrate our point. What if the currency rises to $1,000,000 per bitcoin? It may sound farfetched but it wouldn’t be too surprising given what has already happened to bitcoin prices (Figure 2). That would give it a market cap of around $20 trillion, depending upon how many bitcoins exist by then. If it then collapsed, it could have a negative impact upon the finances of more recent buyers, many of whom might not be financially well off and many of whom would have purchased near the top. If one assumes a -5% wealth effect for drops in asset prices – a dubious but common assumption—then if bitcoin one day lost $20 trillion in market cap, it could shave $1 trillion of consumer spending globally. That would be enough to slow the global growth rate by over 1%. Moreover, a crypto meltdown could also one day hit investment in computer hardware like during the collapse of technology stocks between 2000 and 2002 which led to a sharp decline in business investment and tripped the U.S. economy into a recession in 2001. A combined wealth and investment effect might drive the global economy into a recession and trigger a backlash against cryptocurrencies if they rally enough in the meantime to have such an impact. Obviously, this is an extreme hypothetical. For the moment, however, we’re not the point where this is a serious concern. And, as Aristotle once commented, ‘probable impossibilities are to be preferred to improbable possibilities.’ Investors who are buying bitcoin are presumably hoping to find someone else to sell the currency to at a higher price. That said, there is more to bitcoin economically than just the theory of the greater fool. As more people bid up the price, the difficulty of solving bitcoin’s cryptographic algorithms increases. This in turn is driving up investment in more powerful and faster computing technology of both a traditional integrated circuit and non-traditional variety. Indeed, solving cryptographic problems may be one of the first tests facing quantum computers. The problem is that investors in bitcoin and its peers are mainly out to make profits and not to finance or subsidize the development of distributed ledgers nor more powerful computers. As such, if the price of crypto assets collapsed, investors may be sorely disappointed just as many were when the first generation of internet stocks collapsed between 2000 and 2002, driving the Nasdaq 100 index down over 80%. One possible result of the current run up in cryptocurrencies and their possible collapse is that central banks may one day decide to issue their own distributed ledger currencies. Former Fed Chairman Alan Greenspan once compared making monetary policy to driving a car guided only by a cracked rearview mirror. Even now, important policy decisions must be based upon imperfectly estimated economic numbers that are weeks or months old by the time they become available. In 2017, economic policy making is still a vestige of the 20th century. Blockchain technology has the potential to one day allow policy makers to issue their own cryptocurrencies that will give them real time information on inflation, nominal and real GDP. It won’t allow them to peer through the front windshield into the future but at least they can look into the rearview mirror with much greater clarity and see out the side windows of the monetary policy vehicle. This could allow them to create the amount of money and credit necessary to keep the economy growing at a smooth pace more easily than they do today. Switching off of the gold standard vastly reduced economic volatility and improved per capita economic growth (Figures 3 and 4). Moving to blockchain-enhanced fiat currencies could further reduce economic volatility and, ironically, enable further leveraging of the already highly indebted global economy as people find ways to use capital more efficiently. More broadly, crypto-inspired investments could bring about new technologies that we cannot yet imagine. Whether bitcoin “equity” investors are rewarded for bringing about such “improvements” is another matter. A few investors in the early days of the internet during the 1990s came away enormously wealthy. Many others lost money. The current cryptocurrency boom could end in a similar fashion. |

Bitcoin Supply and Demand - Click to enlarge |

If Bitcoin Is a BubbleThe truth is that most of the assets that trade on exchanges have been in ‘bubbles’ at one time or another for reasons that have nothing to do with the existence of futures contracts. ‘Bubbles’ by the way are only visible in rear-view mirrors. Silver experienced a bubble in 1980 when the Hunt brothers cornered the physical spot market. The price soared from $4 per ounce to around $50 and then collapsed. The futures market performed just fine during this period and fulfilled its function of allowing silver users to hedge risk from the price volatility. The same can be said of subsequent bubbles, including those in the equity market in 1987 and the Nasdaq in 2000. As the housing bubble popped, beginning in 2007, the banking system suffered severe stress but futures markets functioned with neither interruptions nor bailouts. Daily margining helped to prevent the kinds of overleverage that plagued the banking sector. Many commodity prices also experienced bubbles during the past decade and saw their prices collapse. Crude oil fell from $147 per barrel in the summer of 2008 to as low as $36 per barrel by early 2009. Natural gas prices dropped from $13 per MMBtu in 2007 to as low as $2 per MMBtu by early 2015 while exhibiting bitcoin-like volatility. Metals prices also collapsed between 2011 and 2016 after huge run-ups during the previous decade. In every case, futures markets functioned well. |

GDP Growth Per Capita Improved Under the Fiat Currency Standard - Click to enlarge |

Does Bitcoin Have Inherent Value?There are those who argue that bitcoin has no inherent value and is merely a speculative vehicle. With respect to inherent value, we largely agree. Bitcoin has no inherent value. Neither do the U.S., Australian, Canadian or New Zealand dollars, the euro, the yen, the pound, the Swiss Franc or any other government-issued currency. Yet large user networks trade in these currencies in great quantity every day and agree that they do have value in the present moment. Moreover, futures contracts have existed on these fiat currencies for four decades. If fiat currencies have no inherent worth then neither do government bonds. Both are forms of debt whose value derives from taxing authorities and whose value can be eroded by inflation. Gold also has little inherent worth. It barely figures into industrial processes. Most gold is hidden away in vaults and that which is not is largely worn as jewelry – pretty but not economically functional, unless conspicuous consumption really does create value. A small amount of gold winds up in people’s teeth. The fact that gold is prized is a function of both its scarcity and a large user network that accepts that it has value. Bitcoin is no different, only more recent. And, while it can’t be worn as bling-bling, it can be exchanged for hard currency, which is accepted in jewelry stores worldwide. Only industrial metals, agricultural goods and energy products can be said to really have any inherent worth. Yet despite the critical importance of these goods, prices are not sky-high because supplies are, for the moment, abundant. |

|

Lots of Pots, Lots of Kettles

While there is much truth to saying that bitcoin has no inherent worth, there are lots of glass houses in this financial neighborhood, so one should be careful about throwing stones. Cryptocurrencies, including bitcoin, are unique. That said, one can understand them better by drawing analogies to a variety of more familiar asset classes, including fiat currencies, commodities and equities. However unique, bitcoin carries characteristics of all of these assets to which we are more accustomed.

Bottom line:

- In addition to currency and commodity-like characteristics, bitcoin also resembles equity.

- Bitcoin can create spin offs (hard forks).

- Bitcoin miners and transaction validators are compensated with bitcoin in a manner analogous to companies granting stock to employees.

- Like Wikipedia, cryptocurrencies represent non-hierarchical “teal” organizations in which people make voluntary contributions.

- Bitcoin is a bit like an equity on an ecosystem that surrounds the crypto asset rather than a traditional hierarchical corporate entity.

- If there is indeed a crypto bubble, it may be financing and incentivizing the creation of a new generation of powerful computers which could have widespread and unpredictable future applications.

- Investors in cryptocurrencies may or may not benefit from popularizing the blockchain and distributed ledgers.

- At the moment, bitcoin is too small to pose any threat to the stability and continued growth of the global economy but this could change if the currency rises to a much higher value and then collapses.

Tags: Alan Greenspan,Alternative currencies,Bitcoin,Blockchain technology,Blockchains,Business,central banks,Crude,Crude Oil,Cryptocurrencies,Currency,Decentralization,Digital currency,Economics of bitcoin,faster computing technology,Featured,federal government,Finance,Ford,Futures market,Global Economy,housing bubble,integrated circuit,Legality of bitcoin by country or territory,Meltdown,Monetary Policy,money,NASDAQ,Nasdaq 100,Natural Gas,New Zealand,newsletter,recession,Swiss Franc,Volatility,Yen