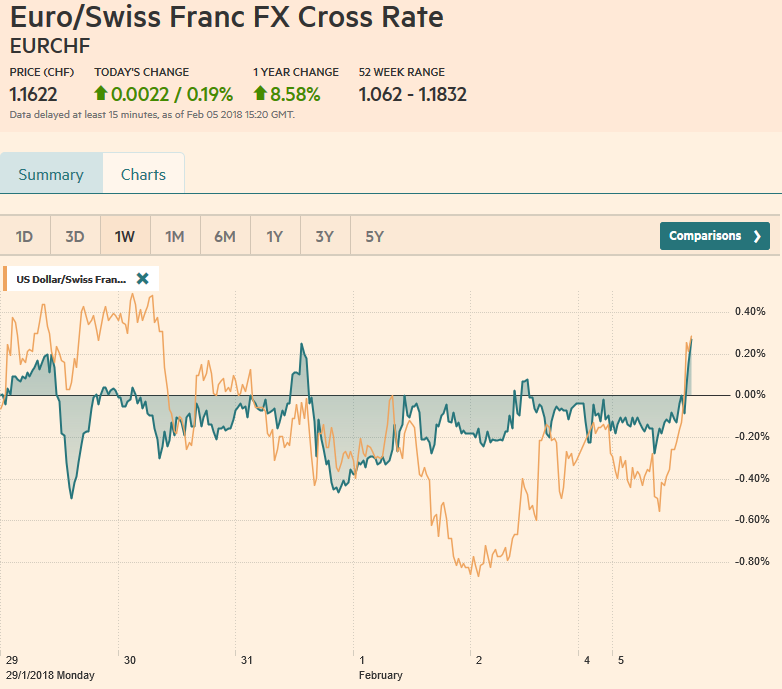

Swiss Franc The Euro has risen by 0.19% to 1.1622 CHF. EUR/CHF and USD/CHF, February 05(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Asian equity markets were weighed down by losses in the US markets ahead of the weekend. The MSCI Asia Pacific Index was off 1.4% after the 1.0% pre-weekend loss. The Nikkei gapped lower and shed 2.5% and has fallen in eight of the past nine sessions. The notable exception in Asia was the Shanghai Composite. The 0.75% was led by the financial sector amid talk that a report later this week will show a strong jump in yuan lending from banks, which are pushing in as the shadow banking is squeezed out. Strong bank lending would suggest

Topics:

Marc Chandler considers the following as important: AUD, CAD, China Caixin Services PMI, equities, EUR, EUR/CHF, Eurozone Markit Composite PMI, Eurozone Retail Sales, Eurozone Services PMI, Featured, France Services PMI, FX Trends, GBP, Germany Composite PMI, Germany Services PMI, Italy Services PMI, JPY, newslettersent, Spain Services PMI, TLT, U.K. Services PMI, U.S. ISM Non-Manufacturing PMI, U.S. Markit Composite PMI, U.S. Services PMI, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Marc Chandler writes March 2025 Monthly

Mark Thornton writes Is Amazon a Union-Busting Leviathan?

Swiss FrancThe Euro has risen by 0.19% to 1.1622 CHF. |

EUR/CHF and USD/CHF, February 05(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesAsian equity markets were weighed down by losses in the US markets ahead of the weekend. The MSCI Asia Pacific Index was off 1.4% after the 1.0% pre-weekend loss. The Nikkei gapped lower and shed 2.5% and has fallen in eight of the past nine sessions. The notable exception in Asia was the Shanghai Composite. The 0.75% was led by the financial sector amid talk that a report later this week will show a strong jump in yuan lending from banks, which are pushing in as the shadow banking is squeezed out. Strong bank lending would suggest that the deleveraging may not be as aggressive as some feared or hoped, which in turn has knock-on effects on the economic outlook. Consistent with this was news from Caixin’s service PMI (53.7 vs. 53.0) and composite reading (54.7 vs. 53.9 and expectations for a small decline). |

FX Daily Rates, February 05 - Click to enlarge |

| Japan’s service PMI rose to 51.9 from 51.1, which helped lift the composite to 52.8 from 52.2. Given Singapore role as a financial hub, its PMI is seen as a broader indication of the region, and its PMI rose to 53.6 from 52.1. Separately, Hong Kong’s PMI eased to 51.1 from 51.5 and appears to be an exception in the region.

The MSCI Asia Pacific Index left a very small gap from the lower opening that is unfilled. The gap is more evident in the European bourses. However, the selling pressure appears to have peaked, at least for the time being. The major bourses are off around 0.6%-0.8%. The German Dax and Italy’s FTSE Milan are trying to fill the opening gaps. |

FX Performance, February 05 - Click to enlarge |

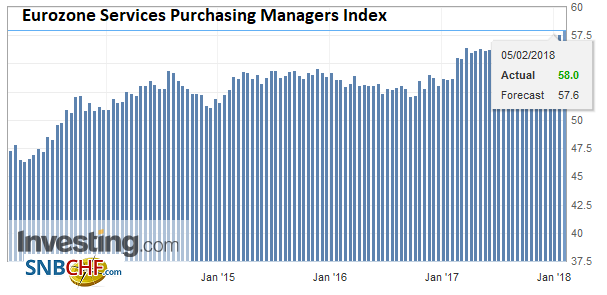

EurozoneThe eurozone reported service and composite PMIs that were stronger than implied by the flash readings and thus confirming a strong start to the New Year. The final reading on the service PMI rose to 58.0 from 57.6 of the flash. |

Eurozone Services Purchasing Managers Index (PMI), Feb 2018(see more posts on Eurozone Services PMI, ) Source: Investing.com - Click to enlarge |

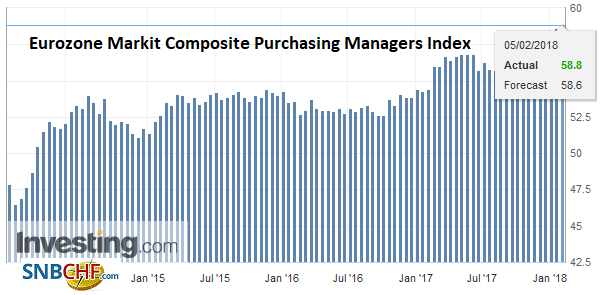

| Composite rose to 58.8 from the flash reading of 58.6. The report will provide more fodder for the ECB hawks who want to issue a clear signal of its exit intentions. Input and output prices in the PMI rose at their fastest pace since 2011. |

Eurozone Markit Composite Purchasing Managers Index (PMI), Feb 2018(see more posts on Eurozone Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

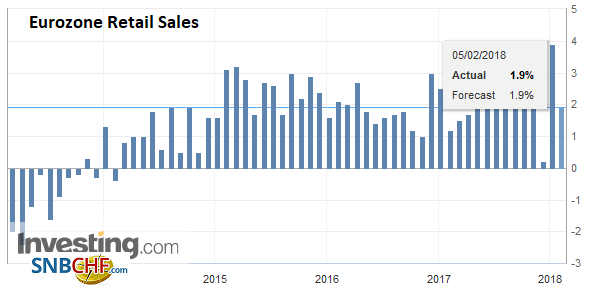

Eurozone Retail Sales YoY, Dec 2017(see more posts on Eurozone Retail Sales, ) Source: Investing.com - Click to enlarge |

|

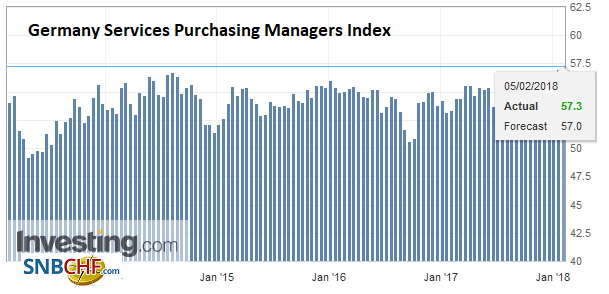

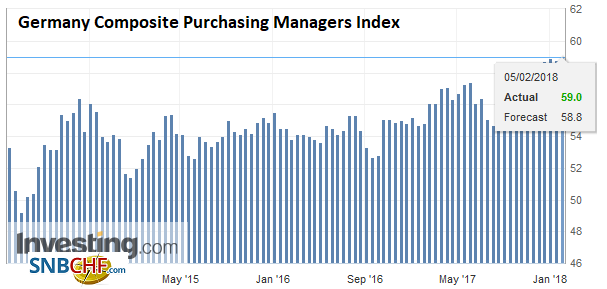

GermanyThe German flash readings were revised higher. |

Germany Services Purchasing Managers Index (PMI), Feb 2018(see more posts on Germany Services PMI, ) Source: Investing.com - Click to enlarge |

Germany Composite Purchasing Managers Index (PMI), Feb 2018(see more posts on Germany Composite PMI, ) Source: Investing.com - Click to enlarge |

|

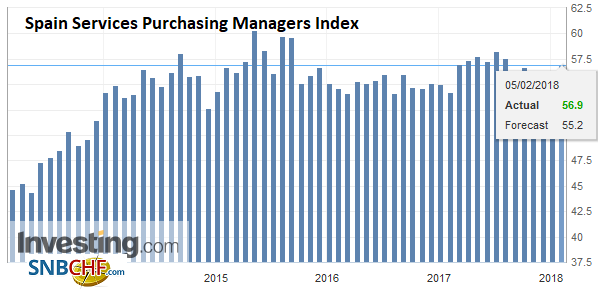

ItalyItaly and Spain readings were well above expectations. |

Italy Services Purchasing Managers Index (PMI), Jan 2018(see more posts on Italy Services PMI, ) Source: Investing.com - Click to enlarge |

Spain |

Spain Services Purchasing Managers Index (PMI), Jan 2018(see more posts on Spain Services PMI, ) Source: Investing.com - Click to enlarge |

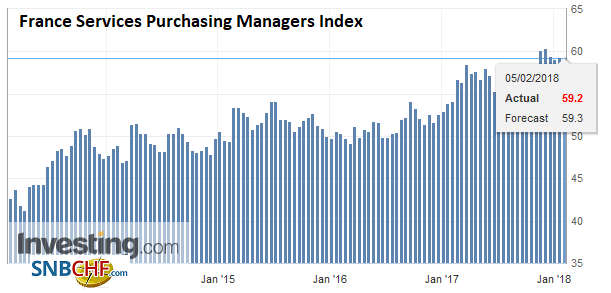

FranceFrance saw minor (0.1) revisions lower to its flash readings. |

France Services Purchasing Managers Index (PMI), feb 2018(see more posts on France Services PMI, ) Source: Investing.com - Click to enlarge |

United KingdomThe UK made it a trifecta. With today’s service reading disappointment, all three January PMIs were weaker than expected. The January service PMI eased to 53.0 from 54.2. The softer reports produced a 53.5 composite reading, down from 54.9 in December, and the lowest since August 2016. |

U.K. Services Purchasing Managers Index (PMI), Jan 2018(see more posts on U.K. Services PMI, ) Source: Investing.com - Click to enlarge |

China |

China Caixin Services Purchasing Managers Index (PMI), Jan 2018(see more posts on China Caixin Services PMI, ) Source: Investing.com - Click to enlarge |

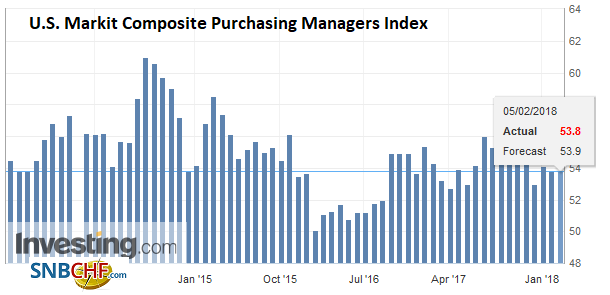

United States |

U.S. Services Purchasing Managers Index (PMI), Feb 2018(see more posts on U.S. Services PMI, ) Source: Investing.com - Click to enlarge |

U.S. Markit Composite Purchasing Managers Index (PMI), Jan 2018(see more posts on U.S. Markit Composite PMI, ) Source: Investing.com - Click to enlarge |

|

U.S. ISM Non-Manufacturing Purchasing Managers Index (PMI), Jan 2018(see more posts on U.S. ISM Non-Manufacturing PMI, ) Source: Investing.com - Click to enlarge |

The Bank of England meets later this week. There had been some creeping speculation that another rate hike could be delivered toward the end of H1 18, but the disappointing PMIs may give participants pause.

The weekend press had made it seem like the hard Brexit camp was moving to challenge Prime Minister May. However, news today that the largest donors to the party continue to support May could take some immediate pressure off her. This is an important week as the cabinet will take up the post-divorce relationship. Suggestions before the weekend that the UK could consider not leaving the customs union (which would resolve what seems like an intractable problem of the Irish border) or a modest separation (as Hammond suggested) have been effectively dashed with May confirmed no customs union.

Some suspect that May will have make more concessions to the hard exit camp. There is increasing speculation that Rees-Mogg may be brought into the government. He takes a hardline and had even advocated no transition period. Hammond seems to be increasingly in the cross-hairs of the hard Brexit camp.

Asian debt markets played catch-up to the sharp rise in the US yields before the weekend, which had been encouraged by the rise in average US hourly earnings. Average hourly earnings rose 2.9% year-over-year, the most since 2009. Average hourly earnings averaged 2.6% in the last half of 2017. Separately, at the start of last week, the US reported a 2.0% rise in Q4 labor costs, which was more than twice the rise economists expected. On the other hand, the 0.6% rise in the Q4 17 Employment Cost Index was in line with recent averages.

Australia’s 10-year bond yield shot up 10 bp to 2.93% and re-established a premium over the US. Australia’s two- and five-year yields remain below comparable US rates. The BOJ’s clear market signals at the end of last week saw the volatility sucked out of the JGB market, and the 10-year yield was steady.

European bonds are firmer. Benchmark 10-year yields are two-three basis points lower. There will be some interest in the ECB’s report that provides some details about its January bond purchases, the first month that the buying has been halved from last year. From preliminary data, it appears that the corporate bond purchases have not be cut as much as the government bond purchases. Last year, it appeared that Italian and French bond purchases had the largest deviations from the capital key, and this is expected to have continued.

The US dollar is largely consolidating the pre-weekend moves and this gives it a slightly heavier bias today. The euro and yen have remained within last Friday’s ranges. Sterling and the dollar-bloc currencies initially extended their pre-weekend losses but snapped back. The intra-day technical readings warn that the bounce may be sold. There are a couple of option strikes that are expiring in NY today that may impact activity. There is an $872 mln option struck at JPY110.00 that will be cut. Also, there is a 587 mln euro option struck at GBP0.8800 that will also expire today.

Recall that last week, the euro and Swiss franc managed to eke out minor gains against the greenback. Their resilience is still evident today. Some suspect the dollar is still be used to fund purchases of European bonds, especially the periphery, encouraged by continued ECB purchases. On the other hand the sharp steepening of the US yield curve, from 50 bp a month ago to nearly 72 bp may translate into a reduced cost of hedging US fixed-income purchases.

The stabilization of the bond and stock markets seems to be a prerequisite for clearer views of the near-term trend in the foreign exchange market. The market has priced in a March Fed hike with near certainty. The weekend Finacial Times questioned on the front page whether the Fed should have been more aggressive in hiking rates earlier. The market has only now come around to nearly accepting that the Fed will likely raise interest rates the three times this year that were indicated by the December FOMC forecasts. The implied yield of the December Fed funds futures contract has risen 16 bp since the end of last year and brought into near alignment with the Fed. The Fed raised rates more last year than the market had expected. Fed officials had to campaign hard to convince investors of a more one hike last year.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #GBP,#USD,$AUD,$CAD,$EUR,$JPY,$TLT,China Caixin Services PMI,equities,EUR/CHF,Eurozone Markit Composite PMI,Eurozone Retail Sales,Eurozone Services PMI,Featured,France Services PMI,Germany Composite PMI,Germany Services PMI,Italy Services PMI,newslettersent,Spain Services PMI,U.K. Services PMI,U.S. ISM Non-Manufacturing PMI,U.S. Markit Composite PMI,U.S. Services PMI,USD/CHF