(Disclosure: Some of the links below may be affiliate links) I have recently done simulations of how often you should invest to maximize your gains. And I thought that it would also be interesting to simulate how often we should withdraw money from the portfolio while in retirement. If you are retired and living from your portfolio, you will have to withdraw money from the portfolio to pay for your expenses. For this, you have to sell shares and use the proceeds to live. But how often should you do that? Does it even matter (hint: it does!)? This is what we are going to see in this article. I am going to use historical to simulate different withdrawal frequencies for different Safe Withdrawal Rates. Withdrawing Frequency I will assume you are familiar with the Trinity Study and how to

Topics:

Mr. The Poor Swiss considers the following as important: Financial Independence

This could be interesting, too:

Baptiste Wicht writes A few ways to simplify our life

Baptiste Wicht writes Retire Early: The Simple Guide – I wrote a book

Mr. The Poor Swiss writes 9 Reasons to Aim for Financial Independence

Mr. The Poor Swiss writes How to Open an Interactive Brokers Account in 2021?

(Disclosure: Some of the links below may be affiliate links)

I have recently done simulations of how often you should invest to maximize your gains. And I thought that it would also be interesting to simulate how often we should withdraw money from the portfolio while in retirement.

If you are retired and living from your portfolio, you will have to withdraw money from the portfolio to pay for your expenses. For this, you have to sell shares and use the proceeds to live.

But how often should you do that? Does it even matter (hint: it does!)? This is what we are going to see in this article. I am going to use historical to simulate different withdrawal frequencies for different Safe Withdrawal Rates.

Withdrawing Frequency

I will assume you are familiar with the Trinity Study and how to retire based on your portfolio. Otherwise, you should read the previous article and come back here.

When you live from your portfolio based on your Safe Withdrawal Rate, you will sell your shares from the stock market and live from this money.

There are basically two main strategies for withdrawing:

- Sell enough shares at the beginning of the year to cover an entire year’s worth of expenses.

- Sell enough shares at the beginning of each month to pay for your monthly bills.

People making yearly withdrawals argue that this way is safer from large stock market movements during the money since the money is out of the market. People making monthly withdrawals argue that this way is more effective since they keep their money in the stock market as long as possible.

So, who is right? That is what we are going to find out.

Simulations

I will run simulations based on the Trinity Study with different withdrawal rates and different withdrawing frequencies. For this, I am using data from the U.S. Stock market from 1871 to 2020. The withdrawals are taking U.S. CPI inflation historical data into account as well. In all my simulations, I assume a TER of 0.1% per year.

I am using my own tool to do these simulations. If you are interested in the tool and the data, you can look at my Updated Trinity Study article.

The output of the simulation is the success rate. Success is simply defined as not running out of money before the end of the simulation. If you end up with 1 CHF at the end of the simulation, it is still a success. And the success rate is how many simulations succeeded in the given time span compared to the total number of simulations.

Fun fact: I have run several million simulations for this article!

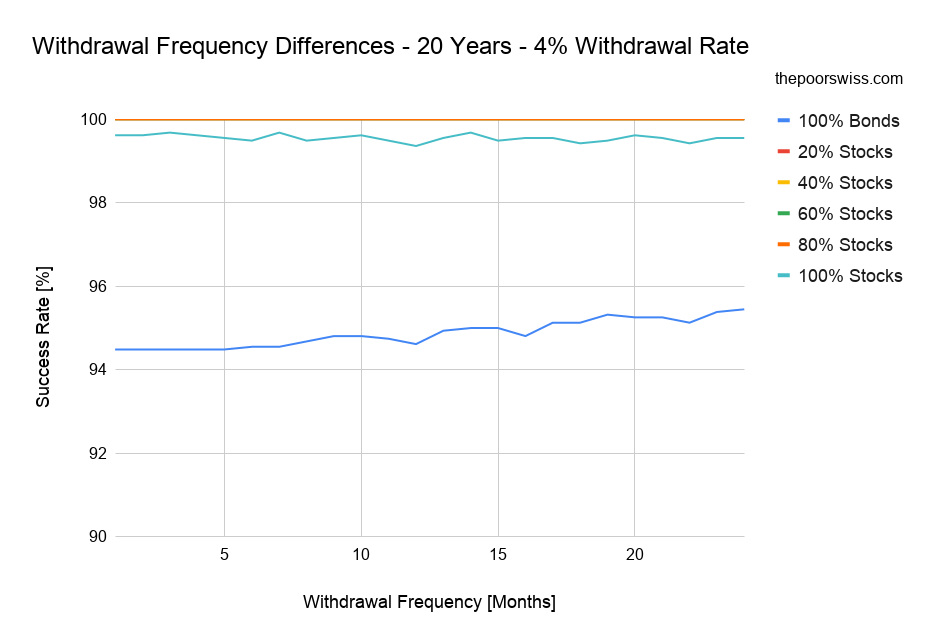

Retirement of 20 years

Let’s start with a retirement period of 20 years. Your retirement is successful if you still have money after twenty years. I am going to use a 4% withdrawal rate for this simulation.

Here are the success rates for different withdrawing frequencies and different portfolios:

Over 20 years, these simulations are not very interesting. You basically have a very high chance of success. You could actually use a higher withdrawal rate and still be fine. But we are mostly talking about early retirement, so 20 years is a short retirement time.

But back to the subject of withdrawing frequency. Interestingly, we can see that the less frequently you withdraw with a 100% bonds portfolio, the higher your chances of success are. I was not expecting this. We generally want to keep the money in the stock market to get high returns. But if the returns are not high, it should make less of a difference.

For all the other portfolios, the differences are not significant with withdrawing frequency. So, we need to increase our retirement period to see if something is interesting.

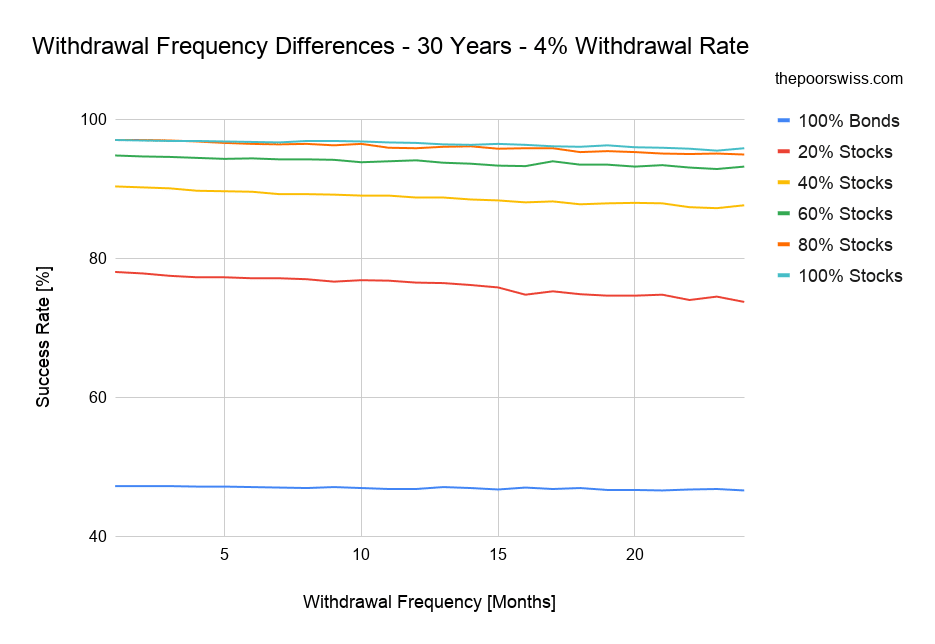

Retirement of 30 years

Let’s continue with the same simulation but for a period of 30 years. This starts to resemble early retirement. Here are the success rates in this simulation:

Over 30 years, the results look more interesting already. There is some clear difference between the different portfolios and the different withdrawing frequencies.

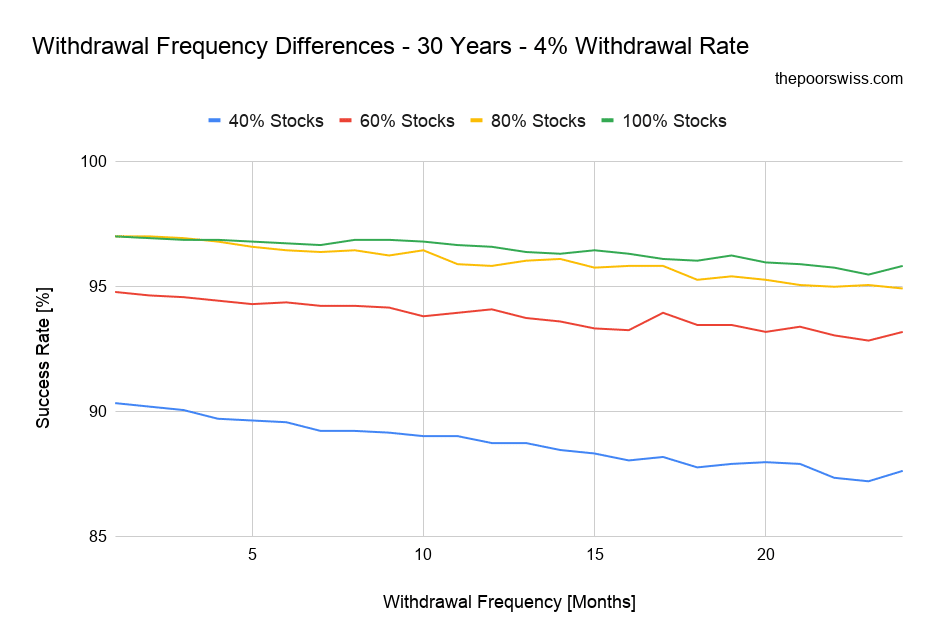

Since the 100% bonds and 80% bonds portfolios are too conservative for a 30 years retirement, let’s remove them to have a better view of the other portfolios.

Now, we can see better! And we can see that there is a significant difference between the different withdrawal frequencies. For all the portfolios, on average, a more frequent withdrawal strategy yields better results!

On average, over 30 years, you would reduce your chances of success by 2% by withdrawing every two years instead of withdrawing every month. If you withdraw every year, you would only reduce your chances of success by 0.98%.

Overall, this confirms what I was thinking. Withdrawing small sums frequently is better than withdrawing large sums at once. The reasoning is simple: you keep money in the stock market for a longer time. So, you only keep enough cash to pay one month of expenses. The rest of the money keeps compounding.

What about the claim that you would help in bad times. On average, the stock market is going up more months than it is going down. This means you bet that the stock market will go down, although it should go up more regularly. It is better to bet that the stock market will go up rather than to be that it will go down. This is the same argument against Dollar Cost Averaging.

Let’s see if this holds true for longer retirement periods as well.

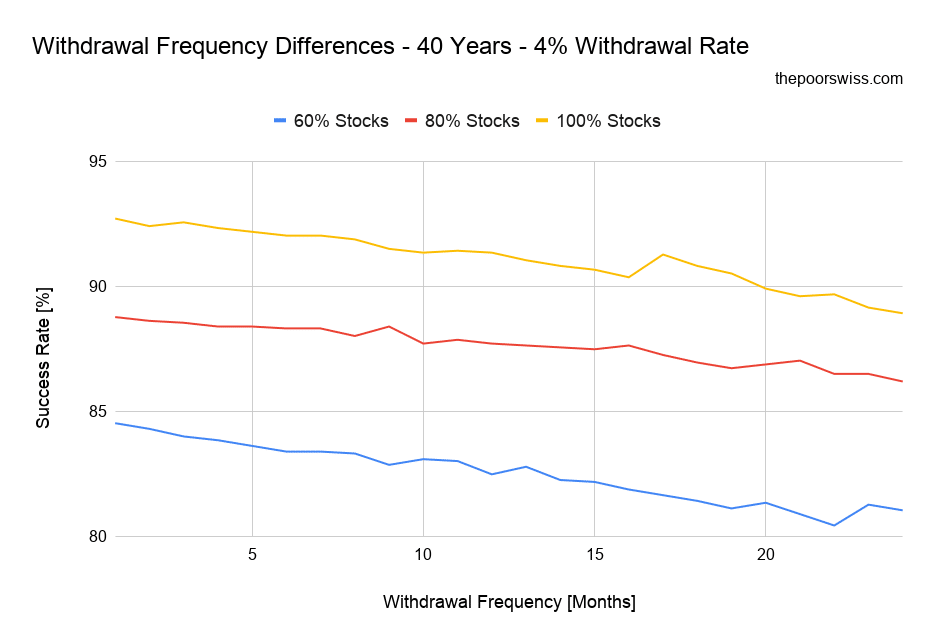

Retirement of 40 years

Here are the results with the same parameters but for a retirement that would last 40 years:

I have excluded all the portfolios that had less than a 75% chance of success, so we are left with three portfolios only.

We can see something quite interesting in these results. The differences between the different withdrawing frequencies are more significant than for 30 years.

On average, over 40 years, you would reduce your chances of success by 3.4% by withdrawing every two years instead of withdrawing every month. If you withdraw every year, you would only reduce your chances of success by 1.54%.

So, not only is the withdrawal frequency significant, but it is also more significant as your retirement gets longer.

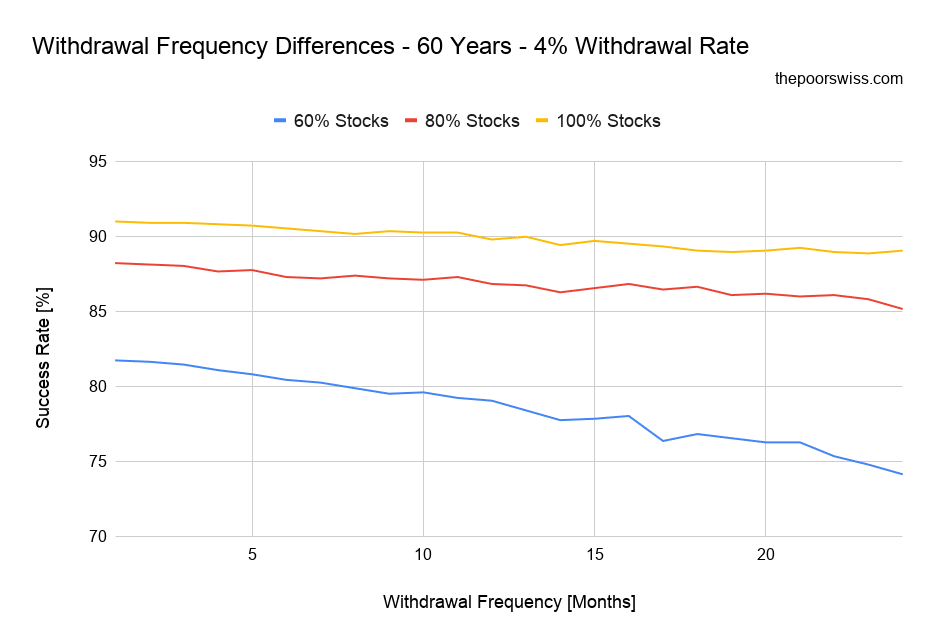

Retirement of 60 years

Let’s see the results with a final simulation with a retirement of 60 years:

Interestingly, the difference is significantly higher for a higher percentage of bonds. This makes sense since you have lower returns. Hence you need to capture them as much as possible. In this case, with a 60% stocks portfolio, your chances of success would drop by 7.5% by withdrawing every two years! This is a very significant difference.

On average, over 60 years, you would reduce your chances of success by 3.72% by withdrawing every two years instead of withdrawing every month. If you withdraw every year, you would only reduce your chances of success by 1.73%.

For a very long retirement, the withdrawing frequency gets more important. But for 60 years, it is not very significantly different than for 40 years. But we can see that some cases are very significant!

Other withdrawal rates

Until now, we did all our simulations with the famous 4% withdrawal rate. Does the same apply to other withdrawal rates? Let’s find out.

Here are the success rates for various withdrawal rates and various frequencies with a 100% stocks portfolio:

We can observe several things from these results. First, all withdrawal rates are impacted by the changes in withdrawing frequencies. Second, not all withdrawal rates are impacted equally.

Indeed, higher withdrawal rates are impacted more than lower withdrawal rates. This makes sense since lower withdrawal rates are less likely to fail, so there is not a large area for improvement. On the other hand, an aggressive withdrawal rate is likely to fail, so it has a large capacity to improve.

For instance, when comparing 12 months and one-month frequencies, a 3.25% withdrawal rate would see its chances of success dropping by 0.3%, while a 6% withdrawal rate would lose a 2.6% chance.

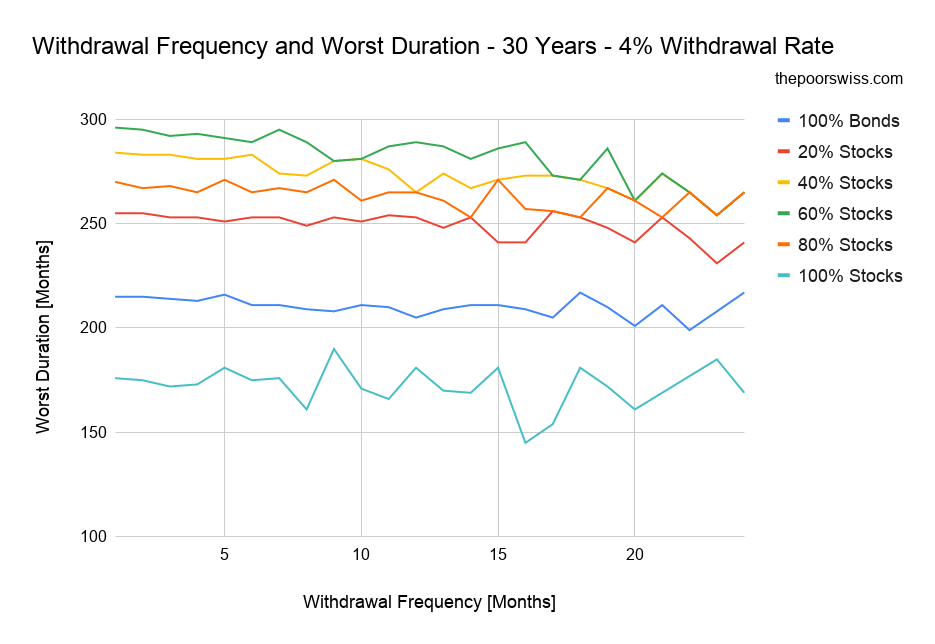

Impact on the worst duration

We can also see if changing the withdrawal frequency would change the worst duration of a simulation. The worst duration is the lowest number of months after which a simulation would fail. It is an interesting metric because sometimes the simulation’s worst duration can be catastrophic while having a high success rate.

So here are the worst durations for a 4% withdrawal rate and a 30 years duration:

It is important to realize: while 100% is the best portfolio in terms of success rates, it is the worst in terms of worst durations. This is why it is important to look at the worst duration as well as the success rate.

Now, let’s go back to the withdrawing frequency. At first sight, it is not very clear what is going on here. For a high number of stocks, the worst duration does not change much with the withdrawing frequency. It goes up and down. It is, in fact, logical since the success rate did not change much either.

Now, for more conservative portfolios, the impact of withdrawing less frequently is significant. We can see that the worst duration goes down as the number of months between withdrawals is increasing.

On average, withdrawing every year makes the worst duration worse by 5 months. And withdrawing every two years makes the worst duration worse by 10 months.

So, not only does frequent withdrawals increase your chances of success, but it also reduces the worst duration of your portfolio in retirement!

Conclusion

We are now done with all the simulations! We can draw quite a few interesting conclusions:

- If you plan a retirement of at least 30 years, the frequency at which you withdraw money is important!

- Withdrawing money every month will increase your chances of a successful retirement.

- Withdrawing money every month improves the worst duration of your retirement.

- The withdrawing frequency is more and more significant as the duration of your retirement increases.

- The withdrawing frequency is less important for low withdrawal rates.

This confirms what I was thinking about withdrawing frequency. It is good to have strong data to make such decisions. If I ever retire on my portfolio, I will sell shares every month to live from them.

If you like this kind of simulation, you can look at my previous article about investing frequency.

How often do you plan to withdraw while in retirement?