As Murray N. Rothbard explained in his masterful economic treatiseMan, Economy, and State with Power and Market,The distinctive and crucial feature in the study of man is the concept of action. Human action is defined simply as purposeful behavior. . . . The entire realm of praxeology and its best developed subdivision, economics, is based on an analysis of the necessary logical implications of this concept.All the laws of economics are derived from the fundamental facts of human action. For example, one of the most important laws of economics is the law of supply and demand. This law states that as prices of a good or service rise, demand falls and supply rises. Conversely, as prices of a good or service fall, demand rises and supply falls. The equilibrium price

Topics:

Jon Wolfenbarger considers the following as important: 6b) Mises.org, Featured, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Krypto-Ausblick 2025: Stehen Bitcoin, Ethereum & Co. vor einem Boom oder Einbruch?

Connor O'Keeffe writes The Establishment’s “Principles” Are Fake

Per Bylund writes Bitcoiners’ Guide to Austrian Economics

Ron Paul writes What Are We Doing in Syria?

As Murray N. Rothbard explained in his masterful economic treatiseMan, Economy, and State with Power and Market,

The distinctive and crucial feature in the study of man is the concept of action. Human action is defined simply as purposeful behavior. . . . The entire realm of praxeology and its best developed subdivision, economics, is based on an analysis of the necessary logical implications of this concept.

All the laws of economics are derived from the fundamental facts of human action. For example, one of the most important laws of economics is the law of supply and demand. This law states that as prices of a good or service rise, demand falls and supply rises. Conversely, as prices of a good or service fall, demand rises and supply falls. The equilibrium price of a good or service is the price where demand meets supply.

Rothbard applies the logic of human action to economic markets, where goods and services are bought for either consumption or production. The buyer of an economic good or service can rationally determine the price they are willing to pay for a good or service based on either a) the personal subjective value to them based on the utility of the good or service if it is a consumption good or b) the profit potential if it is used for production.

However, Rothbard did not apply praxeology (the study of human action) to financial markets. But since humans buy and sell investments in financial markets, praxeology can be used to analyze financial market behavior.

In this article, I will provide a brief overview of a praxeological approach to financial markets and discuss how this understanding can help economists forecast more accurately and investors invest more profitably.

Financial Markets Are Very Different

For those who have not noticed, financial markets are very different from economic markets. The motive for buying investments in financial markets—such as stocks, bonds, commodities, and cryptocurrencies—is not for personal consumption or production but to potentially profit from a future rise in the price of the investment. Thus, the key question for an investor is, “Will someone pay more for this investment in the future?”

Since no one can know the answer to that question with certainty, this different motivation for buying results in profound differences between the behavior of financial market prices and economic market prices.

One key difference is the buyers of financial market investments cannot rationally determine the value of an investment. For example, an investor in Apple stock, gold, or bitcoin has no way to precisely determine what the investment is worth to them since they are not using it for consumption or production.

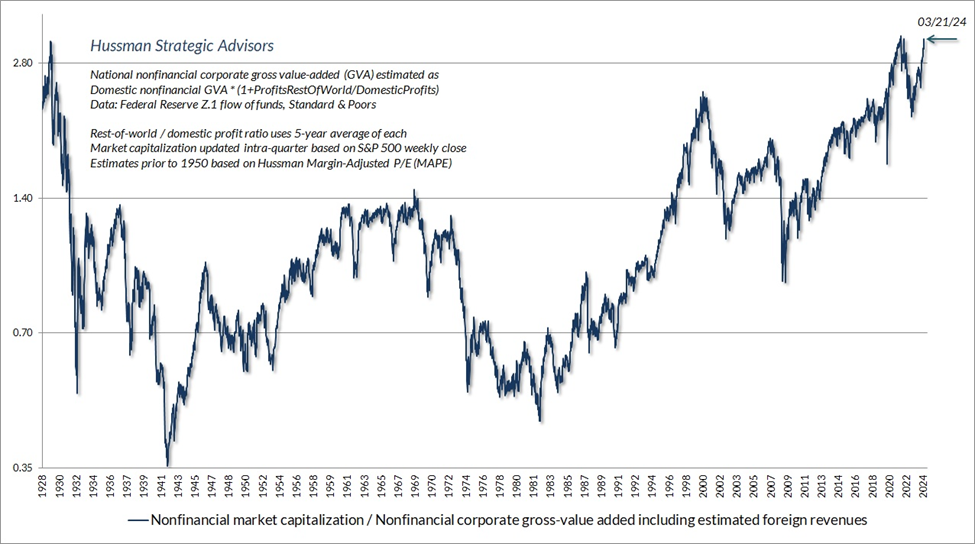

The chart below shows the ratio of the value of United States stocks compared to corporate gross value added, including estimated foreign revenues over the past century. This stock market valuation ratio is similar to Warren Buffett’s favorite valuation metric, which is total stock market value divided by gross domestic product. This ratio has proven to be the most accurate valuation metric for estimating long-term (ten to twelve years) returns for the Standard and Poor’s 500 stock index. As this chart shows, investors have valued stocks anywhere from 0.35 to over 2.80 times the amount of corporate gross value added, including estimated foreign revenues, depending on how optimistic (as in 1929 and now) or pessimistic (as in the early 1940s) they were about the future. That is more than an eight-fold difference between the high and low valuation ranges based on social mood and mass psychology.

Figure 1: Ratio of United States stock values to corporate gross value added

Source: Hussman Strategic Advisors.

If supply and demand drove financial markets the way it drives economic markets, financial market prices would remain relatively stable at an equilibrium value until there was significant new information. But financial market prices change significantly all the time. There is no equilibrium price. There are only waves of rising and falling prices driven by herding behavior shifting between optimism and pessimism.

Financial Markets Are Driven by Herding Behavior

Since investors are always buying and selling under conditions of extreme uncertainty about the value of a given investment, the majority of buy-and-sell decisions are made based on herding behavior rather than rational profit-maximizing behavior.

For example, in an economic market like computers, one would not buy more computers just because prices had skyrocketed the day before or not buy a computer just because prices had fallen significantly the day before. But that happens all the time in financial markets. In financial markets, supply usually remains fixed while demand tends to rise as prices rise and fall as prices fall, which is the opposite behavior seen in economic markets.

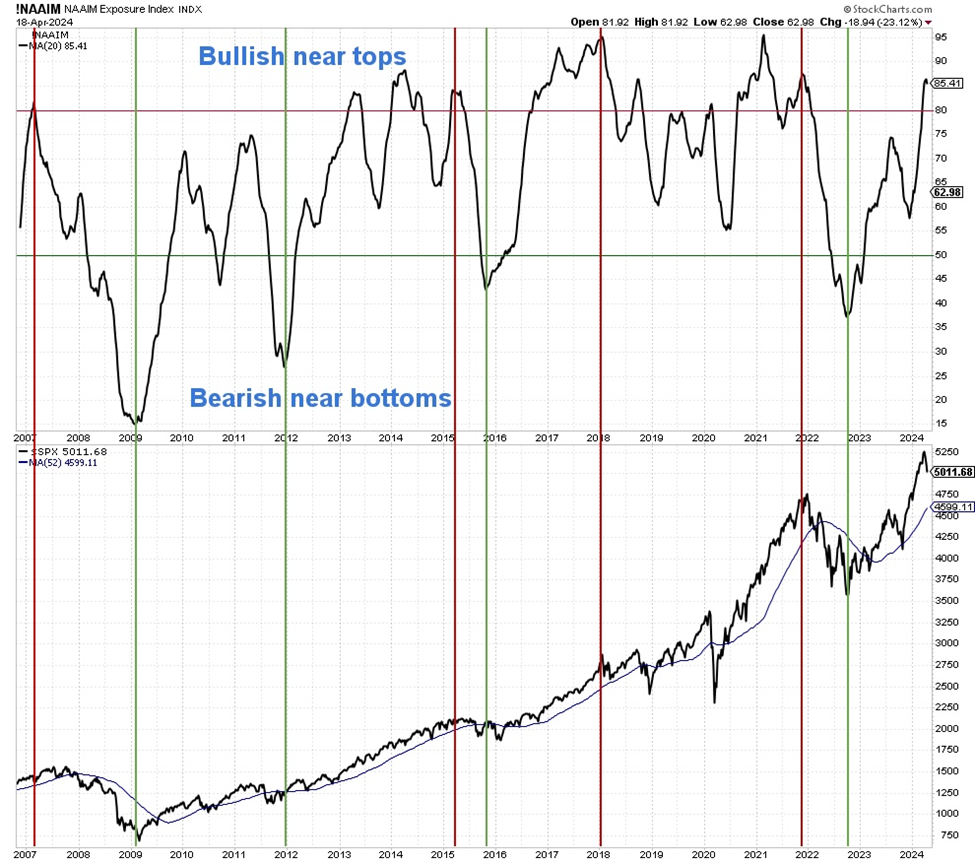

There are numerous examples of this behavior. One example is shown in the chart below of the twenty-week moving average of the National Association of Active Investment Managers (NAAIM) Exposure Index (top clip) and the Standard and Poor’s 500 stock index (bottom clip). The NAAIM Exposure Index shows the average “exposure” or allocation that professional portfolio managers have to stocks. They tend to have the highest exposure to stocks near stock market tops (red vertical lines) and the lowest exposure near stock market bottoms (green vertical lines). This herding behavior is the opposite of rational profit-maximizing behavior.

Figure 2: NAAIM Exposure Index

Source: StockCharts.com.

Herding behavior is a survival mechanism developed by humans through evolution. For example, if you saw everyone in your tribe running in one direction, you would generally be wise to run with them to avoid being eaten by a lion.

Herding behavior became hardwired into human psychology long before the creation of financial markets. As a result, instead of rationally “buying low and selling high” to profit in financial markets, most investors in the aggregate follow the herd and buy high and sell low.

Boom-Bust Business Cycles and Financial Markets

The phenomenon of the “boom-bust” business cycle has been explained by Austrian business cycle theory. This theory points out that when monetary authorities create money out of thin air to make new loans, interest rates are artificially lowered below free-market levels. This encourages businesses to borrow the newly created money and spend it on new long-term investment projects. This leads to the “boom” phase of the business cycle. Eventually, the money supply growth slows, and businesses discover that there are not enough scarce resources to complete their projects, leading to the “bust” phase of the business cycle.

How does this relate to the herding behavior of financial markets? The same waves of optimism and pessimism that drive financial markets into “bull market” uptrends or “bear market” downtrends also contribute to the business cycle. When most people in society are optimistic about the future, then banks are more willing to lend and borrowers are more willing to borrow and invest in future projects, which leads to more money creation under a fractional reserve banking system. Conversely, when most people in society are pessimistic about the future, then banks are less willing to lend and borrowers are less willing to borrow and invest in future projects (and they are also more likely to pay down or default on debt), which leads to less money creation under a fractional reserve banking system.

Thus, while it is true that the boom-bust business cycle is driven by banks creating money out of thin air, the motivation to lend and borrow is ultimately driven by optimism or pessimism about the future, which is driven by mass psychology and herding behavior.

No one, not even bureaucrats at the Federal Reserve, can force banks to lend or businesses to borrow. We saw that in the early 2000s and 2008–9 recessions when the Fed slashed interest rates but failed to prevent those recessions and stock bear markets because the social mood was pessimistic.

Investing in Financial Markets

Investors who wish to invest more profitably should learn how to analyze leading economic indicators.

The stock market has long been considered a leading economic indicator by economists. For example, The Standard and Poor’s 500 stock index is one of the ten components of the Conference Board’s US Leading Economic Index.

The reason the stock market leads the economy is because it is much easier and faster to buy and sell stocks compared to hiring new workers, building a new factory, etc.

Highly successful investors such as Warren Buffett understand the irrational herding behavior of financial market participants and use it to their advantage to consistently profit in financial markets. The fact that there are few investors who are highly successful shows how difficult it is to not follow herding behavior in financial markets.

Tags: Featured,newsletter