Swiss Economicblogs.org

Swiss Economicblogs.org

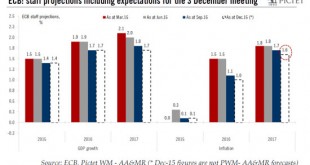

November’s upside surprises in surveys (PMI and IFO in particular) are unlikely to dissuade ECB policymakers that more needs to be done at their December 3 meeting. November’s euro area business surveys highlighted that the recovery continues to be largely led by domestic strength. In terms of countries, German surveys (PMI, IFO) surprised on the upside, whereas in France, surveys (PMI, INSEE) were less upbeat than in the previous month, partly reflecting the loss of confidence after the...

Read More »Business surveys in the euro area: solid growth in services sector