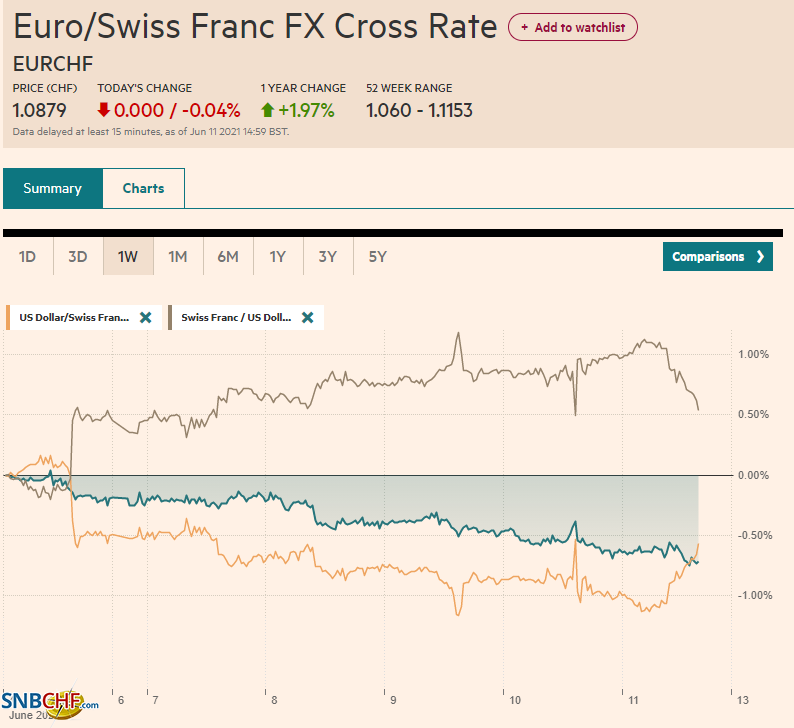

Swiss Franc The Euro has fallen by 0.04% to 1.0879 EUR/CHF and USD/CHF, June 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The 10-year US Treasury yield steadied after reaching a three-month low near 1.43%, despite the US CPI rising more than expected to 5% year-over-year. On the week, the decline of around a dozen basis points would be the largest in a year. Australia, New Zealand, and Italy benchmark yields have seen a bigger decline this week. The S&P 500 see new record highs yesterday, but the spillover effect has been muted. Japanese and Chinese stocks eased today, though most other markets rose. On the week, Thailand and the Philippines did best in the region. Europe’s Dow Jones Stoxx 600 is

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, China, commodities, CPI, Currency Movement, EUR/CHF, Featured, G7, newsletter, Russia, U.K., USD, USD/CHF, yields

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.04% to 1.0879 |

EUR/CHF and USD/CHF, June 11(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The 10-year US Treasury yield steadied after reaching a three-month low near 1.43%, despite the US CPI rising more than expected to 5% year-over-year. On the week, the decline of around a dozen basis points would be the largest in a year. Australia, New Zealand, and Italy benchmark yields have seen a bigger decline this week. The S&P 500 see new record highs yesterday, but the spillover effect has been muted. Japanese and Chinese stocks eased today, though most other markets rose. On the week, Thailand and the Philippines did best in the region. Europe’s Dow Jones Stoxx 600 is setting a new record high, but the driver is the decline in interest rates, and the rate-sensitive utility sector is leading the advance. Finance and real estate are not participating today as the benchmark closes in on its fourth weekly gain. US futures are narrowly mixed. The foreign exchange market is quiet. The greenback is mostly a little firmer, though the Australian and Canadian dollars are showing a bit of resilience. Among emerging market currencies, the Turkish lira continues to recover. Its 1% gain today brings the weekly rise to over 4%. The JP Morgan Emerging Market Currency Index is up for the fifth time in six sessions. Barring a reversal, it will be the third consecutive weekly advance. Gold has pushed back after poking above $1900, and July WTI is hovering above $70 a barrel. Other industrial commodities are firm. The CRB Index closed at new six-year highs yesterday. |

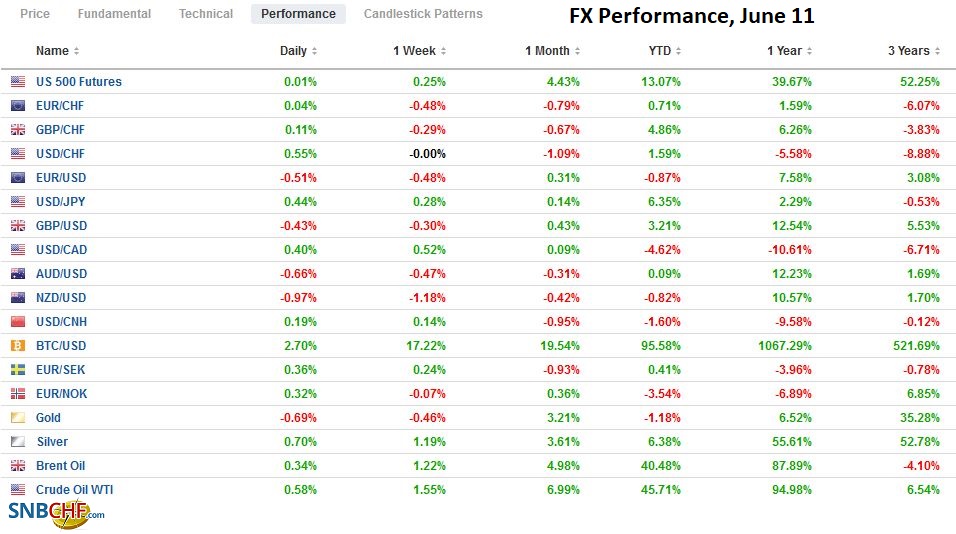

FX Performance, June 11 - Click to enlarge |

Asia Pacific

Beijing has taken several initiatives in recent weeks on commodities, the yuan, and crypto. It is stepping up its efforts to rein in commodity prices. Two new efforts on commodities have been announced. First, base metals from official reserves, including copper, aluminum, and zinc, will be made available directly to end-users. Second, steel mills in Tangshan have been ordered to restrict output (effective June 10-June 15) to combat pollution. Iron ore and steel rebar futures rallied in China today for the third consecutive session.

The US appears to be stepping up pressure on the UAE to drop Huawei and replace it. It appears to be threatening to drop the country from the F-35 jets and drones (~$23 bln) that have been ordered for delivery in 2026-2027.

China has not been invited to the G7 meeting, but it features prominently. Having a common rival is a key to the reassertion of US leadership. Efforts to re-investigate the origins of the covid pandemic are obviously not necessary to combat the virus or tighten lab security broadly, which was seen as lax. The origins of the so-called Spanish flu are still not fully agreed upon. In part, the push to keep pressure on China. Tax reform is another element as it seeks to reduce the competition between major countries. The (2011-2017) Deputy Secretary of the OECD that oversaw tax issues claimed the effort is “incomplete” as the more equitable allocation of tax revenues applies to only 100 companies.

Despite the drop in US yields this week, the dollar has been trading sideways against the Japanese yen. It remains in a tight range: JPY109.20-JPY109.80. There is a $960 mln option at JPY109.80 that expires today. It is holding around the middle of the range in Europe (~JPY109.50), where it finished last week.

The Australian dollar is trading a marginal new high for the week today (~$0.7775). It has been confined to about half a cent range, finding support around $0.7720. It settled around $0.7740 last week.

The Chinese yuan is slightly firmer today and on the week. Evaluating official efforts on the yuan is difficult because the objective is not clear. However, if the goal was to stabilize it around current levels, it succeeded. The dollar finished last month around CNY6.37 and is settling this week just below CNY6.39. Since Beijing moved to raise the reserves for foreign exchange deposits and protested through the daily fixings, the dollar peaked near CNY6.41. According to the Bloomberg survey, the dollar’s reference rate was set at CNY6.3856 today, a little stronger than the median expectation of CNY6.3847.

Europe

The ECB vowed to keep its bond-buying at a “significantly higher” level through September, though there was some disagreement about what to do in August when the lack of new issuance and liquidity typically sees lower purchases. This comes as the staff revised growth and inflation projections higher. This year’s GDP was raised to 4.6% (from 4.2%) and next year to 4.7% (from 4.1%). Its inflation projection was lifted to 1.9% (from 1.5%) this year and 1.5% (from 1.2%) in 2022. The 2023 forecasts (2.1% GDP and 1.4% CPI) were left unchanged. The risks were said to be broadly balanced for the first time since 2018.

The UK reported a surge in April GDP of 2.3% after a 2.1% increase in March. In the month, industrial output and manufacturing fell (-1.3% and -0.3%, respectively). Construction output also weakened (-2.0%). However, strength was seen in services (3.4%) and a reduced trade imbalance (-GBP935 mln from -GBP1.97 bln). The plans to re-open the economy fully in ten days look to be delayed to the end of the month.

Biden and Putin are to meet next week. The Nordstream 2 pipeline was completed yesterday, and testing starts today. The Russian central bank is widely expected to hike rates by 50 bp later today to bring the target to 5.50%. It will be the third hike this year. The first was for 25 bp, and the April move was for 50 bp. May’s inflation was reported earlier this week. The headline and core rates rose from 5.5% to 6.0%.

The euro is trading quietly inside yesterday’s range (~$1.2145-$1.2195). Two large option expirations today mark the broader range. There is a 2.2 bln euro option at $1.21 and a 1.8 bln euro option at $1.22. In the middle of the range is a nearly 2 bln euro option at $1.2150. The euro has been sold in the European morning, and the intraday momentum indicator is stretched before US dealers return to close out the week. The euro settled last week slightly above $1.2165.

Sterling recovered around a cent from the lows yesterday to close near $1.4175. Today, it reached $1.4185, just shy of the week’s high (it has not been above $1.4190 this week are reaching almost $1.4250 last week). It too has been sold in Europe today. Initial support is seen near $1.4140.

America

The larger than expected rise in US May CPI did not derail the bond rally. The bulk of the rise appears attributable to sectors that reinforce the sense that it is being driven by temporary factors adjusting to the re-opening and some supply disruptions. Used car prices rose by 7%, and this alone accounts for around a third of the headline increase. Airfare also rose sharply. Hotel accommodations, auto insurance, and restaurant prices also rose after being depressed by covid. The 10-year breakeven is around 235 bp. It peaked in mid-May near 260 bp. The five-year five-year forward is around 237 bp. It peaked in mid-May a little above 270 bp.

An increasing number of observers are warning that next week the FOMC could announce that it will begin discussing tapering. And ideas that it could adjust the interest it pays on reserves and/or the reverse repo has begun to impact the bill auctions. For example, yesterday’s sale of four-week bills produced a yield above zero for the first time in a month.

The North American economic calendar is light today. The US features the June University of Michigan’s consumer confidence and inflation expectations. Recall that last month, the 5-10 year inflation expectation rose to 3% from 2.7%-2.8% that has prevailed so far this year. Although Fed officials often talk about inflation expectations, the shift in emphasis has been to actual performance rather than projections. Mexico reports April industrial output figures and a 0.3% rise is expected after a 0.7% gain in March.

The US dollar is virtually unchanged against the Canadian dollar through the European morning around CAD1.2100. Two chunky options expire today: $1.66 bln at CAD1.2090 and the other for a little more than $600 mln at CAD1.2085. A move above the CAD1.2145 area will likely trigger stop-loss US dollar buying. The greenback finished around CAD1.2085 last week.

The US dollar remains within Wednesday’s range against the Mexican peso (~MXN19.60-MXN19.79). It is around the middle of the range and looks poised to test the lower end of the range. At the end of last week, on the eve of the legislative and local elections, it settled a little below MXN20.00.

Graphs and additional information on Swiss Franc by the snbchf team.

You Might Also Like

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

FX Daily, June 10: ECB Meeting and US CPI: Transitory Impact

2021-06-10

The ECB meeting and the US May CPI report is at hand. The US dollar is consolidating at a higher level against most of the major currencies. Softer than expected, inflation readings are weighing on the Scandis, which are bearing the brunt. The US 10-year yield closed below 1.50% for the first time in three months yesterday, and this may have helped underpin the Japanese yen.

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

FX Daily, June 08: Marking Time ahead of the Week’s Big Events

2021-06-08

The capital markets appear to be in a holding pattern ahead of this week’s big events, including the US CPI and the ECB meeting. Equities are little changed but with a heavier bias evident. Most of the large bourses in the Asia Pacific region were lower, except Australia, which eked out a small gain.

FX Daily, June 07: The Greenback Steadies after Retreating on the Jobs Data

FX Daily, June 07: The Greenback Steadies after Retreating on the Jobs Data

2021-06-07

After falling to 1.55% after the US employment data, which, while mixing expectations, could hardly be considered weak, the US 10-year yield has come back firmer today (1.58%) This may be lending the greenback a better tone. Equity markets are quiet. Most markets in the Asia Pacific region edged higher.

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

Weekly SNB Sight Deposits and Speculative Positions: Inflation is there, CHF must Rise

2021-06-07

Update June 04 2021: SNB intervening. Sight Deposits have risen by +0.3 bn CHF, this means that the SNB is intervening and buying Euros and Dollars.

FX Daily, June 04: US and Canada Report on Jobs as G7 Fin Mins Talk Taxes

FX Daily, June 04: US and Canada Report on Jobs as G7 Fin Mins Talk Taxes

2021-06-04

Stronger than expected US employment data, ahead of today’s monthly report and compromise proposal on corporate tax by the White House to help secure a deal on infrastructure sent US bond yields and the dollar high. Late dollar shorts were forced to cover.

FX Daily, May 24: China Action on Commodities and Crypto Featured

FX Daily, May 24: China Action on Commodities and Crypto Featured

2021-05-24

The US dollar is firmer in the European morning after starting out with a softer bias in Asia Pacific turnover. The dollar-bloc currencies, sterling, and the Swiss franc are heavy, but ranges are narrow, and consolidation seems to be the flavor of the day.

FX Daily, May 14: Softer Yields = Softer Dollar

FX Daily, May 14: Softer Yields = Softer Dollar

2021-05-14

The surge in consumer prices reported on Wednesday saw rates jump and the dollar push higher. Stronger than expected producer prices yesterday, and news of wage increases (average 10%) at Mcdonalds and for 75,000 people Amazon wants to hire, saw rates ease and the dollar’s upside momentum stall.

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

FX Daily, May 12: The Dollar Stabilizes but Stocks, Not So Much

2021-05-12

The markets remain on edge. Asia Pacific and US equities have yet to find stable footing, and inflation fears are elevated. The foreign exchange market has turned quiet as the dollar consolidates its recent losses.

Tags: #USD,China,commodities,CPI,Currency Movement,EUR/CHF,Featured,G7,newsletter,Russia,U.K.,USD/CHF,yields