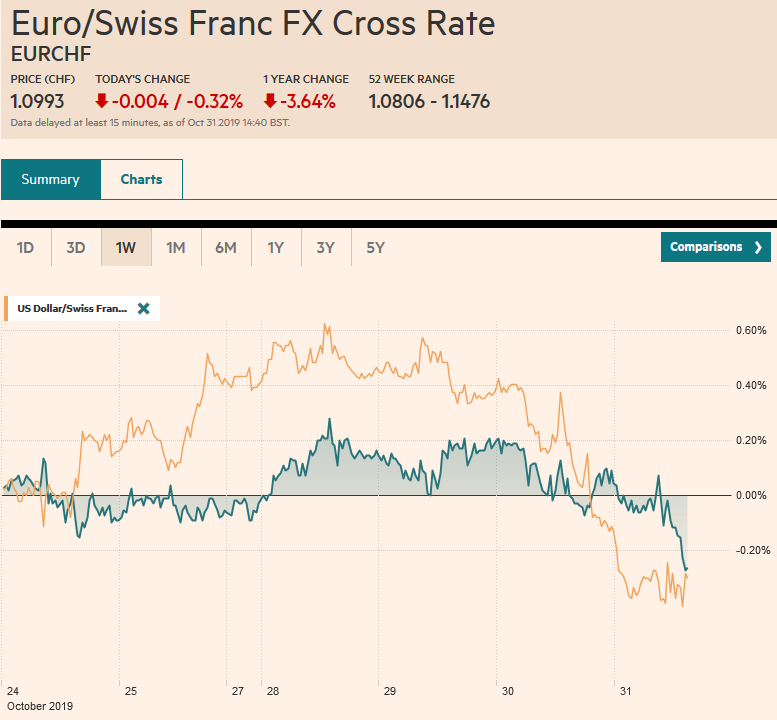

Swiss Franc The Euro has fallen by 0.32% to 1.0993 EUR/CHF and USD/CHF, October 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge FX Rates Overview: The equity and bond rally in North America yesterday carried over into today’s session. With some notable exceptions, like China, Taiwan, Australia, and Indonesia, most bourses in Asia Pacific and Europe traded higher. US shares are little changed in early Europe after the S&P 500 rose to new record highs. The US 10-year Treasury yields fell six basis points yesterday, and benchmark yields eased in Japan, China, and South Korea. HSBC cuts Hong Kong’s prime rate for the first time in eleven years, and several Middle East countries (Saudi Arabia, Kuwait, UAE, Bahrain) cut also cut

Topics:

Marc Chandler considers the following as important: 4.) Marc to Market, 4) FX Trends, Bank of Canada, Bank of Japan, Brazil, Brexit, China, China Manufacturing PMI, China Non-Manufacturing PMI, Currency Movement, EUR/CHF, Eurozone Consumer Price Index, Eurozone Core Consumer Price Index, Eurozone Gross Domestic Product, Eurozone Unemployment Rate, Featured, FOMC, FX Daily, newsletter, South Korea, USD, USD/CHF

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

Swiss FrancThe Euro has fallen by 0.32% to 1.0993 |

EUR/CHF and USD/CHF, October 31(see more posts on EUR/CHF, USD/CHF, ) Source: markets.ft.com - Click to enlarge |

FX RatesOverview: The equity and bond rally in North America yesterday carried over into today’s session. With some notable exceptions, like China, Taiwan, Australia, and Indonesia, most bourses in Asia Pacific and Europe traded higher. US shares are little changed in early Europe after the S&P 500 rose to new record highs. The US 10-year Treasury yields fell six basis points yesterday, and benchmark yields eased in Japan, China, and South Korea. HSBC cuts Hong Kong’s prime rate for the first time in eleven years, and several Middle East countries (Saudi Arabia, Kuwait, UAE, Bahrain) cut also cut key rates today. In Europe, bond yields are mostly 3-4 bp lower. The US dollar has softened against most of the major currencies but the Canadian dollar. The South Korean won, and Chinese yuan lead the emerging market currencies higher today. The South African ran, Turkish lira, and Mexican peso nursing small losses. Gold and oil are firmer but within recent ranges. |

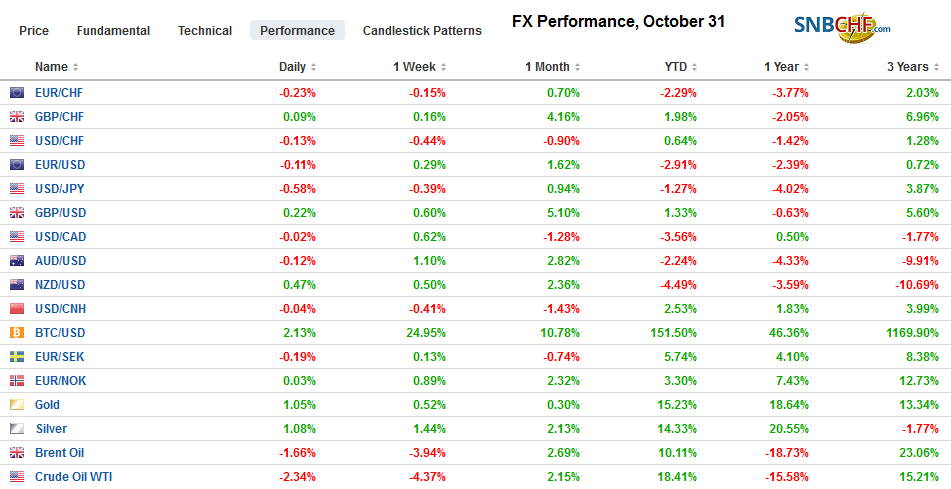

FX Performance, October 31 - Click to enlarge |

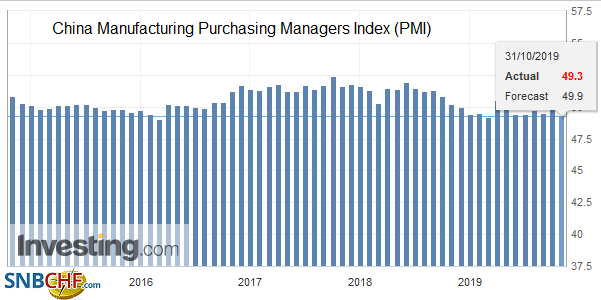

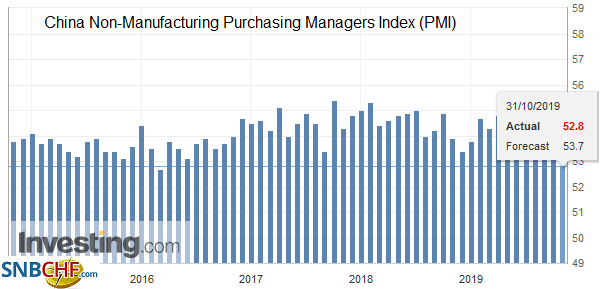

Asia PacificChina’s official October PMI disappointed. The manufacturing PMI slipped to 49.3 from 49.8, and the non-manufacturing PMI fell to 52.8 from 53.7. This translated into a composite reading of 52.0, down from 53.1. Economists project a further slowing in the world’s second-largest economy and see the pace falling below 6% next year. Separately, Hong Kong reported that Q3 GDP plunged 3.2% quarter-over-quarter, which is around five-times worse than economists forecast. |

China Manufacturing Purchasing Managers Index (PMI), October 2019(see more posts on China Manufacturing PMI, ) Source: investing.com - Click to enlarge |

| As protests that were initially sparked by a CLP30 (four-cent) increase in subways fares roiled Chile, next month’s APEC meeting has been canceled. Of course, it can be held somewhere else. The Chilean government has reversed itself and boosted pensions and minimum wage. In terms of the US-China trade deal, it does not matter in the short-term. China is buying for US agriculture products and granting more exemptions from the tariffs it imposed. The test of how real these talks are is December 15 tariff that the US has threatened. Until this is off the table, the tariff truce has not been secured. |

China Non-Manufacturing Purchasing Managers Index (PMI), October 2019(see more posts on China Non-Manufacturing PMI, ) Source: investing.com - Click to enlarge |

The Bank of Japan met market expectations. It did not change rates but adjusted its forward guidance and reduced growth forecasts. The BOJ shifted for date-linked guidance (spring 2020) to one tied to its confidence that there is momentum toward its inflation target. It shaved its core inflation forecast for FY21 to 1.5% from 1.6%.

Japan’s Justice Minister Kawai resigned after a magazine article alleged his wife made an illegal campaign contribution. This is second such resignation in the past week stemming from reports in Shukan Bunshun. Economic Minister Sugawara resigned after his secretary improperly gave the equivalent of less than $250 to a constituent in mourning. Following yesterday’s news of a surge in retail sales (ahead of the Oct 1 tax increase, Japan reported industrial output jumped 1.4% in September, more than three times what the median forecast in the Bloomberg survey forecast. It entirely offset the 1.2% decline in August, and the year-over-year rate jumped to 1.1% from -4.3%.

South Korea’s industrial output jumped 2% in September, and this was four times stronger than the median forecast in the Bloomberg survey. The fact that the August series was revised to show a decline of 1.8% instead of 1.4% takes some of the shine off the report. That said, another sharp decline in semiconductor inventories (-13.7% month-over-month, the most in two years) could be signaling the bottom of this key sector and more stable prices. Samsung Electronics beat profit estimate, which helped lift the Kospi, and the Korean won.

The disappointing Chinese PMI did not weigh on the Australian dollar, which extended its advance for the fifth consecutive session. It reached a three-day high near $0.6930 today and fulfilled the (61.8%) retracement objective of the decline from the late July high near $0.7080. However, it has seen some profit-taking in the European morning.The 200-day moving average, which has checked several bounces this year, is found near $0.6960, and the (50%) retracement of this year’s decline is a little higher, around $0.6985. The dollar’s pop to JPY109.30 around the FOMC meeting yesterday appears to have exhausted the move. The greenback was sold around JPY108.60 in Asia and took another leg lower in Europe. We have been looking for the dollar to fail up here. There are $2.3 bln of options between JPY108.00 and JPY108.10 that expire today and may slow the greenback’s sudden drop. The dollar’s weakness was also evident against the Chinese yuan. It had been confined to narrow ranges above CNY7.05, and today it fell to about CNY7.0330, its lowest level since mid-August.

EuropeThe House of Lords accepted the bill, leaving only the royal assent to formalize the December 12 UK election. Although the campaign will formally begin next week, it is clear that it has been underway for some time. Today’s Daily Mail poll bears out our concern that the election may not resolve anything. The Tories remain the largest party (34%), but it does not seem likely to secure a majority. Labour is around 26%, and Corbyn’s call to re-nationalize the mail, rail, and water, is unlikely to appeal beyond his base. |

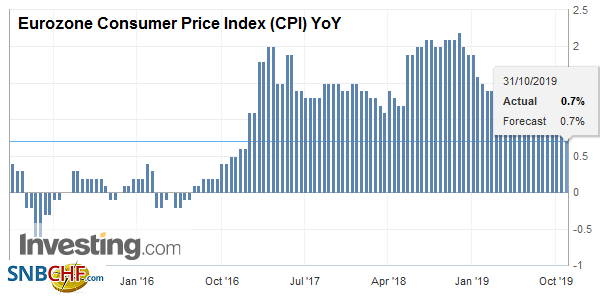

Eurozone Consumer Price Index (CPI) YoY, October 2019(see more posts on Eurozone Consumer Price Index, ) Source: investing.com - Click to enlarge |

| The Lib Dems are polling just below 20% have positioned themselves as the Remain Party, which would seem to make another coalition with the Tories unlikely. Farage’s Brexit Party, which the press reports, may strategize to avoid diluting the leave vote, is drawing around 12% support. Meanwhile, the moderate Tories are getting out of politics, and Cultural Minister Morgan indicators she will join them and not run for her seat again. |

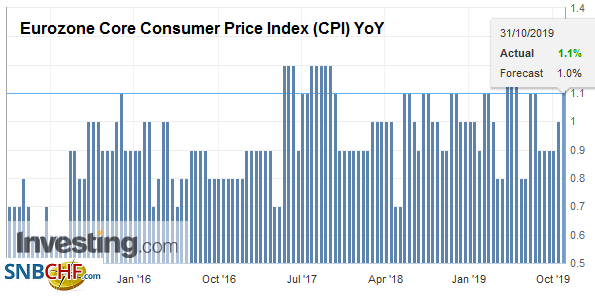

Eurozone Core Consumer Price Index (CPI) YoY, October 2019(see more posts on Eurozone Core Consumer Price Index, ) Source: investing.com - Click to enlarge |

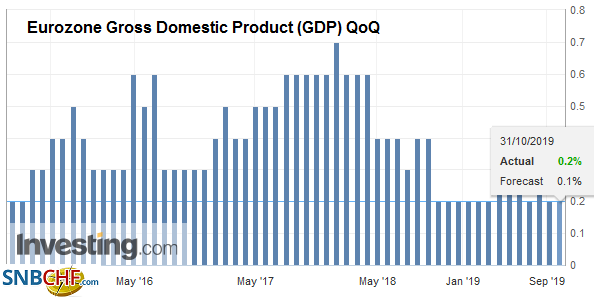

| The EMU reported Q3 growth slowed to 0.2% the same as in Q2. This translates into a 1.1% year-over-year pace. Both France and Spain grew by 0.4%. Italy was flat. Germany does not report for a couple of weeks, but many expected it to have contracted slightly for the second consecutive quarter. Euro area October CPI slipped to 0.7% from a revised 0.8% pace (initially 0.9%), but the core rate, which excludes food and energy, was stickier, unexpectedly ticked to 1.1% from 1.0%. |

Eurozone Gross Domestic Product (GDP) QoQ, Q3 2019(see more posts on Eurozone Gross Domestic Product, ) Source: investing.com - Click to enlarge |

| The euro extended its rally and briefly poked through $1.1170. It stopped shy of the month’s high set on October 21, near $1.1180. The 200-day moving average and a billion euro option that expires today are at $1.12. Intraday support is seen near $1.1120, though there is a 2.8 bln euro option at $1.1150 that expires tomorrow. For two weeks now, the sterling has chopped between around $1.28 and $1.30. There is an option for near GBP345 mln at $1.2950 and another for GBP425 mln at $1.30 that will be cut today. The euro is flattish against sterling between two chunky options that also expire today: at GBP0.8600, there is an option for 1.1 bln euros, and at GBP0.8650, there is another option for 1.2 bln euros. |

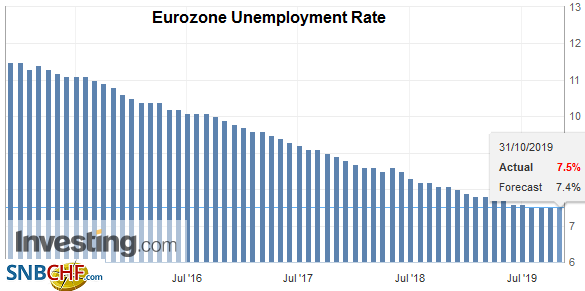

Eurozone Unemployment Rate, September 2019(see more posts on Eurozone Unemployment Rate, ) Source: investing.com - Click to enlarge |

America

The market correctly anticipated the outcome of today’s meeting, and the implied January 2020 fed funds futures contract eased by half a basis point. The 25 bp reduction was well-telegraphed and completes the midcourse correction, which also meant three cuts in the 1990s. While Powell said policy “was in a good place,” by insisting that the bar to raising rates is so high, he appeared to retain a modest easing bias. The implied yield of the December 2020 fed funds futures contracted eased 2.5 bp to 1.295%. This is consistent with the market discounting another rate cut next year.

It is true that the initial estimate of Q3 GDP (1.9%) was a little firmer than most economists expected, but the quality of the growth is questionable. While the consumer continued to shop (2.9% rather than 2.6% annualized as economists forecast), Federal spending (3.4%) also goosed growth. Inventories subtracted 0.1% from growth, not the 0.6% that was expected. However, all the inventory data has not been reported, and the change in inventories is often one of the drivers of statistically significant revisions. The 3% decline in non-residential business investment, the most in four years (after a 1% decline in Q2), is disheartening. Investment in structures slumped a sharp 15.3%, and equipment spending fell 3.8% (might be aircraft related). However, spending on intellectual property rose by 6.6%. The fact that Q3 motor vehicle output rose 1.2% may surprise given the GM strike, and given the trade conflicts, slowing world growth, and complaints about the strong dollar, net exports shaved less than 0.1% points off Q3 GDP.

The Bank of Canada offered a dovish surprise while maintaining the overnight cash rate at 1.75%. It no longer described rates at “stimulative” and or the economy operating near capacity. The central offered a more somber economic assessment. It warned that exports and business investment are likely contracting here in H2 19 and shaved next year’s growth forecast to 1.7% from 1.8% and 2021 GDP to 1.8% from 2.0%. Canadian interest rates and the Canadian dollar reacted dramatically. The two-year yield fell nearly 15 bp to 1.55%, slipping about five basis points below US rates, the most in a month. The benchmark 10-year yield fell 15 bp to 1.45%. The Bank of Canada also helped trigger a sell-off in the Canadian dollar that the technical indicators appeared to have warned. The key upside reversal in the US dollar from almost CAD1.3040 to nearly CAD1.3210. The greenback is consolidating yesterday’s advance. We peg support now near CAD1.3140 and anticipate resistance around CAD1.3240.

Mexico’s economy grew by a meager 0.1% in Q3, half of what most economists expected, but the more significant disappoint was the 0.4% year-over-year contraction. The median forecast in the Bloomberg survey was for a flat report. The odds of a rate cut at the next central bank meeting on November 14 (to 7.50%). The peso weakened initially on the news, and there was some volatility around the FOMC statement, but at the end of the North American session, it was less than 0.1% lower. We continue to see the MXN19.25-MXN19.26 as a near-term cap, which also houses the convergence of the 20- and 200-day moving averages. Separately, Brazil’s central bank delivered the expected 50 bp cut in the Selic rate, which now stands at a record low of 5.0%. It was the third successive cut, and the central bank signaled it was prepared to cut again. Inflation is slipping below target-range, and the Brazilian real is firm. The real has risen nearly 4.75% since the middle of the month, encouraged by the pension reform. The US dollar may see support near BRL3.95, but strong support is likely closer to BRL3.89-BRL3.90.The 200-day moving average is near BRL3.92.

Graphs and additional information on Swiss Franc by the snbchf team.

Tags: #USD,Bank of Canada,Bank of Japan,Brazil,Brexit,China,China Manufacturing PMI,China Non-Manufacturing PMI,Currency Movement,EUR/CHF,Eurozone Consumer Price Index,Eurozone Core Consumer Price Index,Eurozone Gross Domestic Product,Eurozone Unemployment Rate,Featured,FOMC,FX Daily,newsletter,South Korea,USD/CHF