Swiss Economicblogs.org

Swiss Economicblogs.org

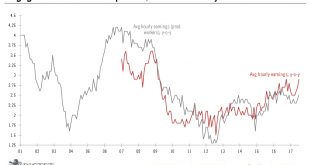

After a jobs report seriously distorted by extreme weather, the Fed remains on track to raise rates again in December.Nonfarm payrolls fell 33,000 in September, with data affected by hurricanes in the southern US. These aside, labour market signals – especially when looking at the household survey – remain solid. After a drop of 74,000 in August, employment rose 906,000 in the household survey, leading to a sharp fall in unemployment to 4.2%, the lowest rate since February 2001.The bottom...

Read More »Underlying momentum in US employment remains intact