Swiss Economicblogs.org

Swiss Economicblogs.org

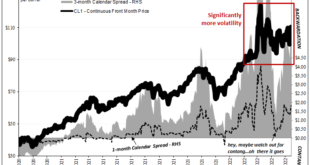

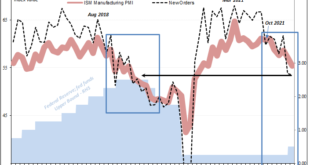

This one took some real, well, talent. It was late morning on April 11, the crude oil market was in some distress. The price was falling faster, already down sharply over just the preceding two weeks. Going from $115 per barrel to suddenly less than $95, there was some real fear there. But what really caught my attention was the flattening WTI futures curve. Up in the liquid front, it was closing in on contango and had it achieved that reshaping it would have been,...

Read More »Crude Contradictions Therefore Uncertainty And Big Volatility