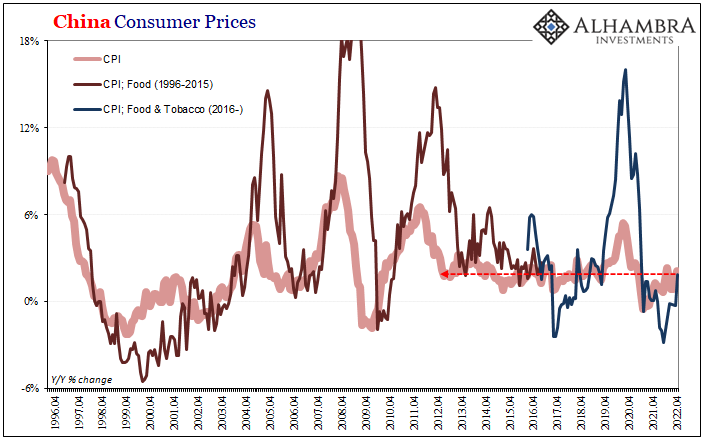

It isn’t just the vast difference between Chinese consumer prices and those in the US or Europe, China’s CPI has been categorically distinct from China’s PPI, too. That distance hints at the real problem which the whole is just now beginning to confront, having been lulled into an inflationary illusion made up from all these things. To start with, yesterday China’s NBS reported the index for its consumer prices rose 2.1% year-over-year in April 2022. That’s up from 1.5% year-over-year in March, but on the basis of base effects and a rebound (from falling) in food prices. This rate is indistinguishable from pretty much every other month since China like the rest of the world dropped off in 2012. . Yet, with consumer prices so well behaved, downright tame compared

Topics:

Jeffrey P. Snider considers the following as important: $CNY, 5.) Alhambra Investments, Australia, China, Consumer Prices, currencies, Dollar, economy, Euro, Europe, Featured, Federal Reserve/Monetary Policy, India, inflation, Markets, New Zealand, newsletter, producer prices, Yuan

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| It isn’t just the vast difference between Chinese consumer prices and those in the US or Europe, China’s CPI has been categorically distinct from China’s PPI, too. That distance hints at the real problem which the whole is just now beginning to confront, having been lulled into an inflationary illusion made up from all these things.

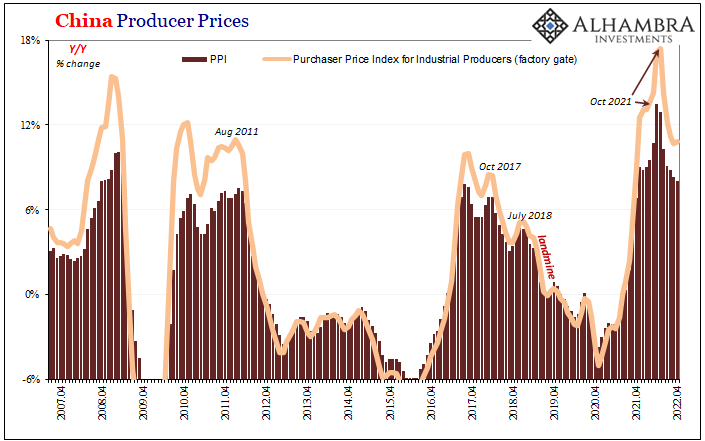

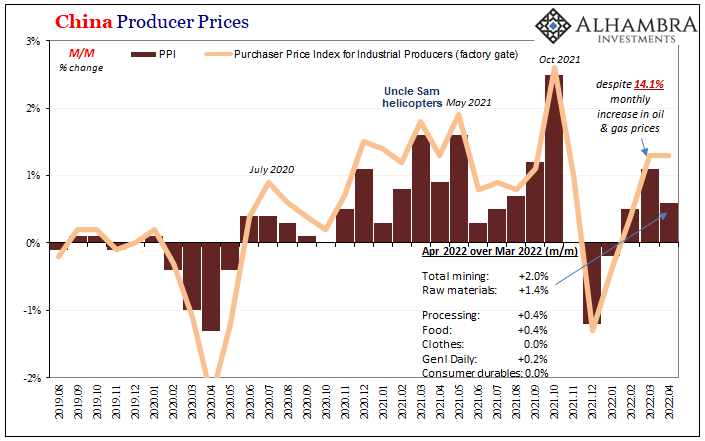

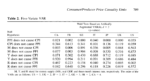

To start with, yesterday China’s NBS reported the index for its consumer prices rose 2.1% year-over-year in April 2022. That’s up from 1.5% year-over-year in March, but on the basis of base effects and a rebound (from falling) in food prices. This rate is indistinguishable from pretty much every other month since China like the rest of the world dropped off in 2012. |

. |

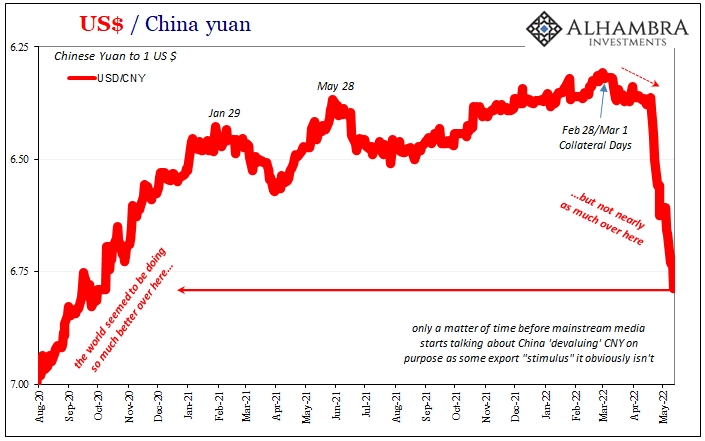

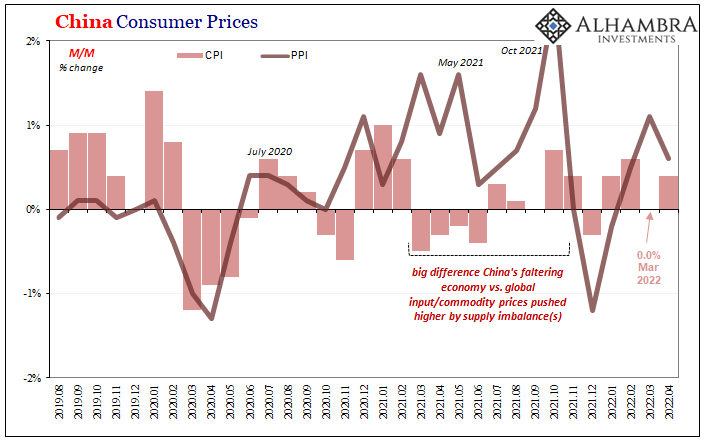

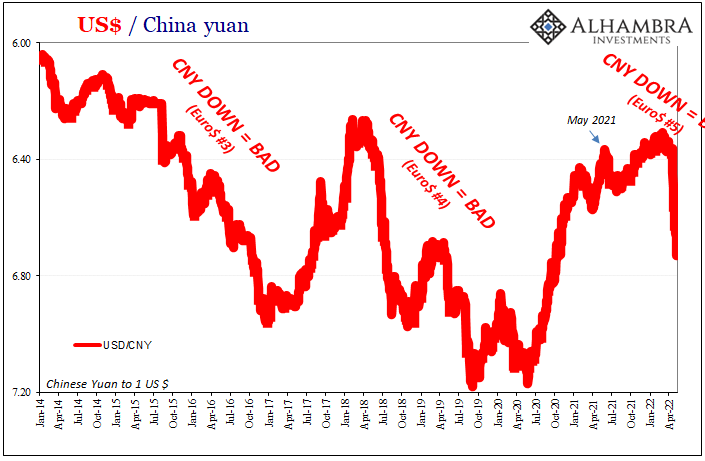

| Yet, with consumer prices so well behaved, downright tame compared to those across America and for people in Europe, it is China’s currency which is currently being destroyed. This apparent textbook “discrepancy” relates instead to what’s really going on, and why price data has been so distinct there.Producer prices, represented by the NBS PPI, continue to decelerate as they have since last October – a month that continues to show up across data and markets worldwide. The April figure for producer prices was 8.0% year-over-year, slower than 8.3% for March, the sixth straight decline (the annual change in factory gate prices did tick higher by 0.1 pts in April).

Like the falling yuan, decelerating producer prices have been consistently related to global downturns. |

. |

| Each of these a product of, as well as reinforcing for, Euro$ #5. |

. |

. |

|

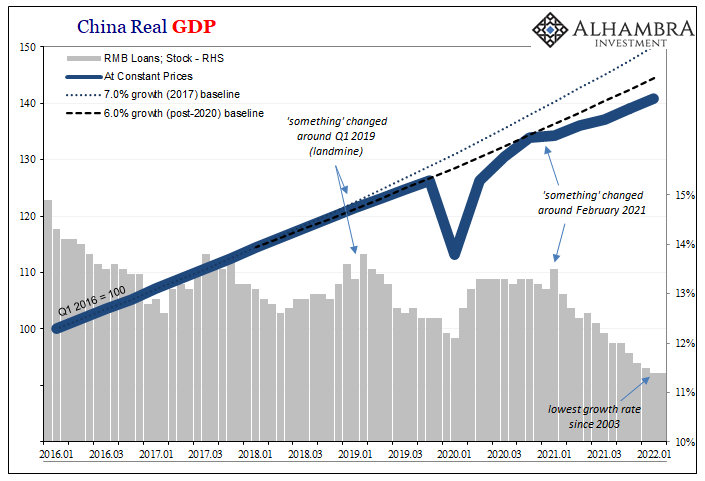

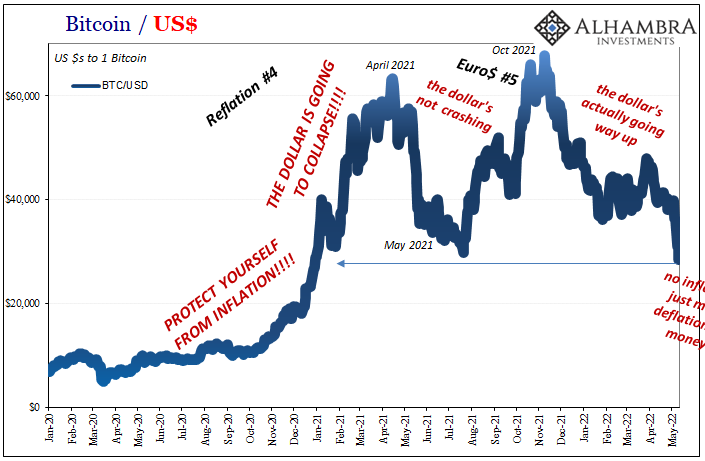

| And much of it can be traced back to how China’s economy never really recovered from its 2020 downturn/recession. That rather than inflation was the result in its CPI, whereas producer prices like the previously higher yuan were representative of nothing more than reflation (#4).

It was a reflationary period unlike the prior three in only that one respect; commodity and input prices which accelerated not from money rather from supply/demand imbalances. Since China’s economy and consumers weren’t really caught up in those, its CPI remained so timid compared to America’s and Europe’s. |

. |

| Now, however, the Chinese PPI like CNY pictures the future while the US CPI as Europe’s HICP each are looking back at last year’s illusion. |

. |

. |

|

. |

|

. |

|

| The entire global system has been more thoroughly recognizing this arrangement and increasingly synchronized direction. That’s why, for one, it isn’t just one currency or another currently being wrecked by the rising dollar (as it isn’t the dollar going up against them that is doing the wrecking, instead the various eurodollar reasons, including severe collateral constraints, which makes the dollar’s upward movement so financially and economically deadly).

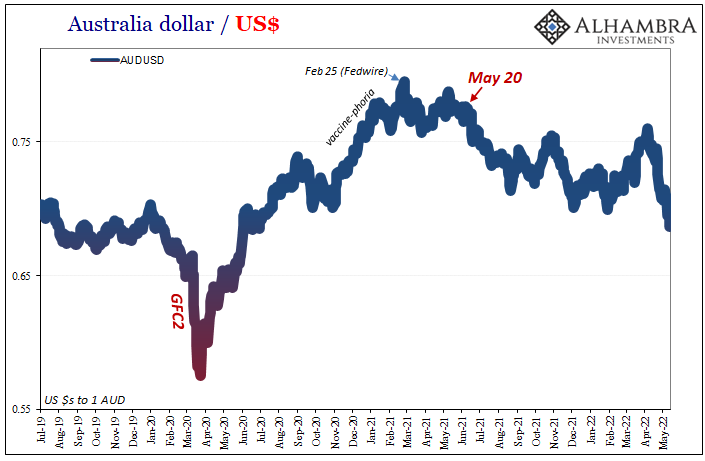

Even those which, to some extent, had been sheltered by the commodity mismatch have, like many commodities themselves, succumbed to these increasingly obvious pressures and negative possibilities. |

. |

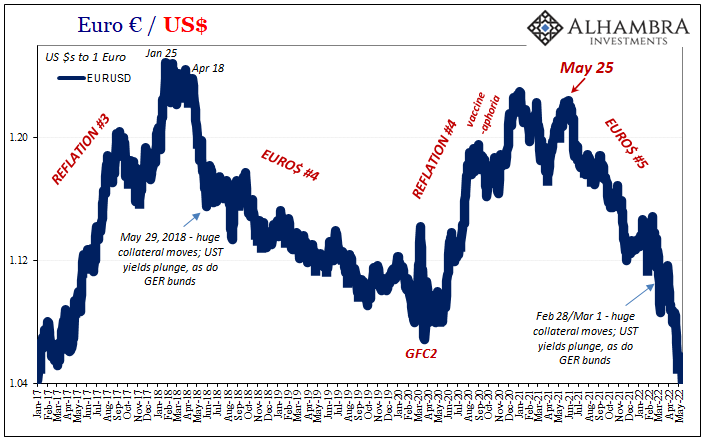

| While the euro drops closer and closer to parity with the dollar, first time in more than half a decade, the Aussie dollar moves down, too. |

. |

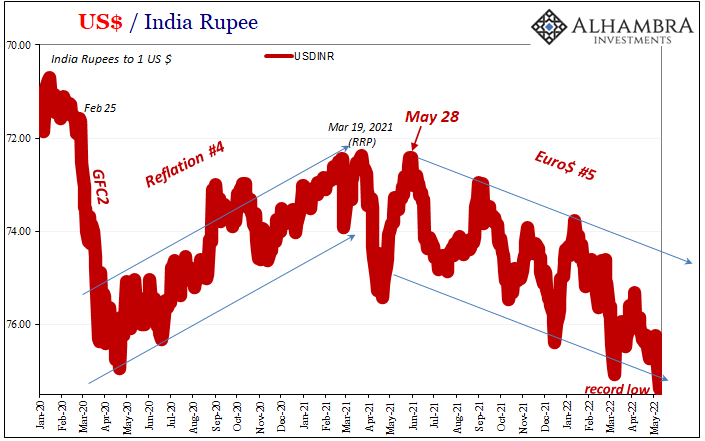

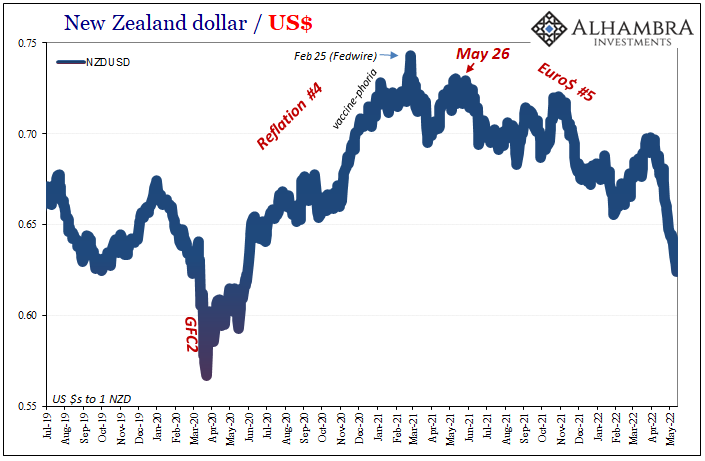

| As has New Zealand’s currency despite that country’s central bank being at the forefront of this current wave of “hawkishness” predicated on various national officials still believing in the price illusion. For each NZD which is quite sensitive to Chinese conditions, there’s an Indian rupee which stands, meaning falls, on its own.

Meaning Euro$ #5. To many, the great question insofar as China is concerned is how its government will respond. Many if not the vast majority of Western observers continue to believe (maybe it’s nothing more than hope?) Xi’s gang is going to bring out the big guns any day now. |

. |

| The truth is, Mao Xi already has, figuratively speaking, and is maneuvering in a more literal sense, too.

In fact, those two mainstream media headlines below merely demonstrate cause and effect. You can see it in Chinese prices, including, now, the price of yuan not against the dollar, not really, up against, for the fifth time, the eurodollar. It is, as always, the eurodollar’s world. We are all, including Xi, just trying to live in it. CNY DOWN… …EQUALS BAD |

. |

. |

You Might Also Like

Who’s Playing Puppetmaster, And Who Is Master of Puppets

Who’s Playing Puppetmaster, And Who Is Master of Puppets

2022-05-09

Cue up the old VHS tapes of Bill Clinton. The former President was renowned for displaying, anyway, great empathy. He famously said in October 1992, weeks before the election that would bring him to the White House, “I feel your pain.”What pain? As Clinton’s chief political advisor later clarified, “it’s the economy stupid.”

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai

2022-04-25

What everyone is saying, because it’s convenient, is that China’s zero-COVID policies are going to harm the economy. No. Economic harm of the past is the reason for the zero-COVID policies. As I showed yesterday, the cracking down didn’t just show up around 2020, begun right out in the open years beforehand, born from the scattering ashes of globally synchronized growth.

China More and More Beyond ‘Inflation’

China More and More Beyond ‘Inflation’

2022-04-17

If only the rest of the world could have such problems. Chinese consumer prices were flat from February 2022 to March, even though gasoline and energy costs predictably skyrocketed. According to China’s NBS, gas was up 7.2% month-over-month while diesel costs on average gained 7.8%.

It Wouldn’t Be TIC Without So Much Other

It Wouldn’t Be TIC Without So Much Other

2022-03-23

With the Fed (sadly) taking center stage last week, and market rejections of its rate hikes at the forefront, lost in the drama was January 2022 TIC. Understandable, given all its misunderstood numbers are two months behind at their release. There were some interesting developments regardless, and a couple of longer run parts that deserve some attention.

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)

US CPI Reaches Seven On US Goods Prices, With Disinflation Setting In Everywhere Else (incl. US Services)

2022-01-16

How is that US Treasury rates out in the independent longer end of the yield curve have now “suffered” a seven percent CPI to go along with double taper and triple maybe quadruple (if the whispers are to be believed) rate hikes this year, yet have weathered all of that allegedly bond-busting brutality with barely a market fluctuation?

As The Fed Seeks To Justify Raising Rates, Global Growth Rates Have Been Falling Off Uniformly Around The World

As The Fed Seeks To Justify Raising Rates, Global Growth Rates Have Been Falling Off Uniformly Around The World

2022-01-08

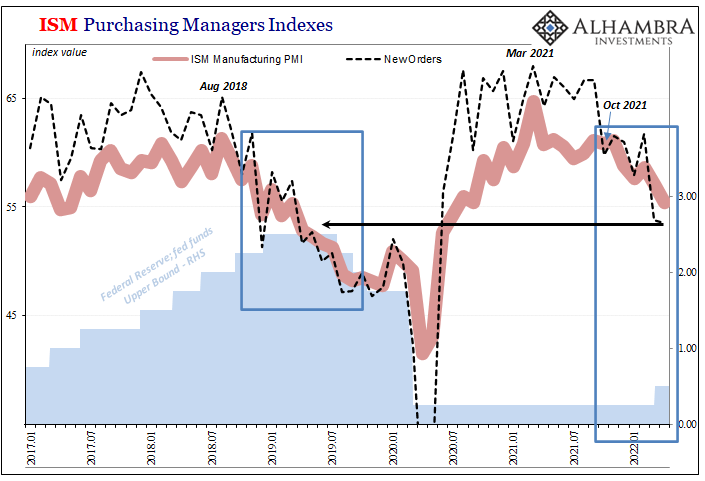

Sentiment indicators like PMI’s are nice and all, but they’re hardly top-tier data. It’s certainly not their fault, these things are made for very times than these (piggy-backing on the ISM Manufacturing’s long history without having the long history). Most of them have come out since 2008, if only because of the heightened professional interest in macroeconomics generated by a global macro economy that can never get itself going.

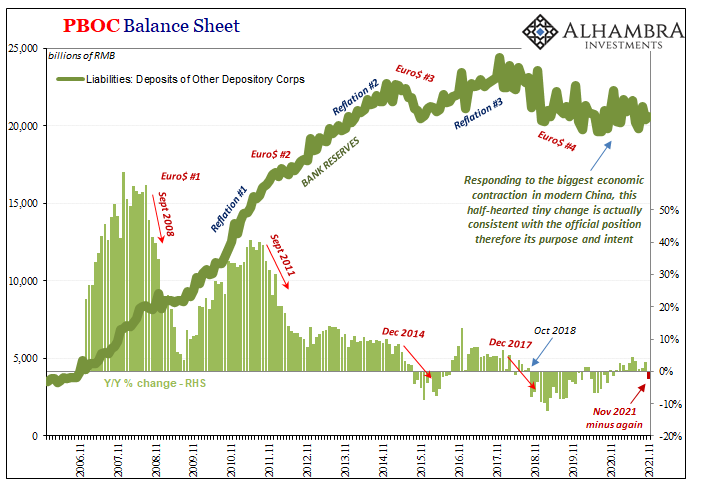

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

2021-12-25

If there is a better, more fitting way to head into the Christmas holiday in the United States than by digging into the finances and monetary flows of the People’s Bank of China, then I just don’t want to know what it is. Contrary to maybe anyone’s rational first impression that this is somehow insane, there’s much we can tell about the state of the world, the whole world and its “dollars”, right from this one key data source.

Testing The Supply Chain Inflation Hypothesis The Real Money Way

Testing The Supply Chain Inflation Hypothesis The Real Money Way

2021-12-18

Basic intuition says this is a no-brainer. Producer prices rise, businesses then pass along these higher input costs to their customers in the form of consumer price “inflation” so as to preserve profits. This is the supply chain hypothesis. Statistically, we’d therefore expect the PPI to lead the CPI.And this was expected for much of Economics’ history, taken for granted as one of those self-evident truths (kind of like the Inflation Fairy). After the dreadful experience of the Great Inflation, and the dreadful performance of Economics during it, a few scholars went back to take a second look.One of the most cited contrary studies was published in 1995 by Todd Clark of the Federal Reserve’s branch in Kansas City (Economic Review; vol. 80, issue Q III, 25-39). Using econometric evidence,

Tags: $CNY,Australia,China,Consumer Prices,currencies,dollar,economy,Euro,Europe,Featured,Federal Reserve/Monetary Policy,India,inflation,Markets,New Zealand,newsletter,producer prices,yuan