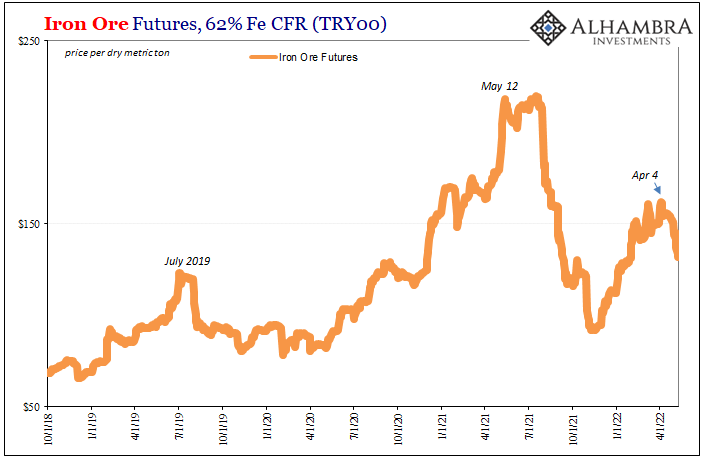

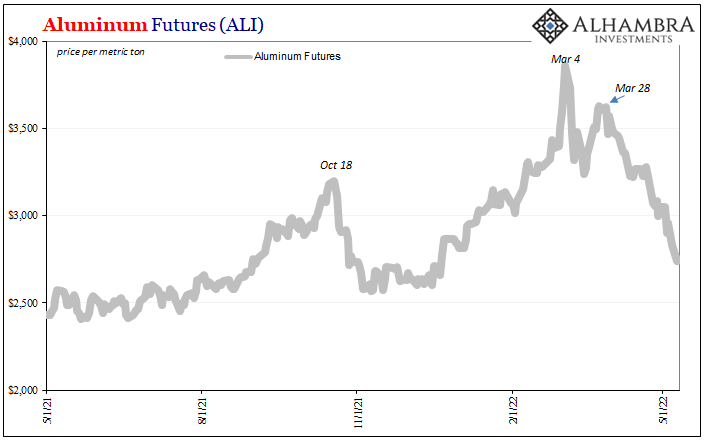

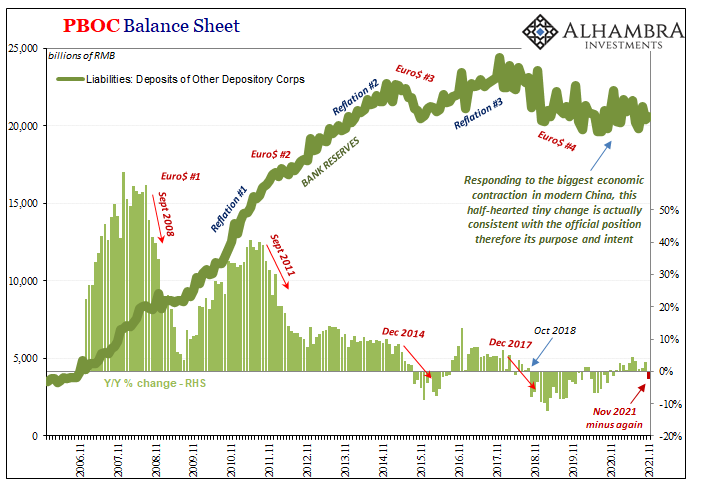

Are the industrial commodities starting to get a whiff of demand side rejection? Short run trends suggest that this could be the case. From copper to iron and the highest (formerly) of the high flyers, aluminum, this particular group has been exhibiting a rather synchronized setback going back to the end of March, start of April. This despite supply bottlenecks and production shortfalls which continue to plague each. Copper has now fallen to its lowest since last October, while iron’s 2022 rebound came to a screeching halt as it heads downward again. As to the latter, the Chinese reported a serious decline in demand for the raw metal that goes a long way back before April 2022. . . By value, China’s imports of iron bounced like the commodity’s price had, yet

Topics:

Jeffrey P. Snider considers the following as important: $CNY, 5.) Alhambra Investments, bonds, China, commodities, Copper, currencies, economy, EuroDollar, Featured, Federal Reserve/Monetary Policy, Germany, imports, industrial production, Markets, newsletter

This could be interesting, too:

Nachrichten Ticker - www.finanzen.ch writes Die Performance der Kryptowährungen in KW 9: Das hat sich bei Bitcoin, Ether & Co. getan

Nachrichten Ticker - www.finanzen.ch writes Wer verbirgt sich hinter der Ethereum-Technologie?

Martin Hartmann writes Eine Analyse nach den Lehren von Milton Friedman

Marc Chandler writes March 2025 Monthly

| Are the industrial commodities starting to get a whiff of demand side rejection? Short run trends suggest that this could be the case. From copper to iron and the highest (formerly) of the high flyers, aluminum, this particular group has been exhibiting a rather synchronized setback going back to the end of March, start of April.

This despite supply bottlenecks and production shortfalls which continue to plague each. Copper has now fallen to its lowest since last October, while iron’s 2022 rebound came to a screeching halt as it heads downward again. As to the latter, the Chinese reported a serious decline in demand for the raw metal that goes a long way back before April 2022. |

. |

. |

|

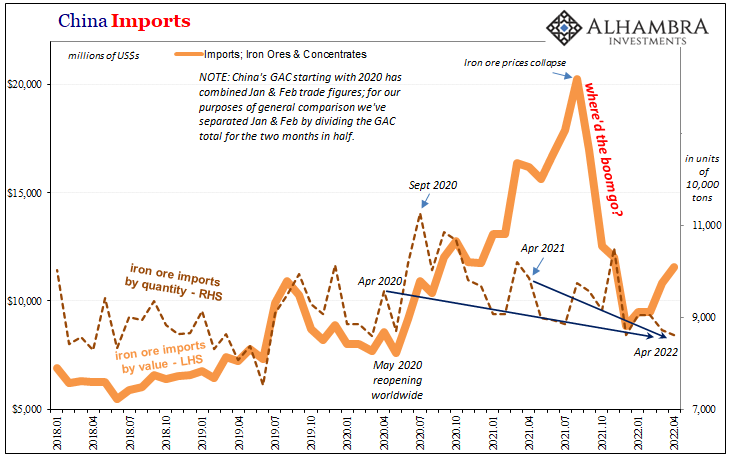

| By value, China’s imports of iron bounced like the commodity’s price had, yet by volume imports last month were 13% less than the same month in 2021.

Had bad was that? Estimated physical imports of iron were “somehow” 10% below April 2020! Lockdowns, they say. This is not what CNY reports, however. Questions aren’t being raised in these markets (eurodollar like industrial commodities) about short run demand as China grapples with more than its curious public pursuit of Zero-COVID. |

. |

As to aluminum, the Chinese didn’t want as much of that metal, either, imports down 4% year-over-year, even as those prior high prices had – small “e” economics – convinced China’s massive smelting scheme to put the pedal to the metal on production.

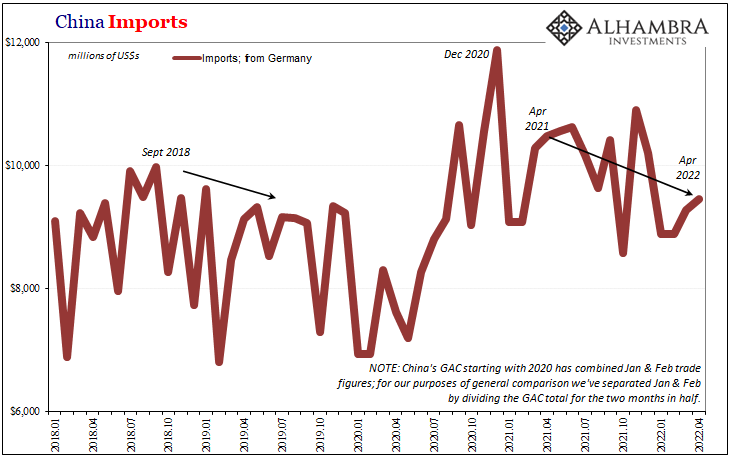

Just as economic activity really starts to reverse. China’s plight is already being picked up elsewhere, notably Germany. |

. |

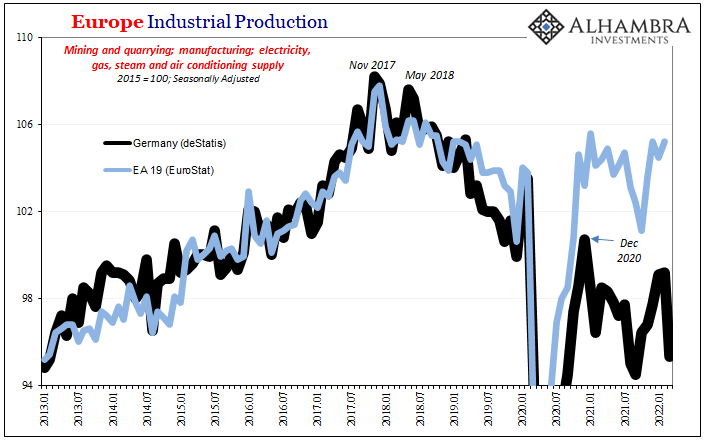

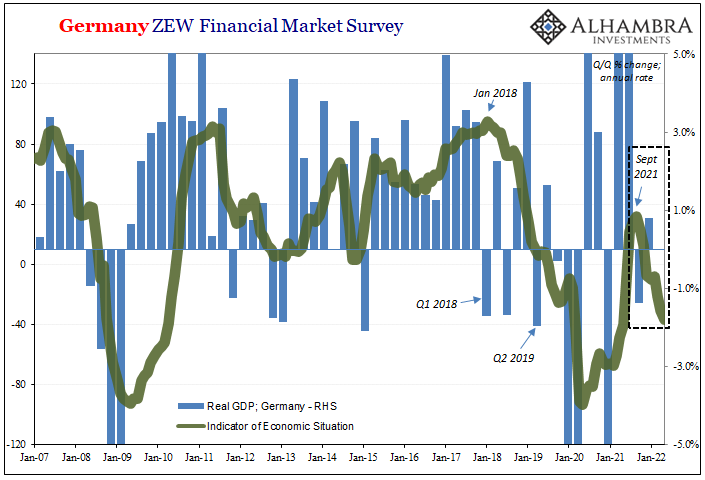

| The Germans have reported an almost continuous and likewise stream of awful economic results one after another. Though GDP managed a small positive in Q1, that won’t last – and falling output from Germany would be consistent with these other industrial price adjustments.

Industrial Production collapsed by 3.2% in March from February, the ZEW’s situation index continued its disturbing decline, there is no end in sight and not all of it should be laid at the doorstep of Vlad Putin. This has been coming since long before the invasion. |

. |

. |

|

. |

|

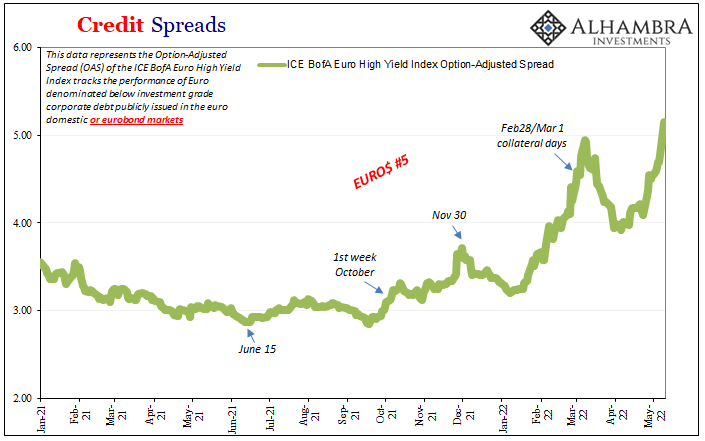

| Euro$ #5, not rate hikes or geopolitics. The latter only adds to the already-tense global economic situation.

As with Eurobond prices and credit spreads, questions about actual demand have been raised – as was always going to be the case following last year’s supply shock. Add to the shock, to some extent because of it, Euro$ #5’s increasing worldwide drag (see: CNY) and it’s getting closer to the time to synchronize – and not just China to Germany. Again. |

. |

You Might Also Like

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now

CNY’s Drop Wasn’t ‘Devaluation’ in ’15 nor ’18, and It Isn’t ‘Devaluation’ Now

2022-04-25

For one thing, that whole Bretton Woods 3 thing is really off to an interesting start. And by interesting, I mean predictably backward. According to its loud and leading proponent, China’s yuan was supposed to be ascending while the dollar sank, its first step toward what many still claim will end up in some biblical-like abyss.

The (less) Dollars Behind Xi’s Shanghai of Shanghai

The (less) Dollars Behind Xi’s Shanghai of Shanghai

2022-04-25

What everyone is saying, because it’s convenient, is that China’s zero-COVID policies are going to harm the economy. No. Economic harm of the past is the reason for the zero-COVID policies. As I showed yesterday, the cracking down didn’t just show up around 2020, begun right out in the open years beforehand, born from the scattering ashes of globally synchronized growth.

China More and More Beyond ‘Inflation’

China More and More Beyond ‘Inflation’

2022-04-17

If only the rest of the world could have such problems. Chinese consumer prices were flat from February 2022 to March, even though gasoline and energy costs predictably skyrocketed. According to China’s NBS, gas was up 7.2% month-over-month while diesel costs on average gained 7.8%.

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed

China’s Loan Results Back The PBOC Going The Opposite Way From The Fed

2022-03-16

This week will almost certainly end up as a clash of competing interest rate policy views. Everyone knows about the Federal Reserve’s upcoming, the beginning of what is intended to be a determined inflation-fighting campaign for a US economy that American policymakers worry has been overheated.

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

China’s Petroyuan, Uncle Sam’s Checkbook, The Fed’s Bank Reserves: Who Really Sits On King Dollar’s Throne? (trick question)

2022-01-14

A full part of the inflation hysteria, the first one, was the dollar’s looming crash. The currency was, too many claimed, on the verge of collapse by late 2017, heading downward and besieged on multiple fronts by economics and politics alike.

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

The Historical Monetary Chinese Checklist You Didn’t Know You Needed For Christmas (or the Chinese New Year)

2021-12-25

If there is a better, more fitting way to head into the Christmas holiday in the United States than by digging into the finances and monetary flows of the People’s Bank of China, then I just don’t want to know what it is. Contrary to maybe anyone’s rational first impression that this is somehow insane, there’s much we can tell about the state of the world, the whole world and its “dollars”, right from this one key data source.

Weekly Market Pulse: Discounting The Future

Weekly Market Pulse: Discounting The Future

2021-12-07

The economic news recently has been better than expected and in most cases just pretty darn good. That isn’t true on a global basis as Europe continues to experience a pretty sluggish recovery from COVID. And China is busy shooting itself in the foot as Xi pursues the re-Maoing of Chinese society, damn the economic costs.

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion

The ‘Growth Scare’ Keeps Growing Out Of The Macro (Money) Illusion

2021-11-26

When Japan’s Ministry of Trade, Economy, and Industry (METI) reported earlier in November that Japanese Industrial Production (IP) had plunged again during the month of September 2021, it was so easy to just dismiss the decline as a product of delta COVID.

Tags: $CNY,Bonds,China,commodities,Copper,currencies,economy,EuroDollar,Featured,Federal Reserve/Monetary Policy,Germany,imports,industrial production,Markets,newsletter