Swiss Economicblogs.org

Swiss Economicblogs.org

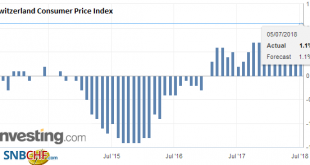

Neuchâtel, 5 July 2018 (FSO) – The consumer price index (CPI) remained stable in June 2018 compared with the previous month, reaching 102.1 points (December 2015=100). Inflation was 1.1% compared with the same month of the previous year. These are the results of the Federal Statistical Office (FSO). The stability of the index compared with the previous month is the result of opposing trends that counterbalanced each...

Read More »Swiss Consumer Price Index in June 2018: +1.1 percent YoY, Stable MoM